Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Co-ops

February 5, 2020

Charts, Maps, Images, Infographics, Video

,

Government, Politics, Regulations & Policy

,

Manhattan

,

The Real Deal

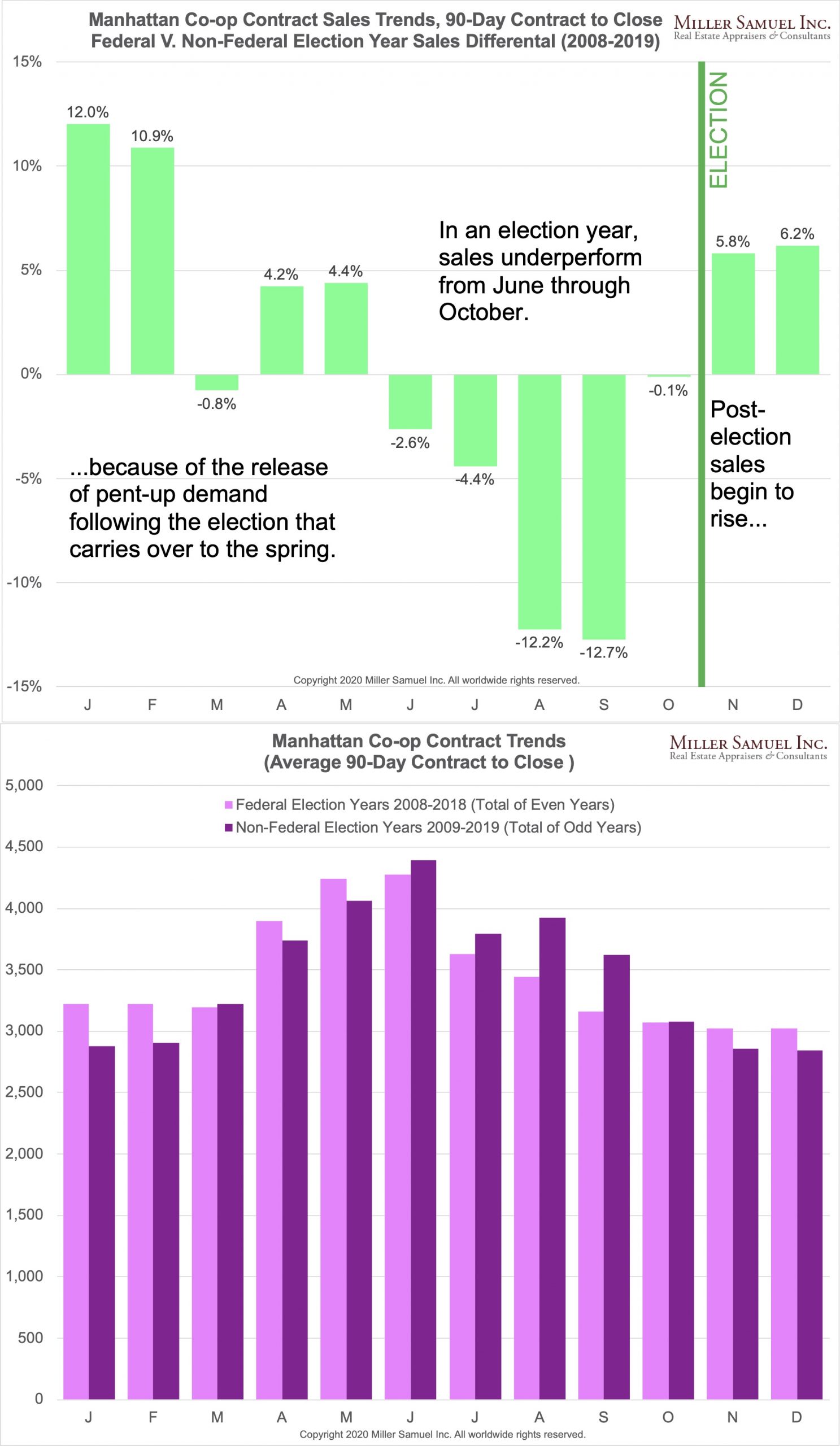

Manhattan Co-op Sales Fall During Federal Election Year

read more

May 12, 2016

Amenities, Adjustments & Value Logic

,

Boards & Associations

,

Brokers, Agents, MLS, NAR

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

How Not to Value A Co-op Apartment: Price per Share

read more

May 30, 2015

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Curbed

,

Douglas Elliman

,

Housing Trends & Cycles

,

Manhattan

,

Statistics, Metrics & Data

[Three Cents Worth #286 NY] How Many NYC Apartments Are Bought With Cold Hard Cash?

