Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› The Real Deal

December 28, 2020

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

The Real Deal

,

Westchester County, NY

TRD Quick Question: Jonathan Miller “What’s Happening in the NYC Real Estate Market?”

read more

February 5, 2020

Charts, Maps, Images, Infographics, Video

,

Government, Politics, Regulations & Policy

,

Manhattan

,

The Real Deal

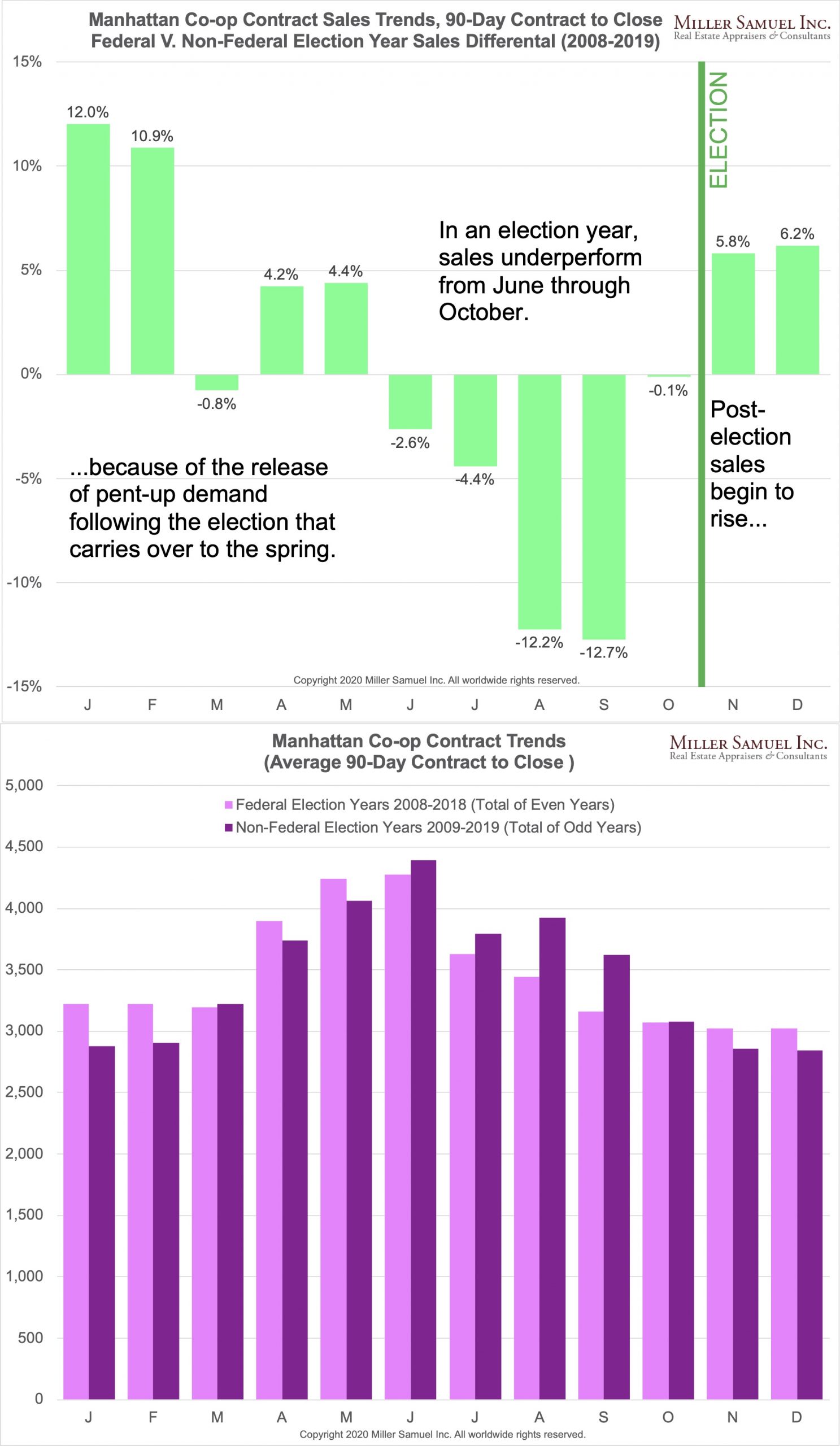

Manhattan Co-op Sales Fall During Federal Election Year

read more

November 27, 2016

China

,

Development, Construction, Architecture & Land

,

International

,

The Real Deal

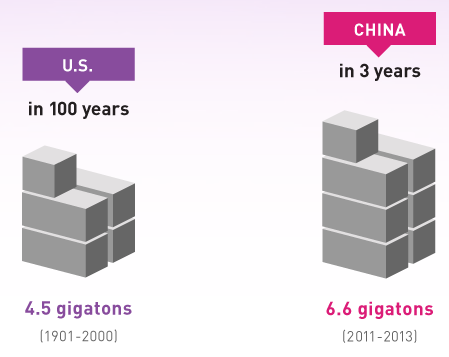

China: A Housing Market Without Re-sales?

