Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› New York Times

January 31, 2014

Backyard BBQ Talk

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

New York Times

,

Records, Thresholds and Outliers

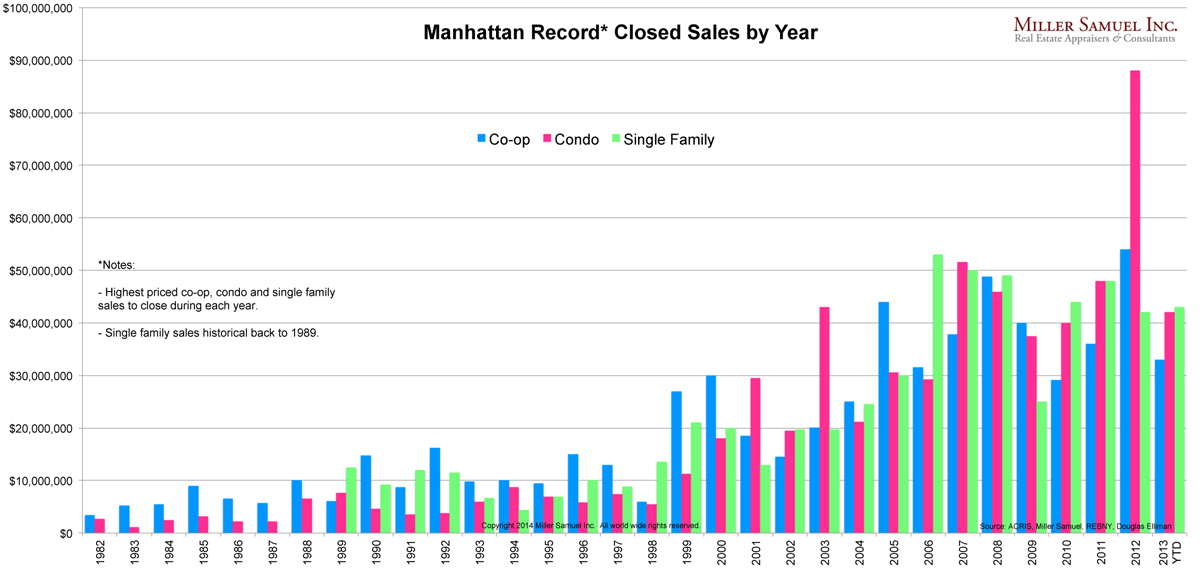

Manhattan Price Records from 1982 to 2013 (Will Soon Be Broken)

