![]()

Over the past few days I’ve been sent this blog post by a number of real estate appraisers who are upset with its derogatory reference to our profession. It was written by Dean Graziosi in the Huffington Post guest blogger section. I’ve never heard of him but perhaps that’s because I’m not a real estate agent. If you insert the word “scam” in your google search, there are a lot of additional insights that come up.

His Huffpost bio and web site indicates he is a NY Times Best Selling Author along with one of the top personal motivation and real estate trainers in the world. I also learned from his bio that he is a multi-millionaire, a guru in the personal motivation sector and cares deeply about his students. Translation: He basically teaches real estate agents how to sell.

Good. While it’s not my thing, I’m happy for Dean’s success (notice how his watch is strategically placed within his Facebook head shot as an indirect confirmation of his success) assuming no one was hurt. However as a public figure (as indicated on his Facebook page with 340K+ likes), Dean has a responsibility to convey information accurately to his students if he does indeed care.

While I doubt he wrote it it personally, his brand handlers managed to mischaracterize two key issues in a small blog post on HuffPost:

1. Graziosi frames the current housing market as equal to the bubble’s peak but doesn’t accurately describe what that means.

2. Graziosi frames the real estate appraiser as something other than a real estate professional while the real estate agent is a professional.

1. Housing Market

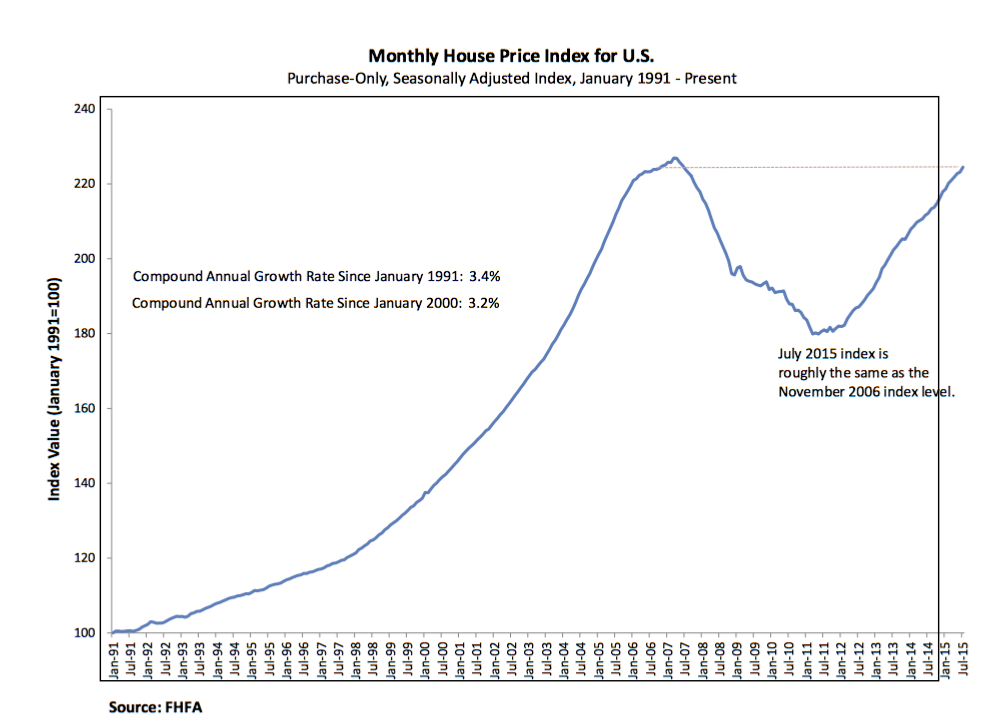

Graziosi cites the FHFA trend line as breaking even with the 2006 peak. Yes, based on FHFA methodology that’s certainly true and taken directly from the most recent FHFA report. I do feel the need to split hairs here since his “brushstroke style” of simplifying everything misaligns with reality. He says:

First, and most important, it requires repeat sales of homes, so if there aren’t huge numbers of sales, then we’re looking at a number derived from a small set of sales data. So, we’re not necessarily seeing an excited bunch of buyers flocking to the market. We are seeing a whole lot of homeowners who aren’t selling, waiting for rising values. So, we have a small inventory and competition for it.

The problem here is that there are a lot of sales outside of FHFA data – and FHFA only tracks mortgages that go through Fannie and Freddie. Roughly 30% of home sales are cash and another 5-10% of them are jumbo loans, too large to be purchased by the former GSEs – so they don’t get included. FHFA also excludes new construction.

