Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› IRS

October 4, 2015

Appraising

,

Brokers, Agents, MLS, NAR

,

IRS

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Law, Ethics & Fraud

Multi-millionaire Motivational Speaker Dean Graziosi Shares His Appraisal Wisdom

read more

April 28, 2014

Brokers, Agents, MLS, NAR

,

Charts, Maps, Images, Infographics, Video

,

Housing Indices & Portals

,

Housing Trends & Cycles

,

IRS

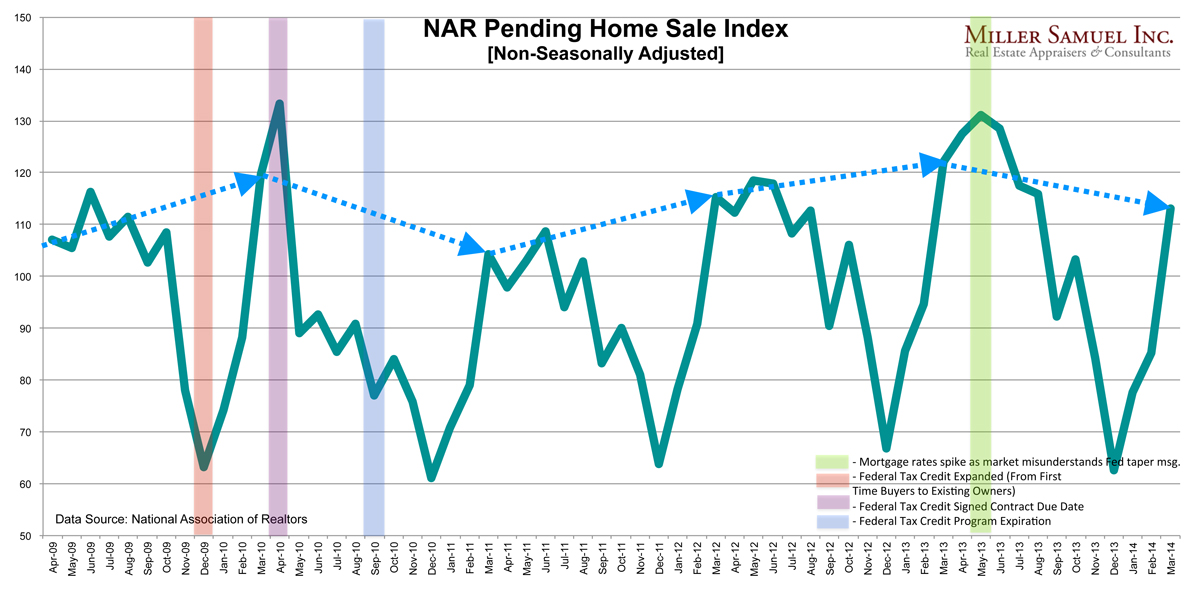

NAR Pending Home Sales Had Biggest “February to March” Jump in 4 Years

read more

March 5, 2014

Government, Politics, Regulations & Policy

,

Housing Trends & Cycles

,

IRS

,

Language, Jargon & Quotes

,

Manhattan

,

New York Times

,

Philadelphia

,

Suburban, Urban, Commuting

Is Gentrification a Four Letter Word?