read more

October 28, 2013

Brokers, Agents, MLS, NAR

,

Market Reports

,

New York Times

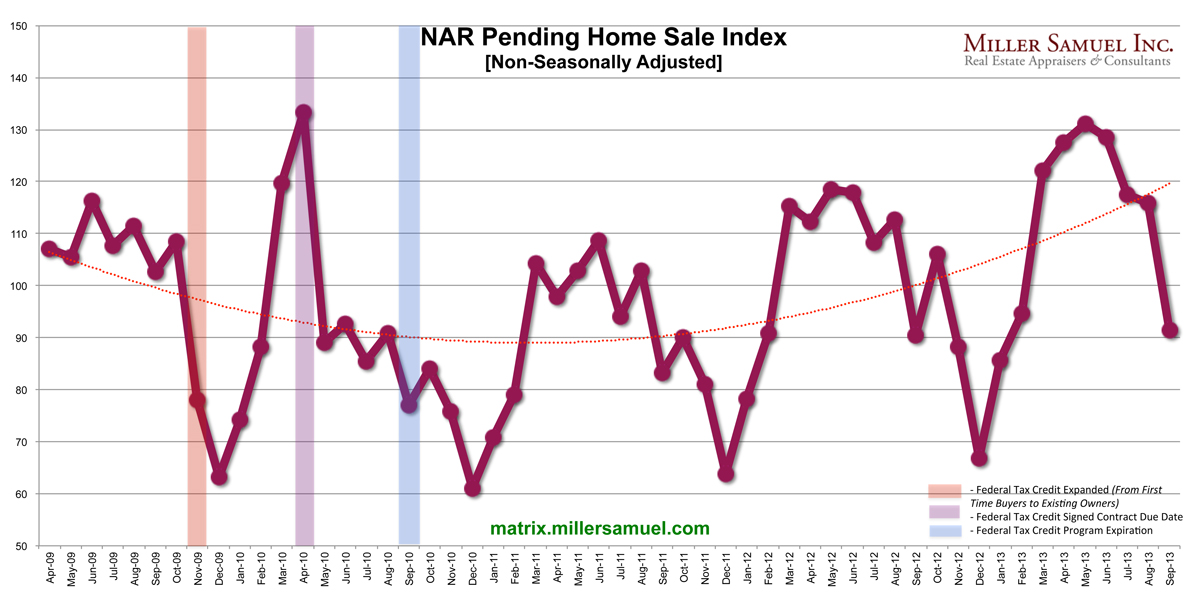

NAR Pending Home Sale Index Sort of Goes Negative

read more

September 16, 2013

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

New York Times

,

Wall Street Journal

The Low Appraisal “Hassle” is a Symptom of a Broken Mortgage Process

read more

September 10, 2013

Elliman Reports

,

International

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Times

[Country Life article] Once upon a time in the American market

read more

July 14, 2013

Boom Bubble Bust

,

Douglas Elliman

,

Manhattan

,

New York Times

Appearing on New York Times’ Page One NEVER Gets Old…But It’s A Process

read more

July 11, 2013

Brooklyn

,

Credit, Finance, Mortgage, Rates

,

Douglas Elliman

,

Elliman Reports

,

New York Times

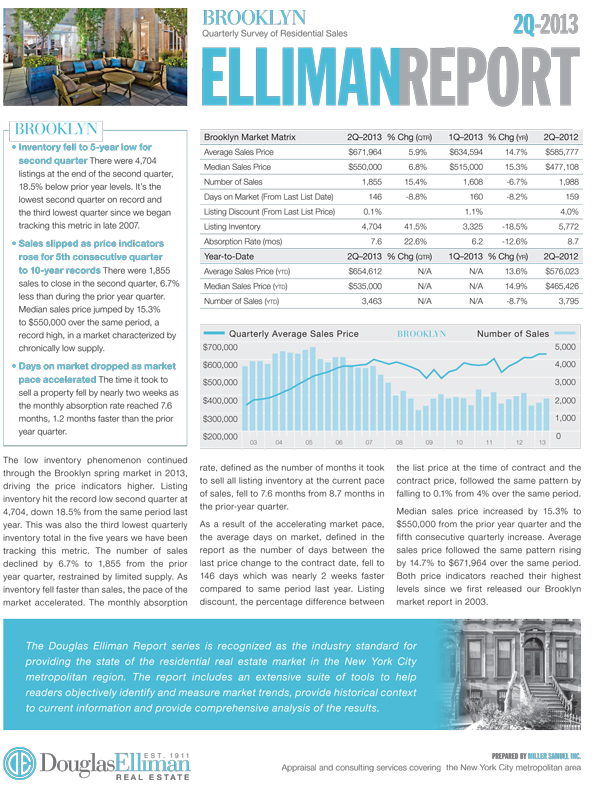

[Plan B] 2Q 2013 Brooklyn Report

read more

February 12, 2013

Manhattan

,

New York Times

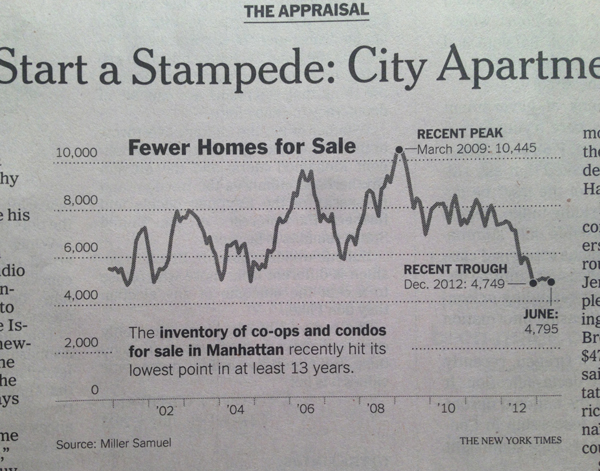

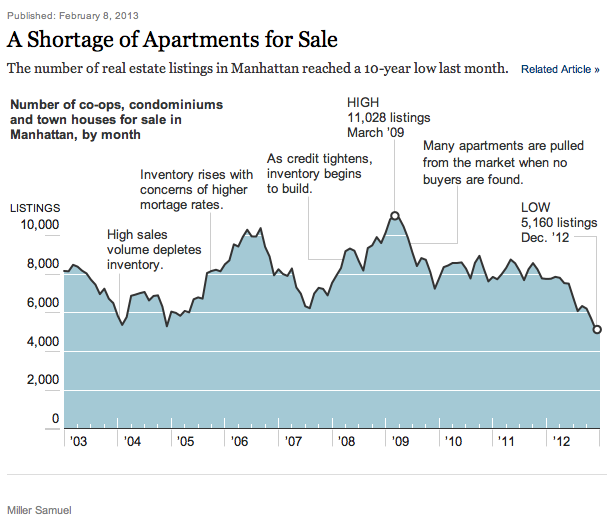

Listing Inventory Is, Well, Listing

