[click to expand]

[click to expand]

Thoughts

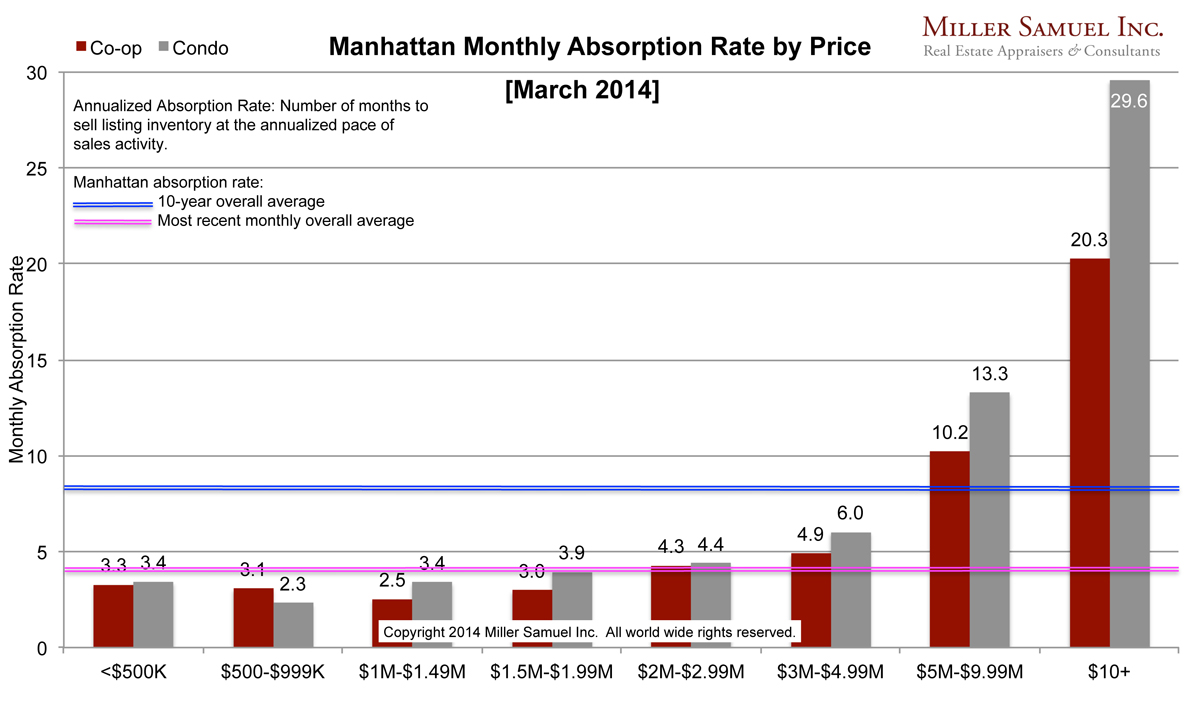

All price segments of the market are generally showing a faster market pace than the same month in the prior year. The top 1% ($10M+) had slower absorption rates for co-ops and condos, but not by much. Inventory began to “bottom” in recent quarters so we may not see much more compression in the market pace in the coming months.

