Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› New York City

August 19, 2020

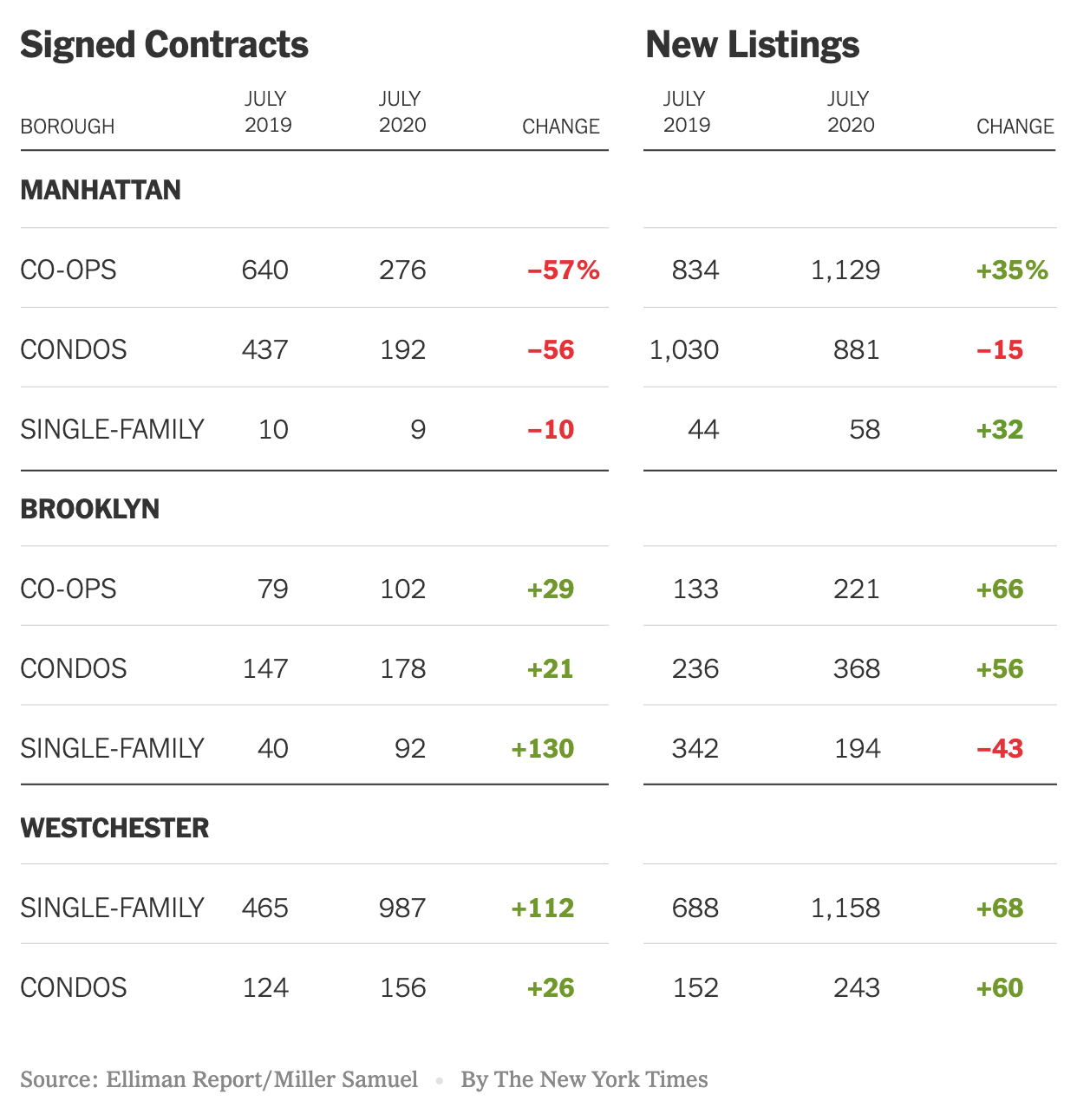

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Elliman Reports

,

Housing Note

,

Housing Trends & Cycles

,

Manhattan

,

New York Times

,

Westchester County, NY

The ‘Urban To Suburban’ Narrative Is Really ‘Manhattan To Suburban’