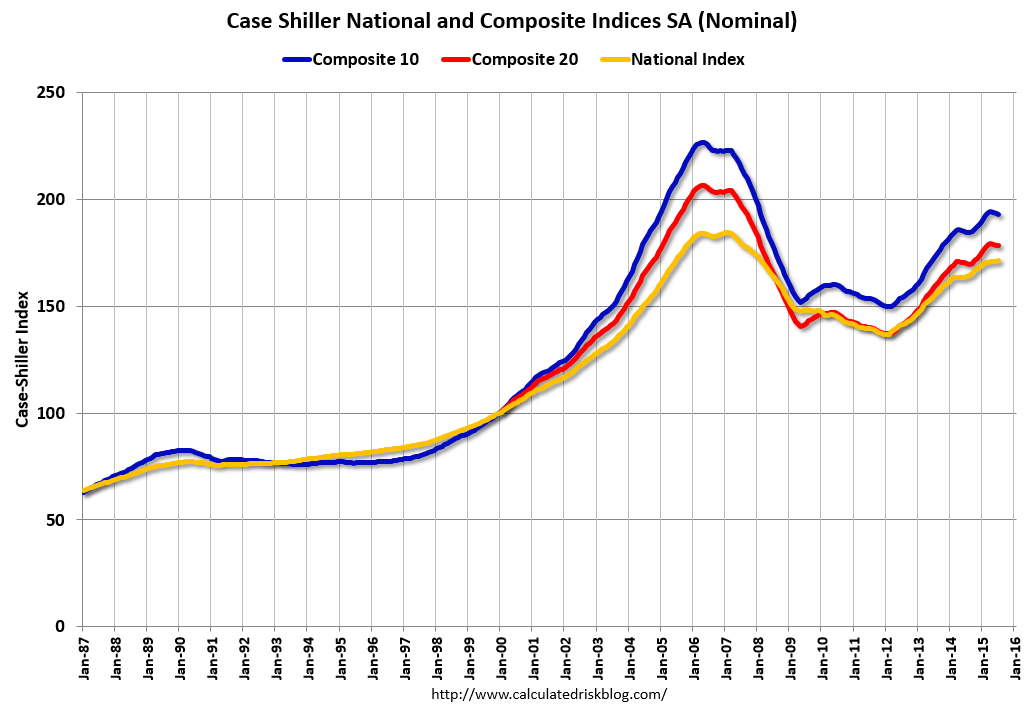

The Case Shiller index is also a repeat sales index like FHFA but shows a different price point for the current market because it includes transactions outside of the GSE world.

