Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Wall Street Journal

December 1, 2015

Charts, Maps, Images, Infographics, Video

,

International

,

Market Reports

,

New York City

,

New York Times

,

Rentals, Investing

,

Wall Street Journal

NYT v. WSJ Smogdown: Status of Chinese Investment in U.S. Real Estate

read more

October 8, 2015

Brooklyn

,

Douglas Elliman

,

Dutchess County, NY

,

Elliman Reports

,

Manhattan

,

Putnam County

,

Queens

,

Wall Street Journal

,

Westchester County, NY

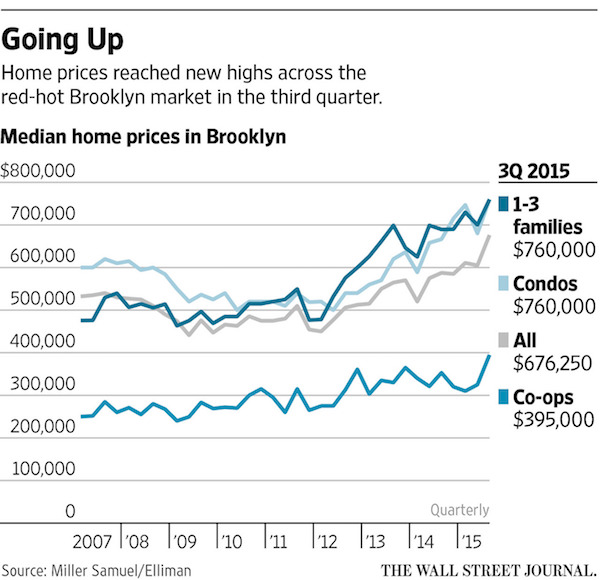

Brooklyn, Queens Set Records, NYC rents jump, Westchester, Putnam and Dutchess Get Busy