read more

July 7, 2020

Affordability, Affordable Housing

,

Housing Trends & Cycles

,

Manhattan

,

New York City

[Spectrum TV/NY1] Stuy Town Vacancies Surge 7/6/20

read more

July 6, 2020

Analysis & Research

,

Bloomberg TV

,

Charts, Maps, Images, Infographics, Video

,

Elliman Reports

,

Housing Trends & Cycles

,

New York City

[Bloomberg TV] Bloomberg Markets 7-6-20: A Busy Housing Market This Summer

read more

June 28, 2020

Brokers, Agents, MLS, NAR

,

Explainer

,

Housing Trends & Cycles

,

New York City

,

Op-Ed

My Forbes Column: Keeping Housing Market Results From The Public Is Never Justified: An Expansive View

read more

May 20, 2020

Housing Trends & Cycles

,

New York City

,

New York City Suburbs

,

New York Times

,

Public Speaking

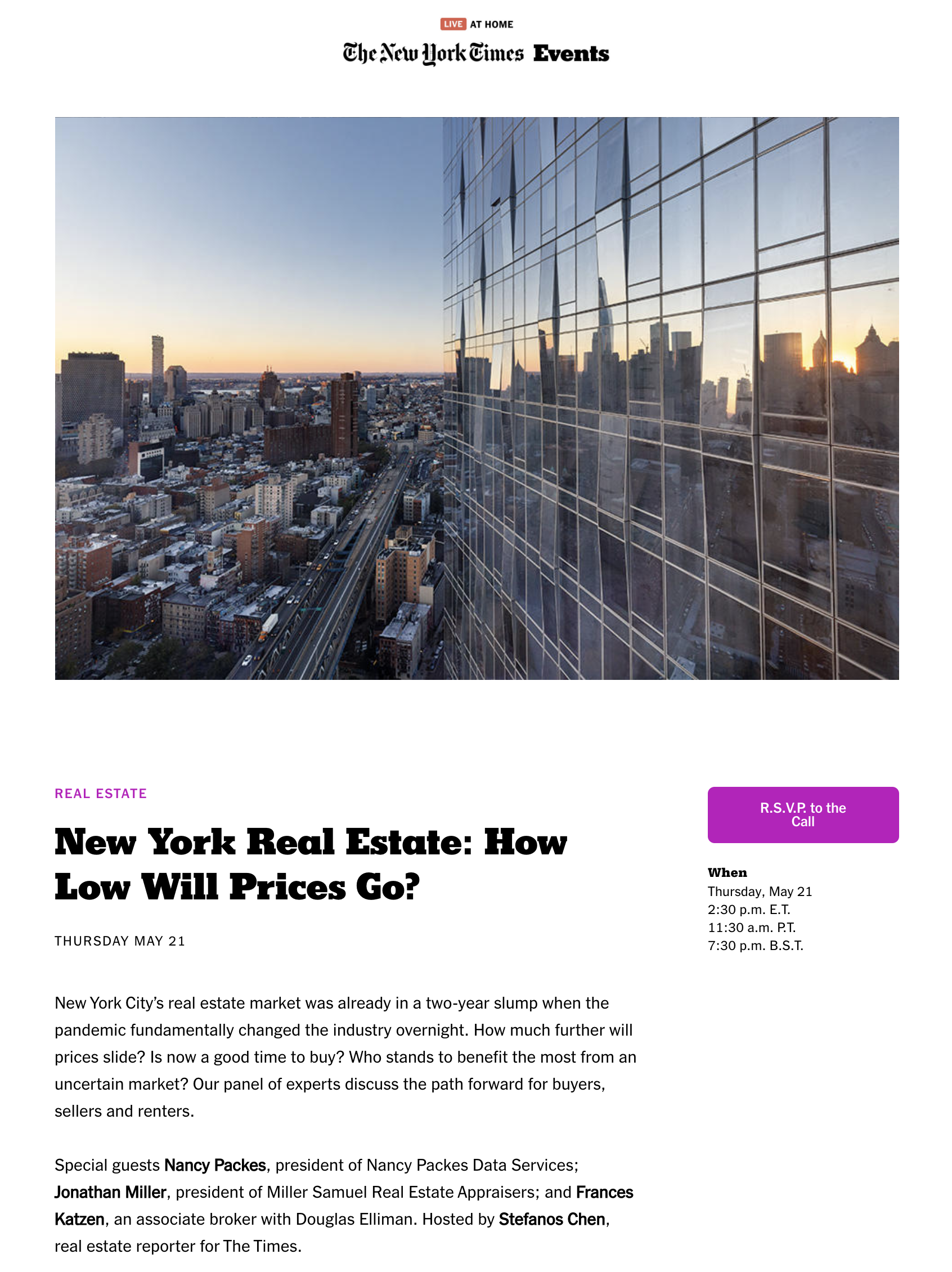

NYT Real Estate Event May 21st @2:30 E.T. New York Real Estate: How Low Will Prices Go?