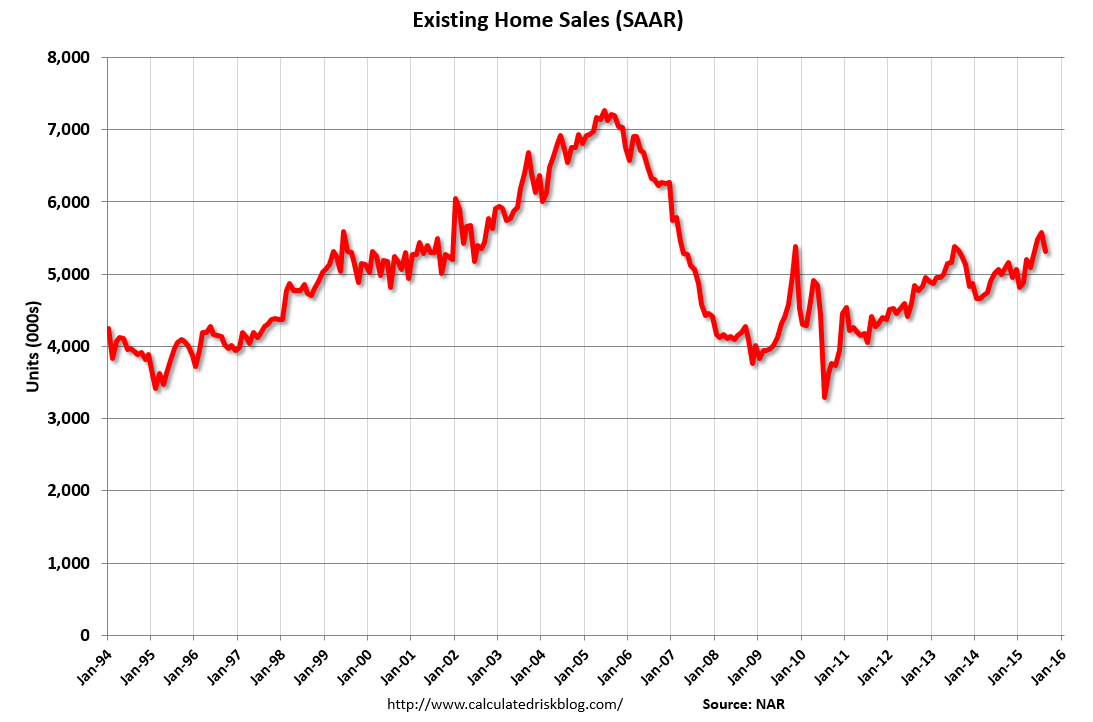

If we look at the number of sales, which is the key point he makes, sales activity is low because we’re not necessarily seeing an excited bunch of buyers flocking to the market. But in reality, home sales are not low and they have been rising for 4 years. Of course sales are not at pre-crash highs because those highs were created largely by fraudulent lending practices including the unethical behavior of consumers caught up in the systemic breakdown that included nearly all particpants in the mortgage process.

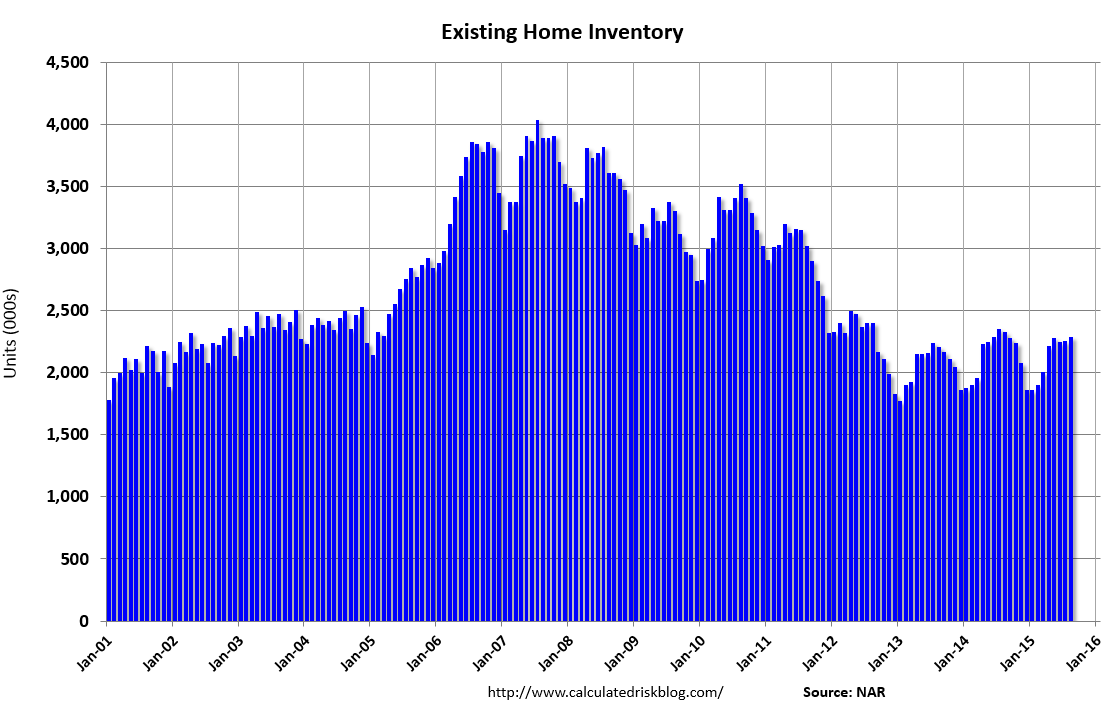

Graziosi is right that inventory is low, but not because buyers aren’t flocking to the market – many buyers are being held back credit access has over-corrected. Many homeowners can’t qualify for the next purchase so there is no point of listing their home for sale.

Conclusion – we are not at the pre-Lehman market peak unless you only look through the eyes off FHFA, a distorted subset of the overall housing market. I would think that real estate gurus understand this.

2. Appraisal Industry

Let’s move on to the real reason I am writing this post.

I can ignore Graziosi’s “lite” market commentary but I can’t ignore his misunderstanding of the appraiser’s role in the purchase mortgage process (buyers applying for a mortgage to purchase a home.)

Don’t call an appraiser, as their approach to market value is different than that of a real estate professional. The real estate agent is trying to get you a sold price near to the top of the market, and their CMA, Comparative Market Analysis, is going to give you a pretty good idea of its value.

There is so much to talk about within these two sentences I’m not sure where to begin. It’s mindbogglingly simplistic, misleading and uninformed. Perhaps this is how he makes his students motivated?