read more

July 30, 2015

Brooklyn

,

Development, Construction, Architecture & Land

,

New York City

,

Wall Street Journal

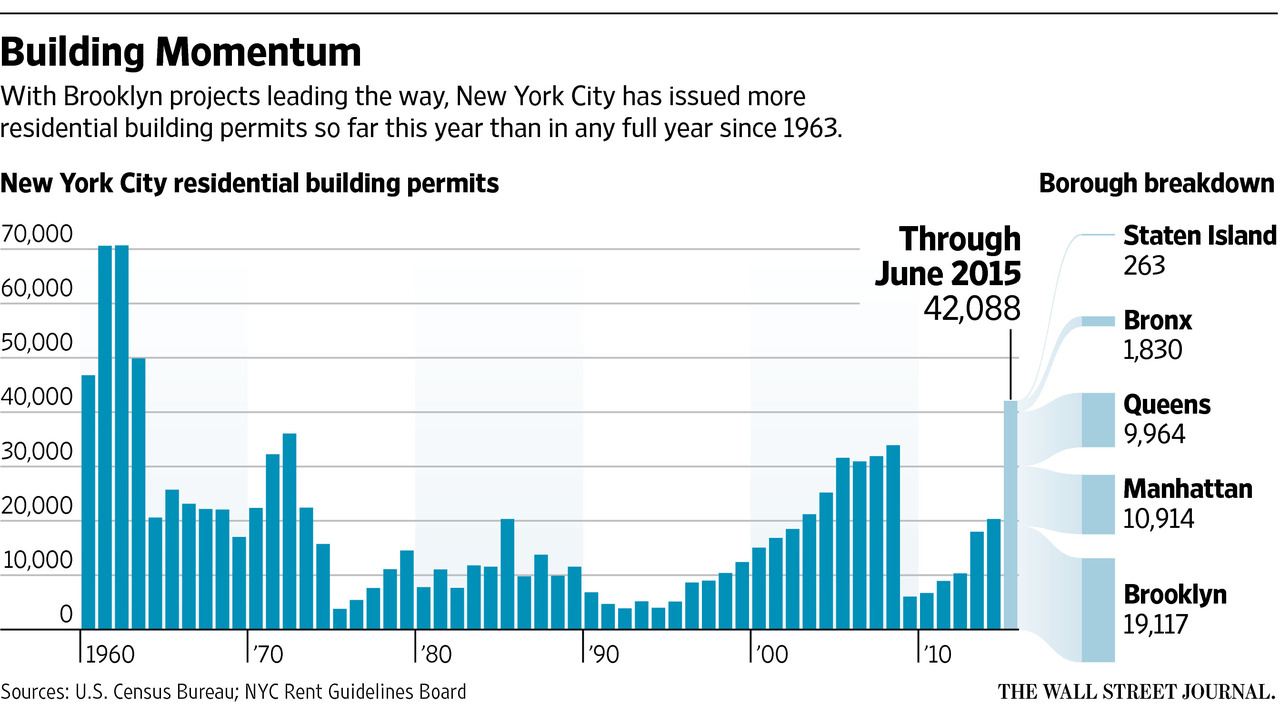

Most NYC building permits since ’63 – Brooklyn nearly equals rest of city

read more

May 4, 2015

Affordability, Affordable Housing

,

Economy

,

Luxury, Super, Ultra, Mega

,

Migration, Psychology, Demographics

,

Rentals, Investing

,

Wall Street Journal

[Video] Why The Rich Get Richer

read more

June 28, 2014

Amenities, Adjustments & Value Logic

,

Brokers, Agents, MLS, NAR

,

Celebrity, Pop Culture

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Records, Thresholds and Outliers

,

Wall Street Journal

Cluttering Luxury Housing Markets with Listings Made for TV – Manhattan Edition

read more

June 23, 2014

Affordability, Affordable Housing

,

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Wall Street Journal

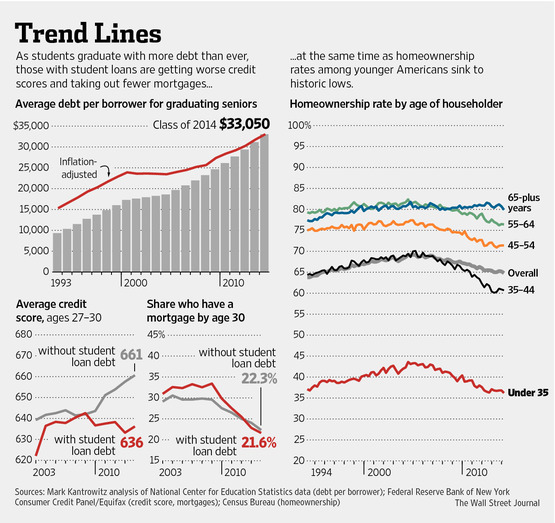

Terrific Chart on Homeownership by Age

read more

March 27, 2014

Economy

,

International

,

Manhattan

,

Rentals, Investing

,

Wall Street Journal

,

Wall Street, Financial Services

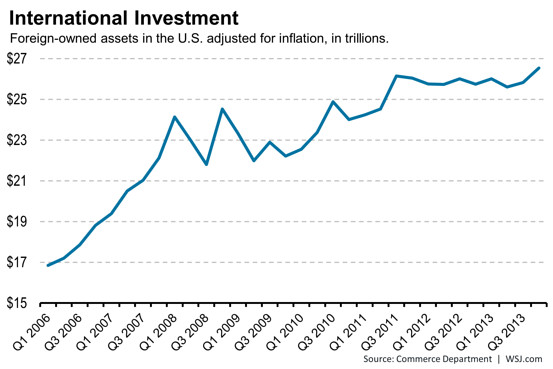

New Record of Foreign-owned Assets in the United States

read more

March 19, 2014

Housing Trends & Cycles

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Migration, Psychology, Demographics

,

Wall Street Journal

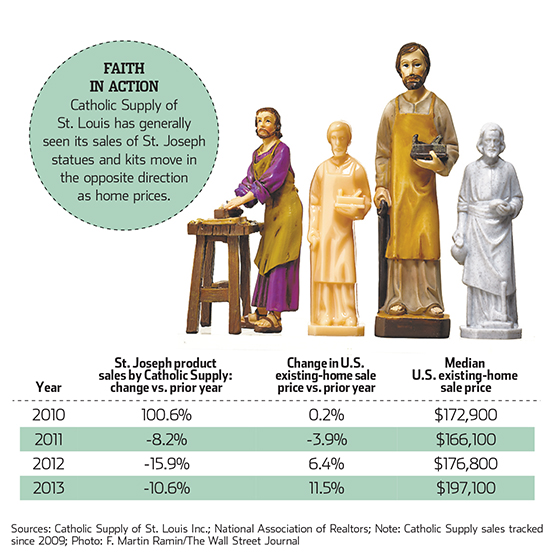

It’s St. Joseph’s Day – What Does It Tell Us About Housing Trends?