read more

May 23, 2014

Brooklyn

,

Development, Construction, Architecture & Land

,

Manhattan

,

New York City

,

Queens

,

The Real Deal

[Video] TRD Forum: Getting A Sense of the New Development Frenzy

read more

May 20, 2014

Development, Construction, Architecture & Land

,

New York City

,

The Real Deal

[TRD] Here’s The New Development Showcase Panel, Including Heckler

read more

May 9, 2014

Manhattan

,

New York City

,

The Real Deal

[Panelist] May 15 – The Real Deal’s New Development Showcase

read more

September 25, 2013

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Media

,

The Real Deal

[Video] Talking Housing on CNBC TV’s Street Signs 9-25-13

read more

February 14, 2013

Housing Indices & Portals

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

The Real Deal

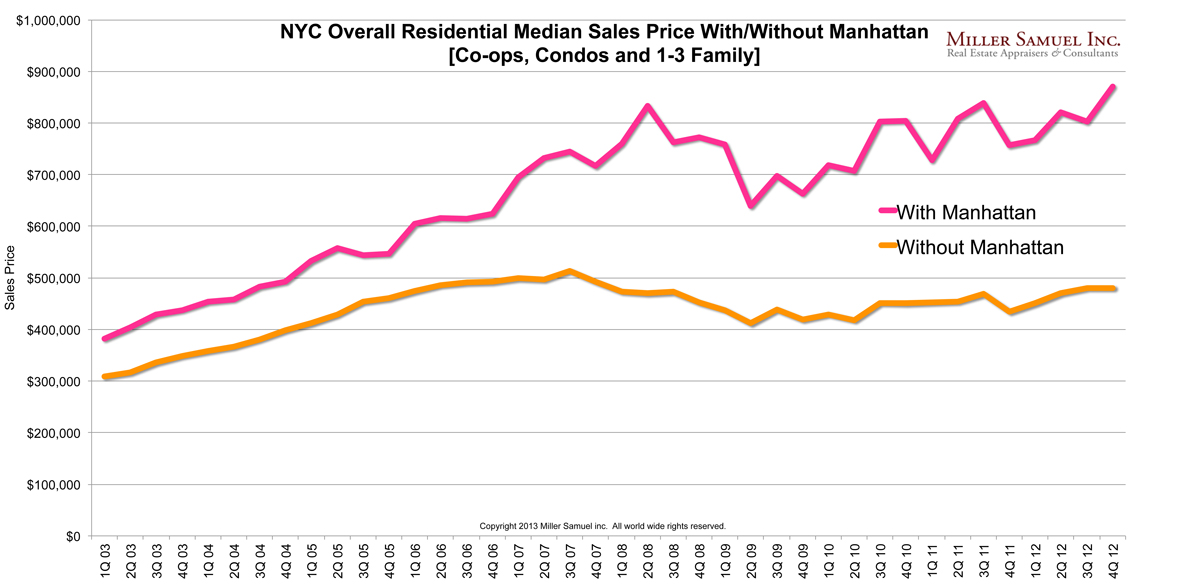

Manhattan Diverged From NYC At US Housing Boom Peak

read more

February 14, 2013

Celebrity, Pop Culture

,

Douglas Elliman