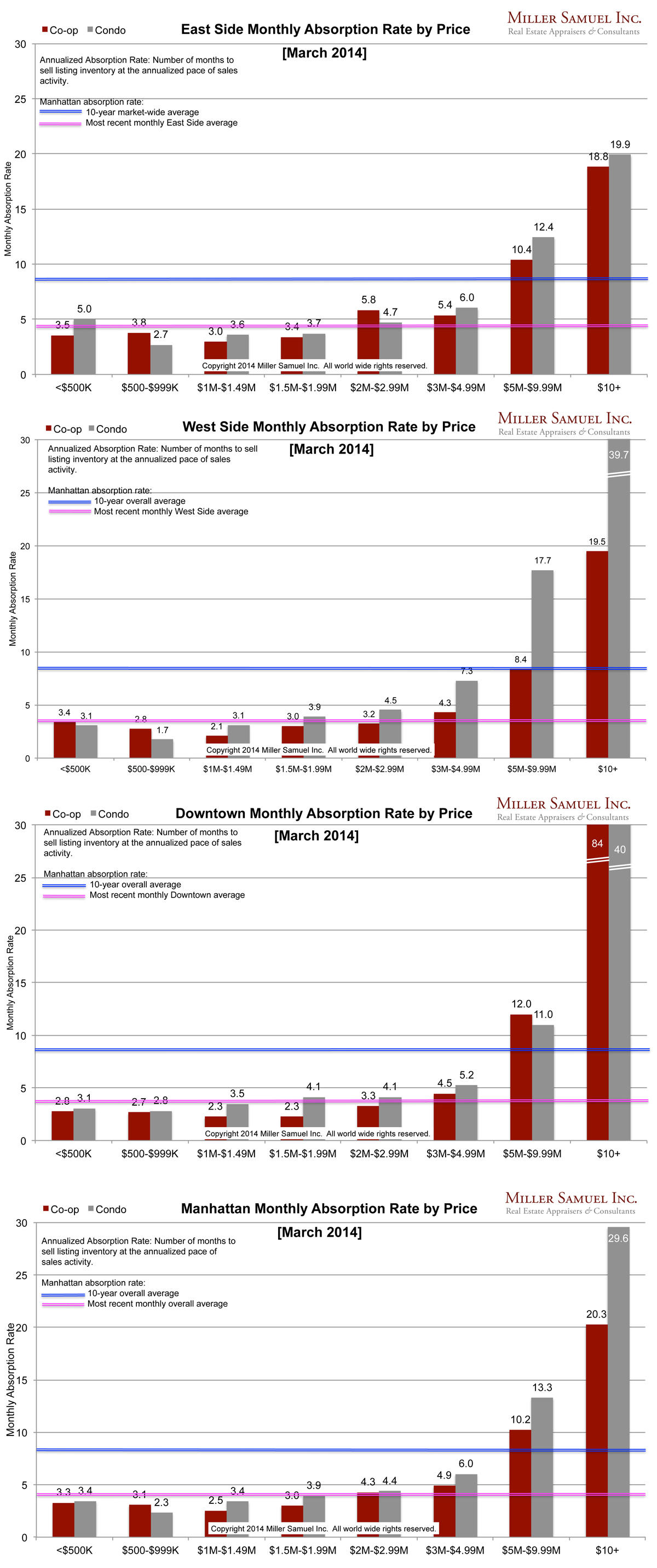

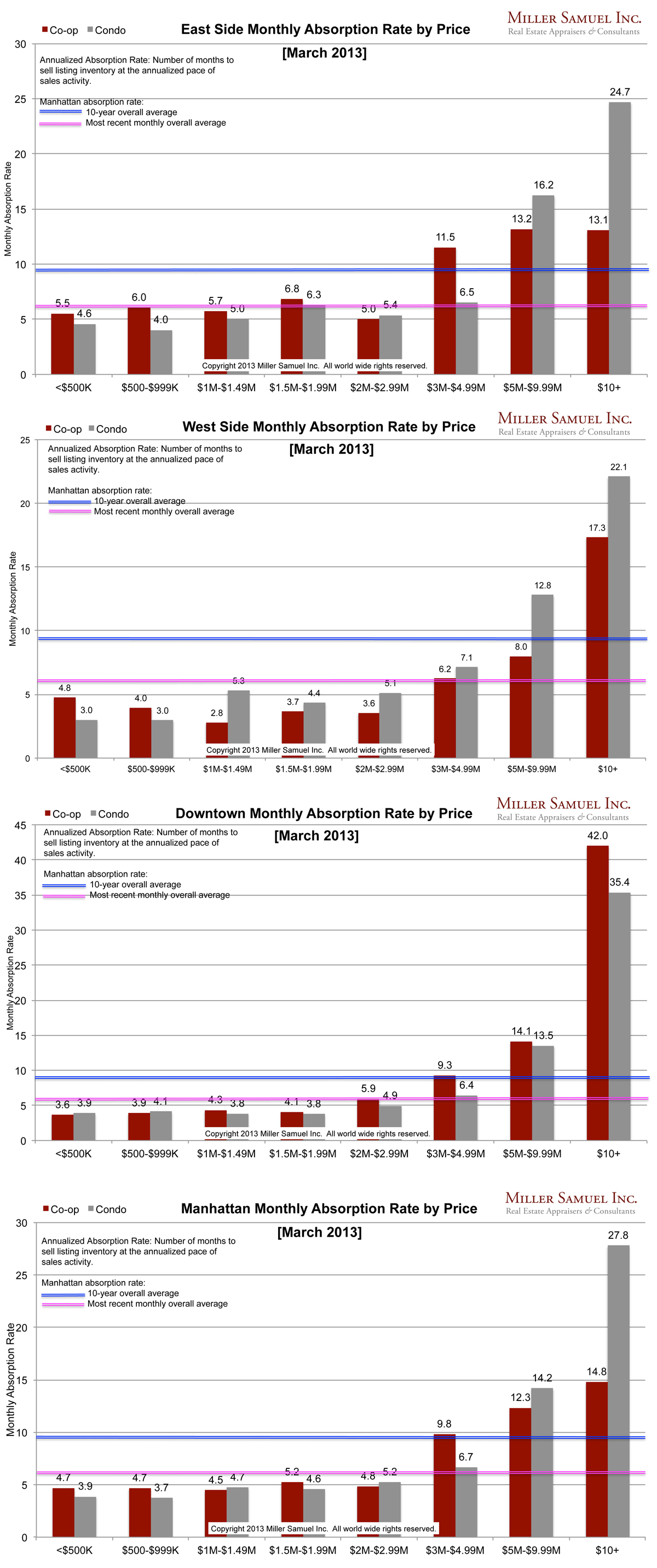

Side by side Manhattan regional comparison:

[click images to expand]

[click images to expand]

I started this analysis in August 2009 so I am able to show side-by side year-over-year comparisons. The blue line showing the 10-year quarterly average travels up and down because of the change in scale caused by some of the significant volatility seen at the upper end of the market. The pink line represents the overall average rate of the most recently completed month for that market area.

Definition

Absorption defined for the purposes of this chart is: Number of months to sell all listing inventory at the annual pace of sales activity. (The definition of absorption in our market report series reflects the quarterly pace – nearly the same)

_______________________

Manhattan Market Absorption Charts [Miller Samuel]