read more

March 17, 2014

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Wall Street Journal

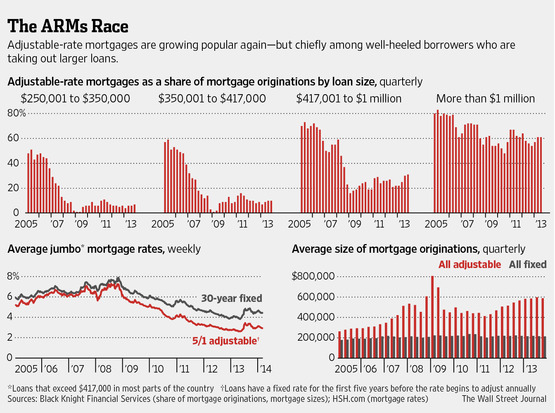

With Plunge in Loan Volume, Lenders Push ARMs to Jumbo Borrowers

read more

March 16, 2014

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Op-Ed

,

Wall Street Journal

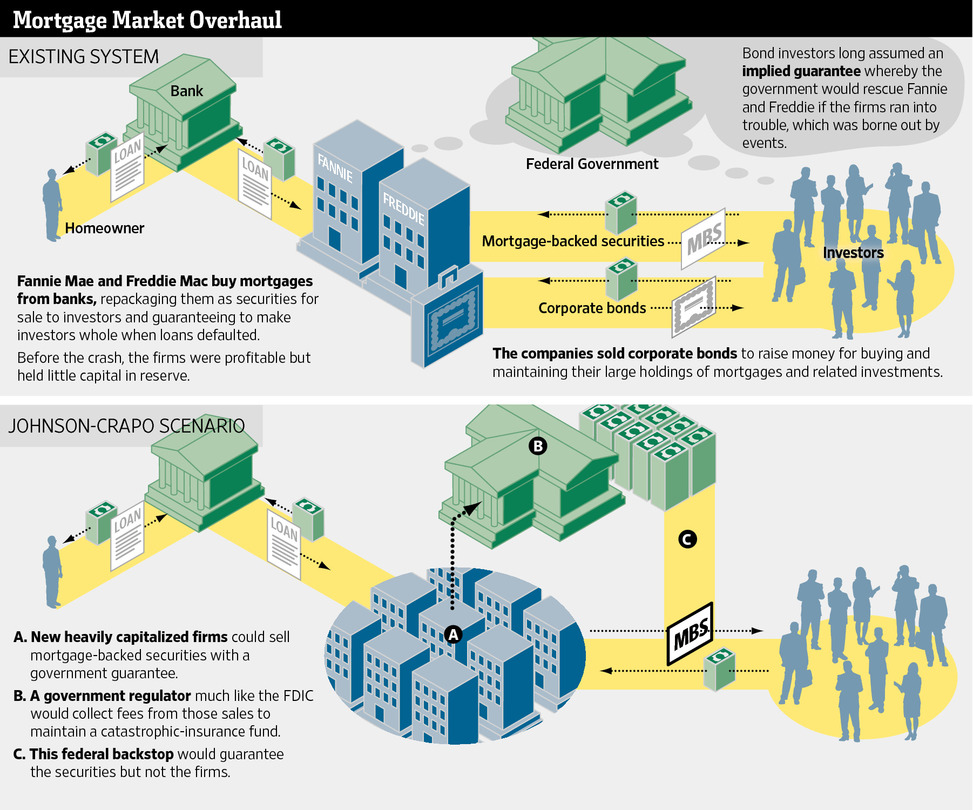

The Bi-Partisan Fannie and Freddie Solution That Isn’t A Fix

read more

February 26, 2014

Housing Trends & Cycles

,

Language, Jargon & Quotes

,

Market Reports

,

Trulia

,

Wall Street Journal

[WSJ] Good Overview on 2014 US Housing Expectations – Jed Kolko, Trulia

read more

February 4, 2014

Canada

,

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Wall Street Journal

,

Weather & Natural Disasters

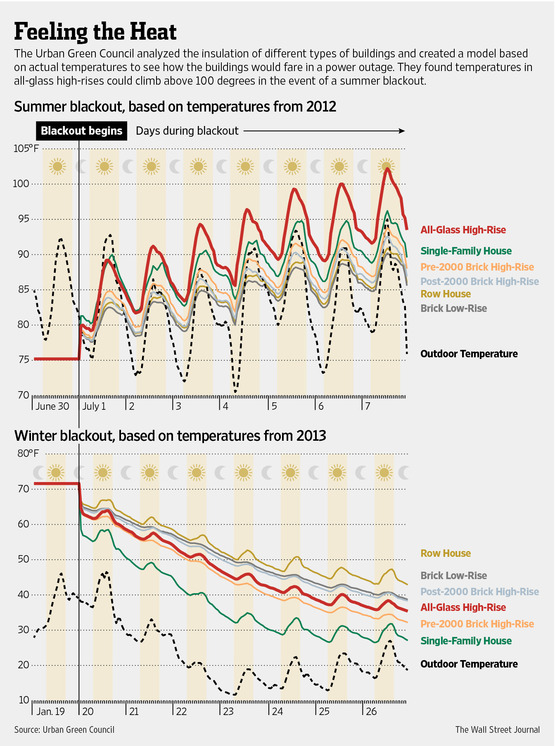

Group Claims Glass Curtain Walls “A Major Step Backward Environmentally”

read more

1

2

Next

Load More Posts

Page load link

Go to Top