Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Douglas Elliman

June 3, 2015

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Douglas Elliman

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Manhattan

,

Market Reports

,

Sales

,

Statistics, Metrics & Data

,

Suburban, Urban, Commuting

,

Wall Street, Financial Services

[Three Cents Worth #288 Hamptons] Comparing Price Trends in the Hamptons and Manhattan

read more

June 3, 2015

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Douglas Elliman

,

Historical, Landmark, Milestone

,

Housing Trends & Cycles

,

Manhattan

,

Rentals, Investing

,

Sales

[Three Cents Worth #287 NY] Tracking New York Rents and Asking Prices Over a Century

read more

May 30, 2015

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Curbed

,

Douglas Elliman

,

Housing Trends & Cycles

,

Manhattan

,

Statistics, Metrics & Data

[Three Cents Worth #286 NY] How Many NYC Apartments Are Bought With Cold Hard Cash?

read more

May 22, 2015

Aspen

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Douglas Elliman

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

,

Records, Thresholds and Outliers

,

Statistics, Metrics & Data

[Three Cents Worth #285 Ski] Aspen Real Estate Has Had Many Peaks, But It’s Not Peaking

read more

May 21, 2015

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Distressed Housing

,

Douglas Elliman

,

Housing Trends & Cycles

,

Miami (Beach + Mainland)

[Three Cents Worth #284 Miami] Miami Drill Down: Picking Up the Scraps of the Financial Crisis

read more

May 21, 2015

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Douglas Elliman

,

Housing Trends & Cycles

,

Los Angeles

,

Statistics, Metrics & Data

[Three Cents Worth #283 LA] How Much Does It End Up Costing When a House Lingers on the Market in Los Angeles?

read more

December 30, 2014

Development, Construction, Architecture & Land

,

Douglas Elliman

,

Miami (Beach + Mainland)

,

Public Speaking

,

Urban Land Institute

Speaking at ULI Miami Condo Market Symposium

read more

October 1, 2014

Douglas Elliman

,

Elliman Reports

,

Manhattan

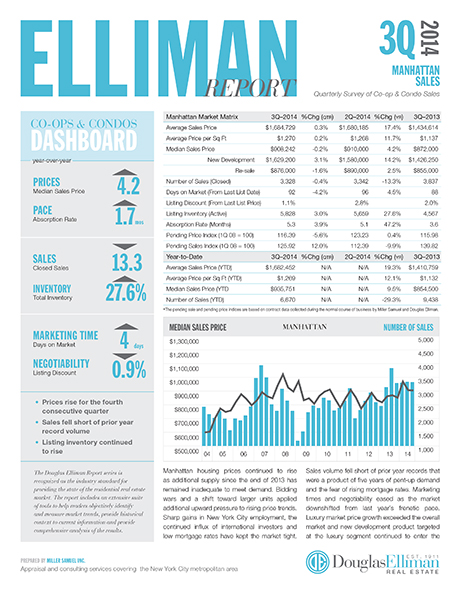

3Q14 Manhattan Sales Market: Operating Just Below Record Levels

read more

July 30, 2014

Douglas Elliman

,

International

,

Knight Frank

,

Manhattan

,

Market Reports

,

Miami (Beach + Mainland)

North America Leads Luxury Housing Trends in 2Q14 – Knight Frank

read more

July 14, 2014

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Manhattan

,

Queens

,

Rentals, Investing

Adding Queens To Our Manhattan/Brooklyn Rental Report

read more

July 14, 2014

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Putnam County

,

Queens

,

Westchester County, NY

2Q14 Brings Mixed Regional Messages – Brooklyn, Queens and Westchester/Putnam Reports

read more

July 1, 2014

Douglas Elliman

,

Elliman Reports

,

Manhattan

,

Sales

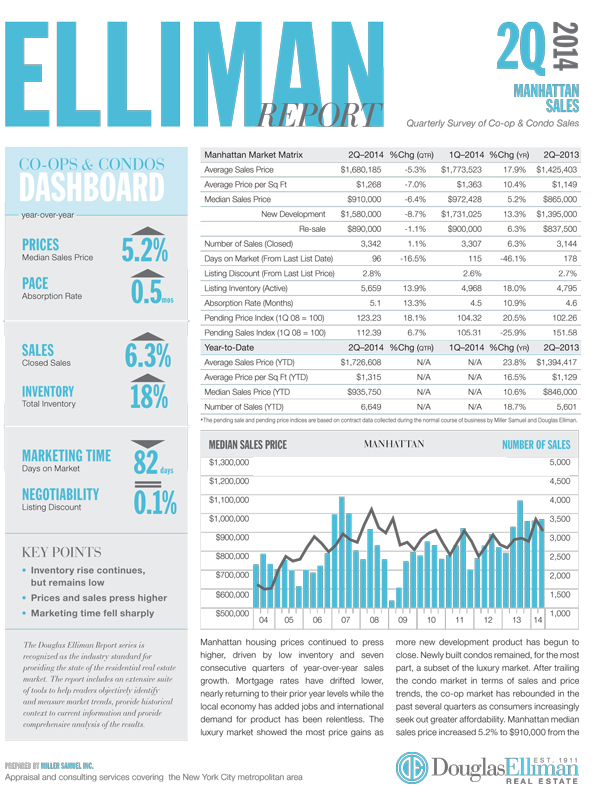

2Q14 Manhattan Sales Market: More Supply, But Not Even Close to Enough

read more

Previous

2

3

4

Next

Load More Posts

Page load link

Go to Top