read more

May 20, 2020

Charts, Maps, Images, Infographics, Video

,

Dutchess County, NY

,

Government, Politics, Regulations & Policy

,

Hamptons/North Fork

,

Manhattan

,

New York City

,

Putnam County

,

Weather & Natural Disasters

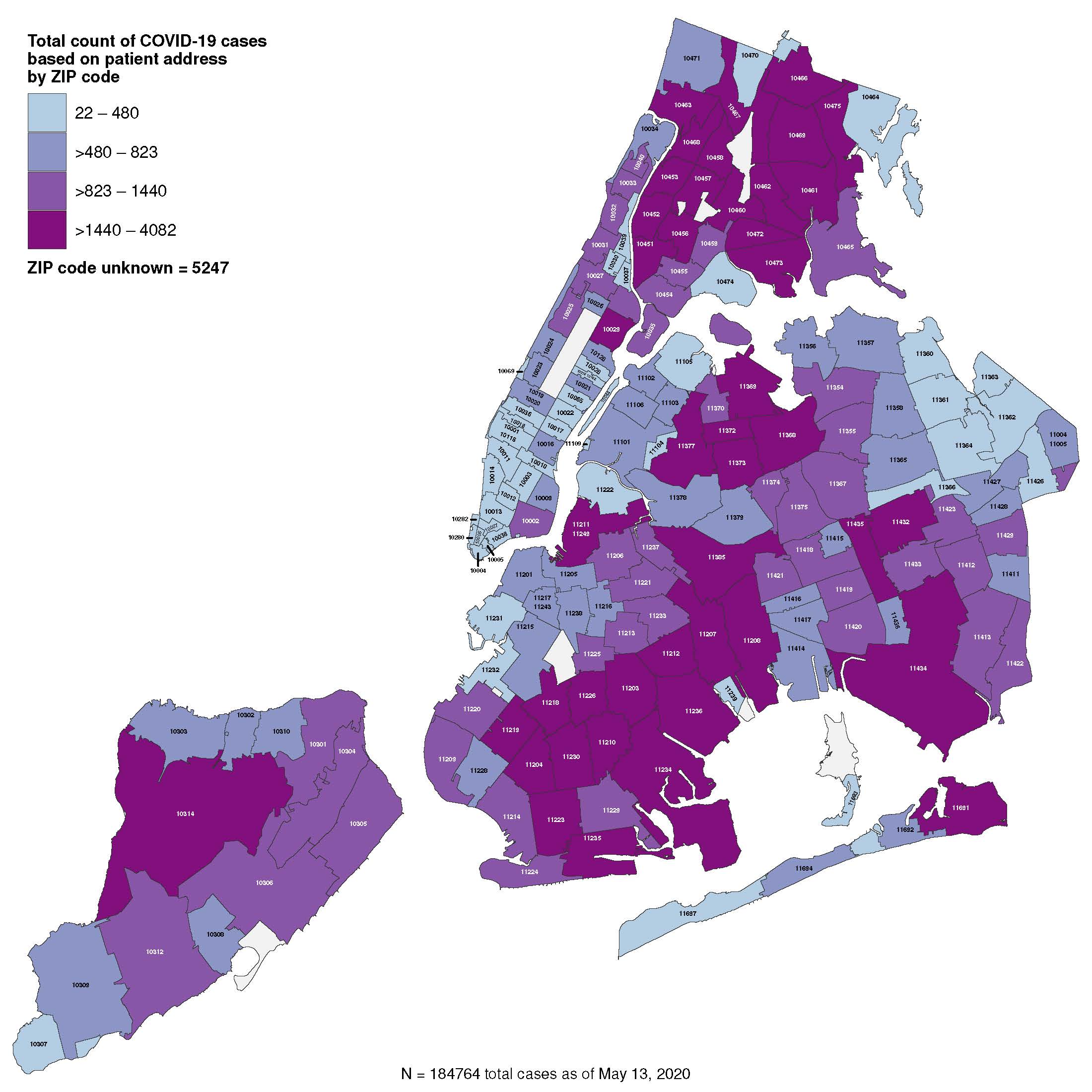

The Overstated COVID-19 Blame on Urban Density in Favor of Suburban Living

read more

May 7, 2020

Charts, Maps, Images, Infographics, Video

,

Distressed Housing

,

Historical, Landmark, Milestone

,

Manhattan

,

New York Times

,

