_Getting Graphic is a semi-sort-of-irregular collection of our favorite BIG real estate-related chart(s)._

In 1996, when the imputed rent replaced sales trends in the CPI calculation, the government provided evidence that this would have little impact on CPI. However, in Floyd Norris’ column this week [What Happens if Inflation Is Overstated? [NYT]](http://select.nytimes.com/2006/06/09/business/09norris.html), he shows that things have changed considerably since then.

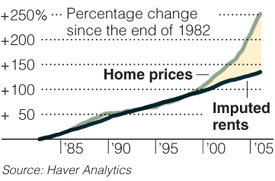

* Sales have doubled

* Rents have increased by a third

I commented about this last February in the post [At The Core Of Inflation, Housing Sales Are Merely Rentals](http://matrix.millersamuelv2.wpenginepowered.com/?p=436).

There is the belief that inflation was understated because rentals were weaker than sales during the housing boom and quite possibly the Fed may have been quicker to raise rates to cool off the market. Now with the rental market expected to grow, inflation may be over stated.

>Higher interest rates might weaken the economy, but could also help the dollar. Lower rates could hurt the dollar, but also strengthen the economy.

>Flexibility may be essential. “If Bernanke commits categorically to a response to core price pressures,” said Robert J. Barbera, chief economist of ITG, “he could find himself raising rates because housing does worse because of the arithmetic of how that plays out in the C.P.I.”

Bernanke may find that making the Fed more transparent, may be easier said than done and Norris concludes that _Mr. Bernanke may come to understand why Mr. Greenspan so rarely said anything clearly._

5 Comments

Comments are closed.

Hi.

Could you ask the Federal Reserve to figure it all out, and quickly?

I need buyers. Like, now.

Hi Jonathan,

I love your analysis & graphics. I have a post on the same topic: How Much Will the Housing Market Fall?. Assuming the same affordability, I calculated the amount of fall by assuming different loan scenarios.

frugal

John K, this is a general response to an imaginary real estate agent. It is inspired by your plea, but really reflects the Stony Brook area in Suffolk county. Your situation is almost certainly different. You are probably a home owner in Queens and will laugh at loud at the irrelevance of my comments below.

No, you don’t need a buyer. When you need a buyer, you will drop your house prices dramatically and change real estate commission structures.

House prices are already dropping, but median prices don’t seem to have hit 3 times median income yet. I think the old rule of thumb was 2.5 times income. But, everybody keeps telling me Long Island is a nice place to live, so let’s use 3. I can still rent for about the cost of owning (including tax breaks, but not including maintenance, closing costs, costs to resell the house when I want to move, and a real risk of price declines).

Commission splits are 2% for selling broker, 1% for buying broker. That’s not really my problem, but I thought it was an significant sign that buyers are still not too hard to find.

Yes, inventory is staggeringly high, but I have yet to see much serious money being put into attracting buyers. Sellers won’t even spend a few thousand to entice agents with buyers, leave alone the 30% price drop that would sell the house in days instead of months (quarters?, years? with 10 months inventory, I am not sure of the right units for time).

As for the Federal Reserve, what can they do? Mortgages are long term (they used to follow the 30 yr. T Bill). The Fed controls short term rates. Massive inflation in wages with stagnant prices may bring house prices in line, but even that may not work since the accompanying mortgage interest rates will keep costs too high for most.

Thanks for the tips. I’m actually a real estate agent, working only with buyers, and I haven’t had a warm body at my door, for months. I agree, housing prices will need to come down to get buyers back on the street – partially because of the high prices, but more so because of the rising interest rates, making the purchases even more unaffordable.

I don’t agree with your estimate of what housing should cost. To me, it’s all a matter of monthly mortgage loan payment, not a multiplier of income.

Sure it matters. If the Fed has taken a “wait until the data comes in” position and they are relying on skewed information, then it has a direct impact on mortgages if the fed chooses to raise rates for the wrong reasons.