read more

February 6, 2013

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Federal Reserve, New York

,

New York Times

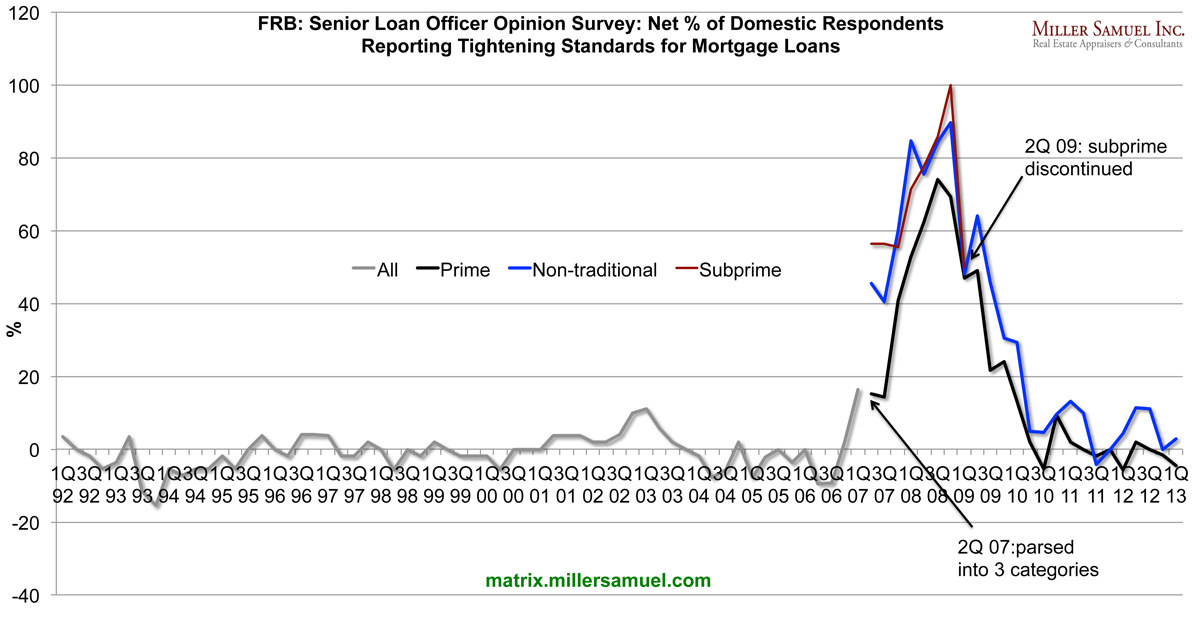

Tight Credit Is Causing Housing Prices to Rise

read more

February 5, 2013

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Humor or Whimsy

,

Law, Ethics & Fraud

,

New York Times

Talking Heads: Burning Down The House, S&P Style

read more

January 28, 2013

Economy

,

Homebuying Process

,

Housing Indices & Portals

,

Language, Jargon & Quotes

,

New York Times

,

RealtyTrac

Falling Inventory Has Created a Housing “Pre-Covery,” not “Recovery”

read more

January 28, 2013

Affordability, Affordable Housing

,

International

,

New York Times

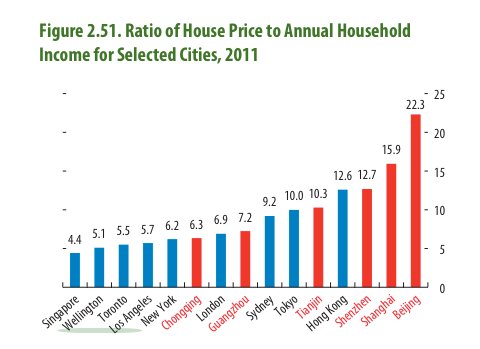

In the Context of Income, New York Prices Housing Prices are a Steal

read more

January 27, 2013

Adventures in Media & Marketing

,

Appraising

,

Brokers, Agents, MLS, NAR

,

New York Times

Broken Appraisal: Lack of Market Knowledge Overpowers Lack of Data

read more

Previous

2

3

4

Next

Load More Posts

Page load link

Go to Top