Weather & Natural Disasters

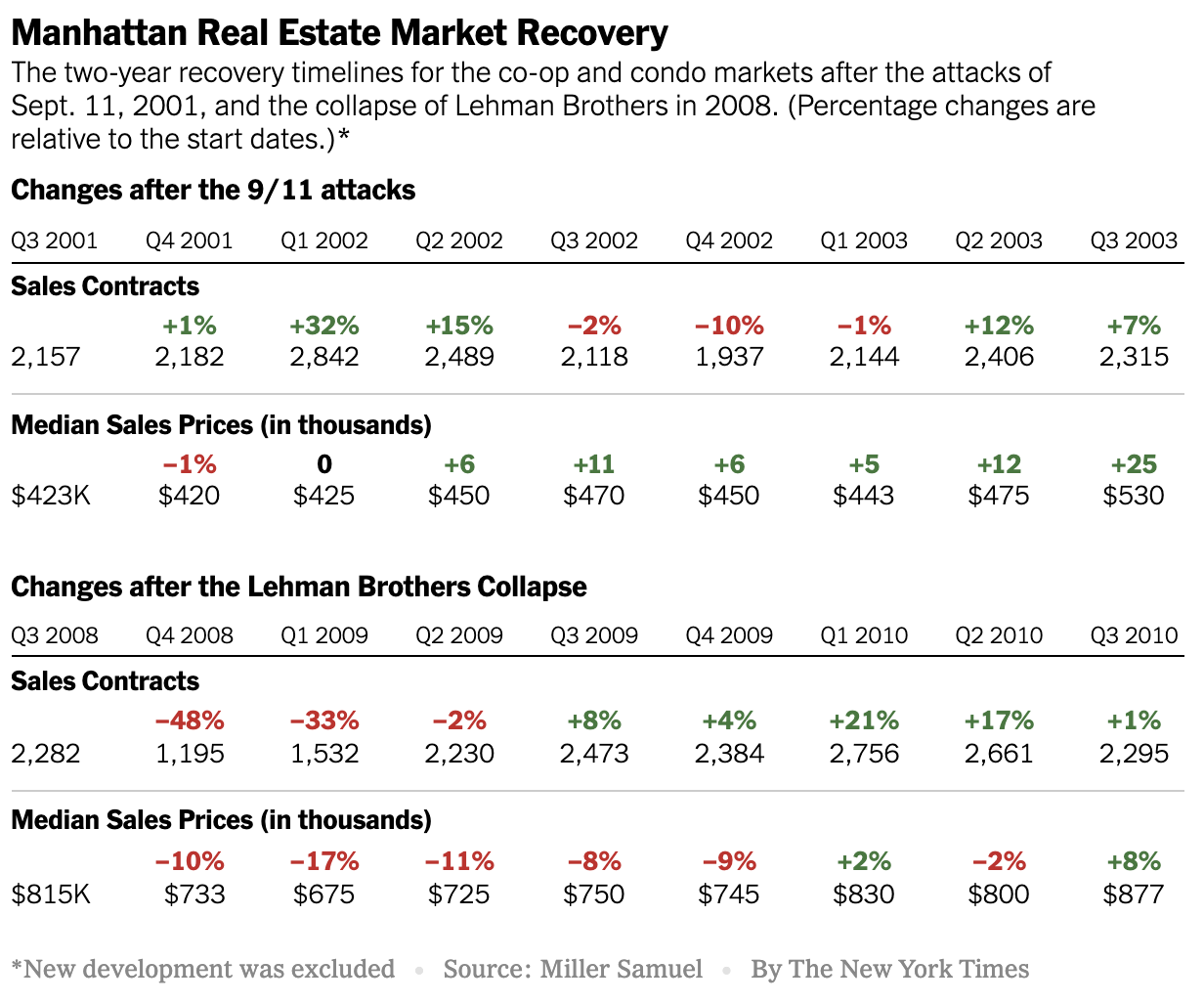

Manhattan Crisis: What Does Our Housing Past Tell Us About Our Housing Future?

read more

May 3, 2020

Government, Politics, Regulations & Policy

,

New York City

,

New York City Suburbs

,

Suburban, Urban, Commuting

,

Weather & Natural Disasters

ABC World News Report 5-2-20 ‘Urban to Suburban’

read more

April 28, 2020

Amenities, Adjustments & Value Logic

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Historical, Landmark, Milestone