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Housing Indices & Portals

,

RealtyTrac

,

The Real Deal

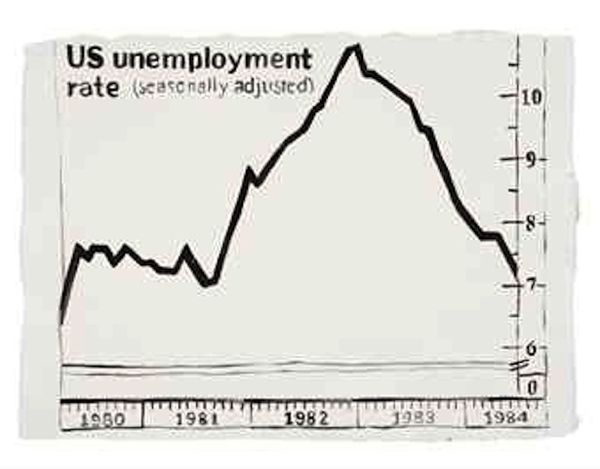

Housing Data as Pop Culture

read more

November 6, 2012

Amenities, Adjustments & Value Logic

,

Appraising

,

International

,

Knight Frank

,

Luxury, Super, Ultra, Mega

,

Market Reports

,

New York Magazine

,

The Real Deal

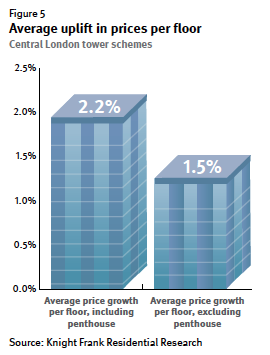

Knight Frank Tall Towers Report Shows London With Similar Manhattan Height Premium

read more

June 14, 2012

Celebrity, Pop Culture

,

Development, Construction, Architecture & Land

,

The Real Deal

Treasures of New York: “Building Stories” Profile of Architect Costas Kondylis

read more

June 9, 2010

Amenities, Adjustments & Value Logic

,

Appraising

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

The Real Deal

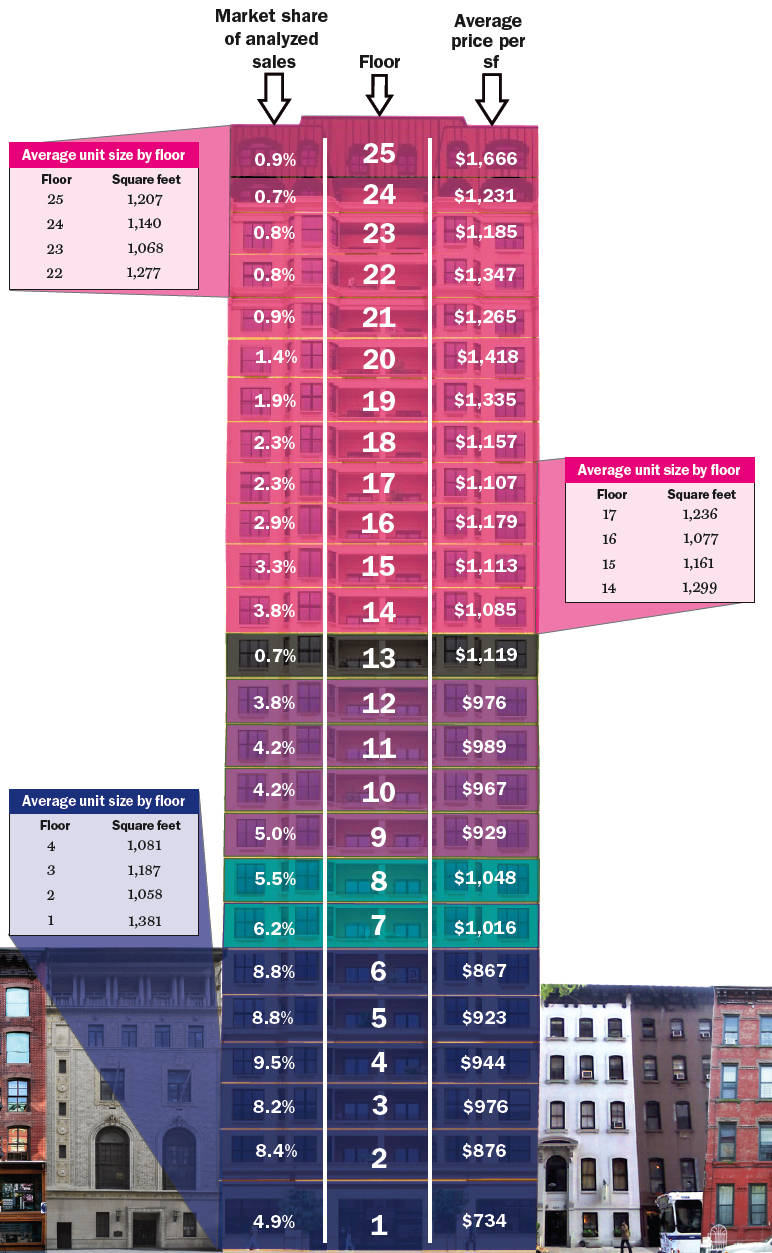

[ChartFloor] Manhattan Price Per Floor Breakdown

read more

1

2

Next

Load More Posts

Page load link

Go to Top