read more

February 25, 2014

Credit, Finance, Mortgage, Rates

,

Curbed

,

IRS

,

Manhattan

,

Rentals, Investing

,

Sales

[Three Cents Worth #260 NY] Looking At Manhattan’s Mortgage History

read more

May 13, 2013

Douglas Elliman

,

Elliman Reports

,

Hamptons/North Fork

,

IRS

,

Taxes, Insurance, Fees

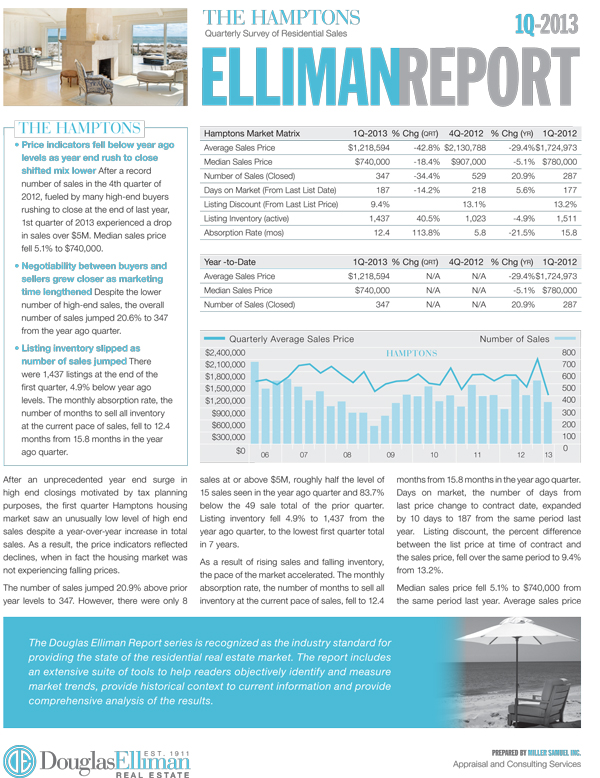

[No Fiscal Cliff Hangover] 1Q 2013 Hamptons & North Fork Reports

read more

May 13, 2013

Douglas Elliman

,

Elliman Reports

,

IRS

,

Long Island

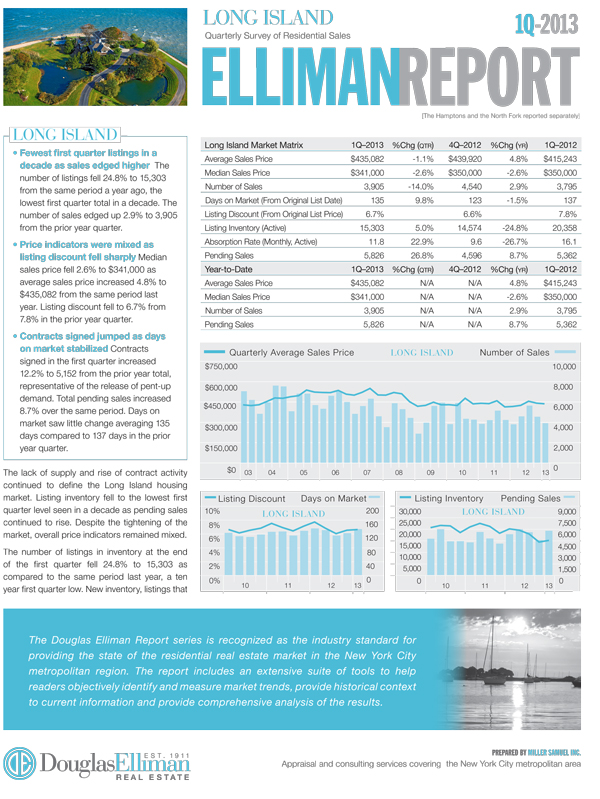

[Defined by Low Supply] 1Q 2013 Long Island Sales Report

read more

April 2, 2013

Douglas Elliman

,

Elliman Reports

,

IRS

,

Manhattan

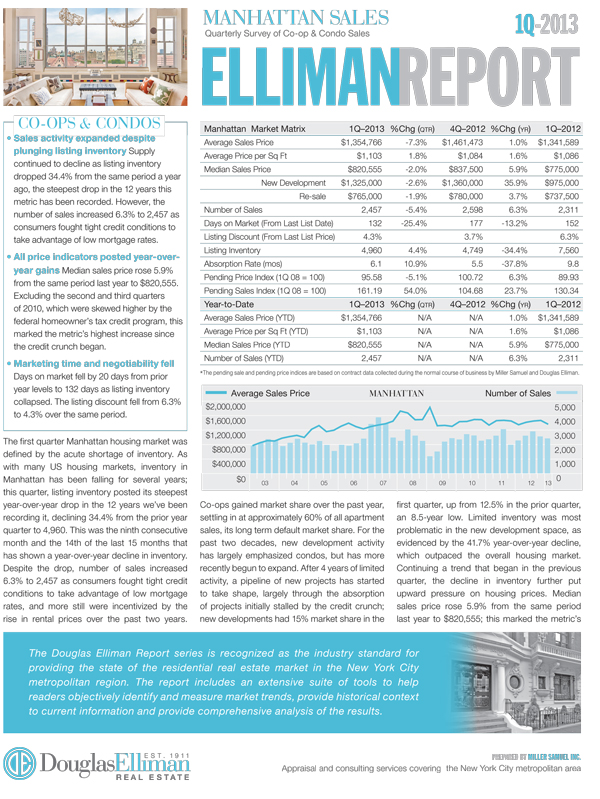

[Inventory Collapse] 1Q 2013 Manhattan Sales Report

read more

January 25, 2013

Douglas Elliman

,

Elliman Reports

,

IRS

,

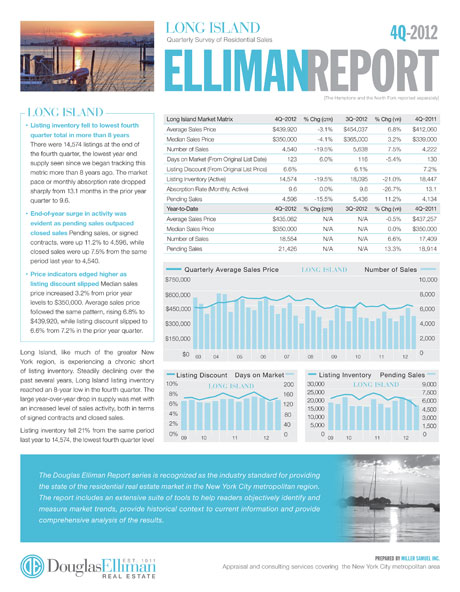

Long Island

[Turning Corner?] 4Q 2012 + 2003-2012 Long Island Decade Reports

read more

June 7, 2012

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

IRS

‘Defensibility’ of Property Values [Part II of Trilogy]

read more

June 23, 2010

Government, Politics, Regulations & Policy

,

IRS

,

Market Reports

[FHFA] U.S. Monthly House Price Index Up 0.8% M-O-M, Down 12.8% From Peak

read more

June 22, 2010

Brokers, Agents, MLS, NAR

,

Distressed Housing

,

IRS

,

Market Reports

,

Wall Street Journal

[NAR] Existing Home Sales Decline 2.2%, But a ‘Northeaster’ Weighed Down the Results

read more

June 21, 2010

IRS

,

Market Reports

,

Washington DC

[CoreLogic] Home Price Index 2.6% YOY and 0.8% MOM Increase

read more

1

2

Next

Load More Posts

Page load link

Go to Top