Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Favorites

May 21, 2023

Appraising

,

Government, Politics, Regulations & Policy

,

Washington DC

Three Hours On C-SPAN Yields One Granddaughter

read more

April 7, 2020

Bloomberg News

,

Greenwich

,

Weather & Natural Disasters

Do We Hope This Listing Goes Viral?…No We Don’t.

read more

March 26, 2020

Humor or Whimsy

,

Time Out

The Future of Real Estate (And Life) Is Happily Looking Remote

read more

December 18, 2016

Appraising

,

Blogosphere

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

Real Estate Industrial Complex versus The Appraisal Institute’s Stealth Culture

read more

November 27, 2016

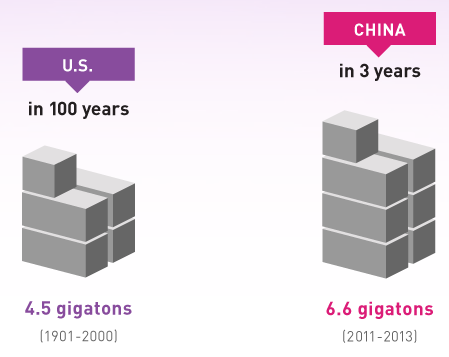

China

,

Development, Construction, Architecture & Land

,

International

,

The Real Deal

China: A Housing Market Without Re-sales?

read more

November 19, 2016

Elliman Reports

,

Fairfield County, CT

,

Greenwich

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Market Reports

Market Optics Over Facts: “Greenwich, CT is Vibrant and Active”

read more

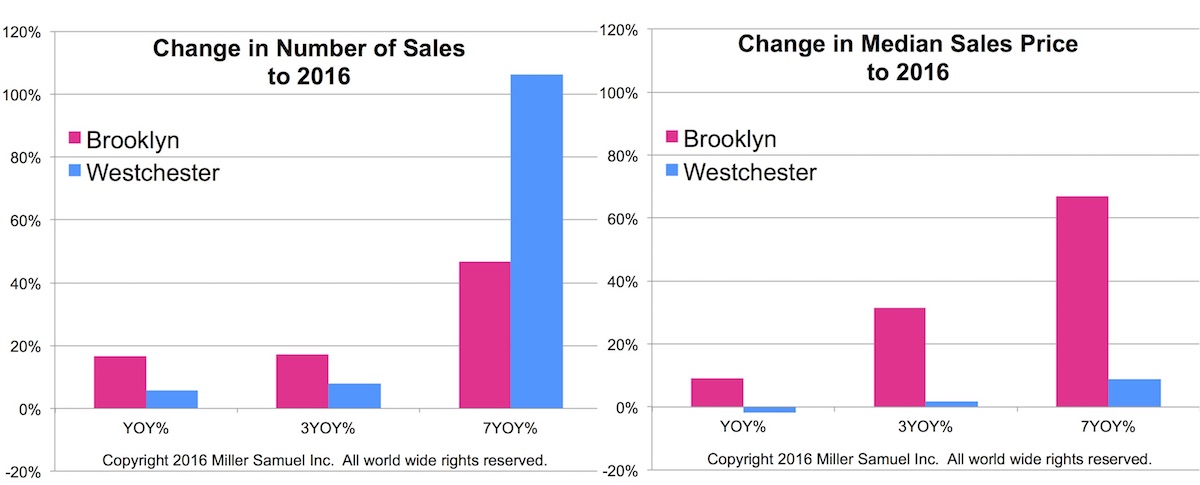

November 19, 2016

Brooklyn

,

Housing Trends & Cycles

,

Media

,

New York Times

,

Sales

,

Suburban, Urban, Commuting

,

Westchester County, NY

NYT Calculator: Suburban Sales Boom Measured By Houses on Monopoly Board

read more

May 12, 2016

Amenities, Adjustments & Value Logic

,

Boards & Associations

,

Brokers, Agents, MLS, NAR

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

How Not to Value A Co-op Apartment: Price per Share

read more

April 2, 2016

Elliman Reports

,

Manhattan

,

Miami (Beach + Mainland)

,

Yahoo! Finance

[Video] Providing the right context for Manhattan and Miami housing markets

read more

March 7, 2016

Analysis & Research

,

Federal Reserve, New York

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Weather & Natural Disasters

New Yorkers Are Busy During Week So Big Snowstorms Need to Occur On Weekends

read more

February 16, 2016

Boom Bubble Bust

,

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Homebuying Process

Contrarians React to Quicken Loans Rocket Mortgage Outrage

read more

December 21, 2015

Affordability, Affordable Housing

,

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Media

,

New York Times

Billionaires’ Row: I Can See For Miles And Miles, Until You Can’t

read more

1

2

Next

Load More Posts

Page load link

Go to Top