,

Housing Note

,

Manhattan

,

Weather & Natural Disasters

Establishing the COVID-19 Demarcation Line: From ‘Hanks To Banks’

read more

April 5, 2020

Bloomberg Radio

,

Bloomberg TV

,

Elliman Reports

,

Housing Note

,

Manhattan

More Bloomberg Media Hits On Real Estate and the Coronavirus

read more

April 2, 2020

Aspen

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Greenwich

,

Los Angeles

,

Manhattan

,

Miami (Beach + Mainland)

Elliman Magazine: 8 Regional Housing Market Charts

read more

February 5, 2020

Charts, Maps, Images, Infographics, Video

,

Government, Politics, Regulations & Policy

,

Manhattan

,

The Real Deal

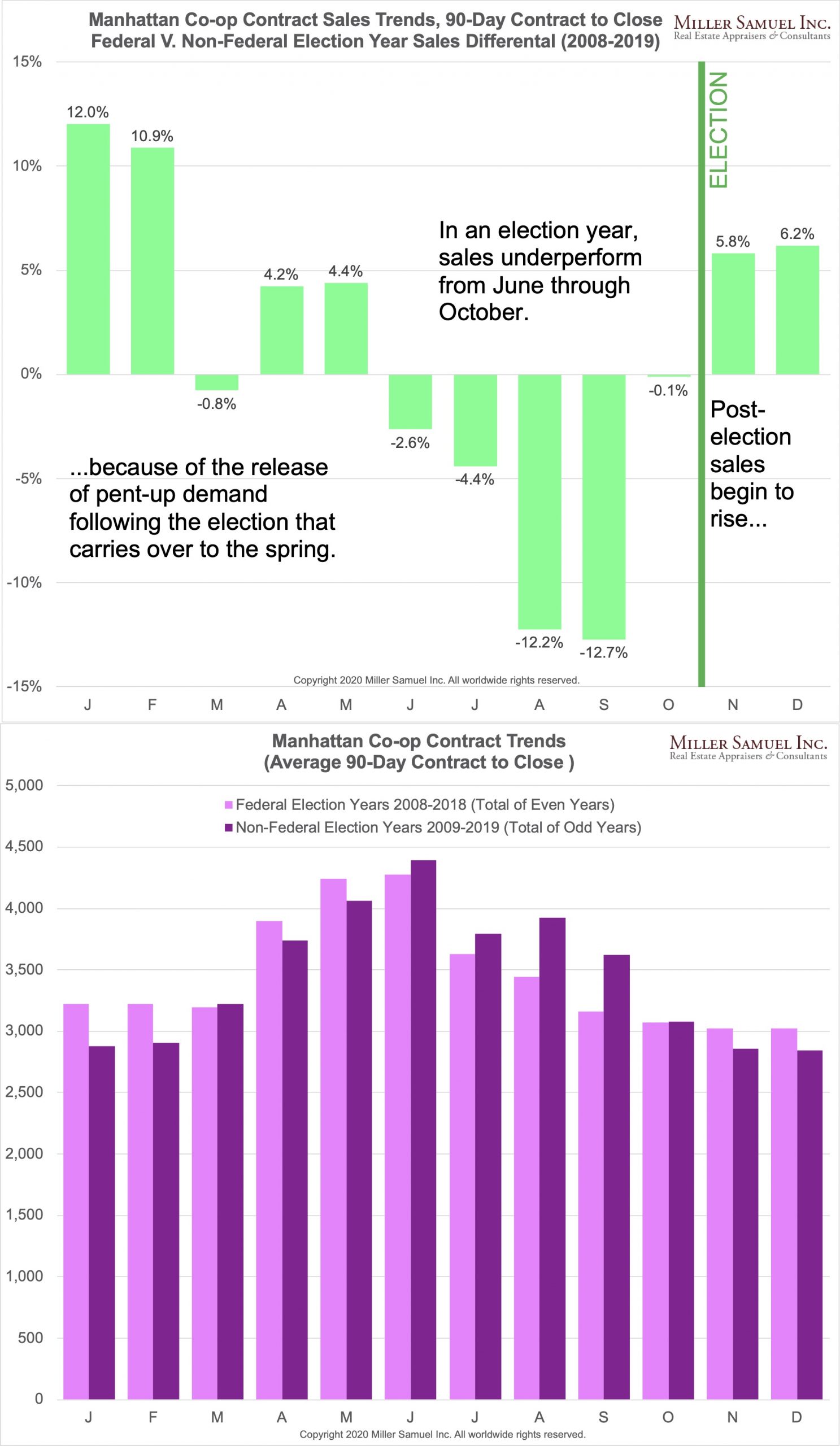

Manhattan Co-op Sales Fall During Federal Election Year

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top