Lets go for the big point first:

“Don’t call an appraiser, as their approach to market value is different than that of a real estate professional.” He must be thinking along the lines of the IRS definition, which is

To meet the IRS requirements, you need two things: spend the majority of your working time spent performing qualified real estate activities (regardless of what you do), and rack up at least 750 hours. Qualified activities include “develop, redevelop, construct, reconstruct, acquire, convert, rent, operate, manage, lease or sell” real estate.

Nary an appraisal-related definition within that list.

The problem with Graziosi’s communication skills as a best selling author and nationally renowned real estate guru who gives seminars for a living to communicate to his students (agents) how to succeed is – if we (appraisers) are not “real estate professionals” then it is a hop, skip and a jump to suggest we are “unprofessional” as if appraisers are something less than a real estate agent. Ask any consumer if they hold real estate agents in higher regard than real estate appraisers? In my view both industries don’t have sterling legacies but one isn’t more professional than another. Remember that he is used to speaking to his students who are real estate agents, the kind that sign up for this type of course. Promote BPOs and help agents get more listings – has got to be his recurring mantra.

The second issue with his quote concerning an appraiser’s value opinions – “their approach to market value is different” than a real estate agent. Providing an opinion of market value is likely the intention of both. Most real estate agents are hoping to get the listing and the appraiser is not incentivized by the home’s future sale. The agent may be the most knowledgeable person in the local market but there is an inherent potential conflict. Graziosi suggests that the broker will give you a price you want to hear. However I do like his idea of getting three broker opinions – that’s a very common practice – nothing new there. Ironically both an agent and an appraiser are looking at closed sales, contracts and listings but the appraiser doesn’t have an inherent conflict. They aren’t going to get the listing no matter how accurate their value opinion proves to be.

One problem with today’s appraiser stereotype as this column brings out indirectly, is that bank appraisers now generally work for appraisal management companies (probably about 90%) and the best appraisers tend to avoid or perform minimal AMC work because they can’t work for half the market rate. As a result, good appraisers aren’t necessarily known as well by the brokerage community as in years passed unless they get in front of the brokerage community in other ways, like giving seminars, public speaking, etc. Competent brokers within a market will know who the competent appraisers are.

There are unprofessional professionals in every industry – doctors, lawyers, deepwater diving arc welders and farmers, so please don’t make sweeping pronouncements to the contrary – especially if you are in the business of communicating information to “real estate professionals”.

Conclusions

• The real estate appraisal industry is not unprofessional

• IRS definition aside, real estate appraisers are real estate professionals

As I’ve walked through this response, I realized that the silly advice blog post in the Huffington Post by an infomercial guy did what it intended, stir up conversations of any type to get his name out there when his actual content was devoid of useful information. There is a great post I stumbled on the industry of motivational speakers:

Real Estate B.S. Artist Detection Checklist. Worth a read.

Looks like I’m never going to be a multi-millionaire wearing a huge watch strategically placed in my head shot. If you notice my own head shot in the righthand column, my watch is very small.

Sigh.

__________________________

UPDATE From the I have no idea for whom the appraisal is being performed but I am a 20+ year real estate professional (see definition above) department: Here’s an article from the Santa Fe New Mexican “Be cautious of appraisals” that damns appraisers using a stunning lack of understanding of the appraiser’s role in the mortgage process given his experience. This piece was written by a mortgage broker who was also a former financial consultant and real estate agent. The author states:

Everyone in every business falls under some measure of accountability. Certainly appraisers must also be accountable to their customer. The customer is the homeowner, not the AMC.

No it isn’t.

The appraiser’s client in the mortgage appraisal situation you describe is not the homeowner. The AMC is acting as an agent for the lender in order to for the lender to make an informed decision on the collateral (of course that’s only a concept). The appraiser is working for the AMC (who works for the lender) and not for your homeowner. Your logic from the housing bubble still sits with you today.

Yes I agree that the quality of AMC appraisals for banks generally stinks, but blame the banks for that, not the appraisers. Quality issues don’t change who the appraiser is working for. AMCs do internal reviews and make ‘good’ appraiser’s lives a living hell for half the prevailing market rate loaded with silly review questions by 19 year olds chewing gum to justify their own institution’s reason for existence. No wonder you are frustrated with appraisers from AMCs. ‘Good’ appraisal firms like mine avoid working for AMCs whenever possible. Yes I would be frustrated as a mortgage broker today because your industry got used to using appraisers as “deal enablers” during the bubble and nothing more. I contend that the current mortgage process post-Dodd Frank is clearly terrible and AMCs are a big part of the problem.

ASIDE This new era of online journalism for print stalwarts like the “Santa Fe New Mexican” and new versions like the “HuffPost” rely on filler-like the above 2 articles discussed here. Very sad.

Comments are closed.