read more

August 1, 2014

Amenities, Adjustments & Value Logic

,

Analysis & Research

,

Historical, Landmark, Milestone

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Times

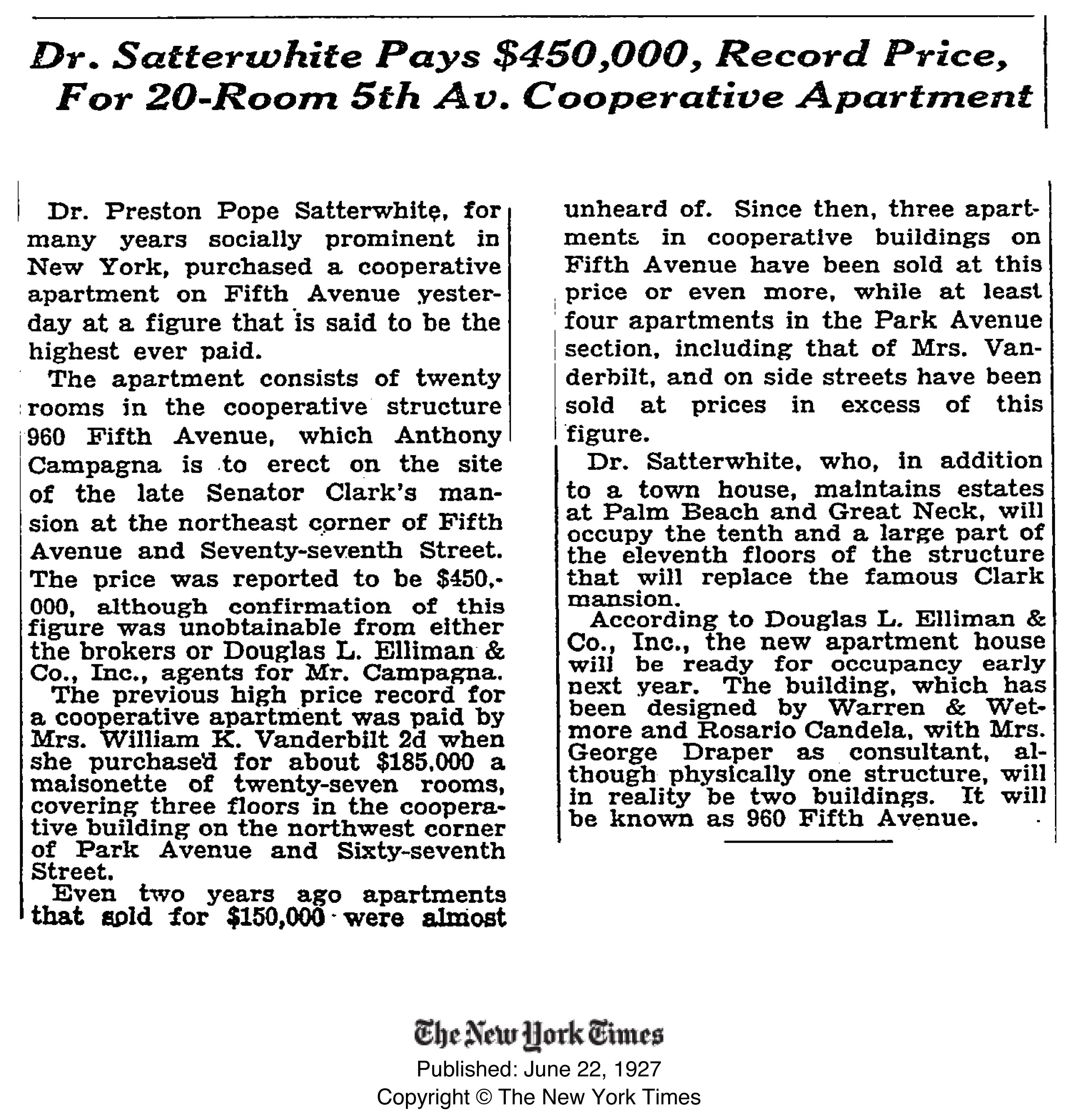

A Fifth Avenue Co-op’s 87-Year Price Increase was 3.6X Rate of Inflation

read more

June 9, 2014

Boards & Associations

,

Historical, Landmark, Milestone

,

Manhattan

,

Records, Thresholds and Outliers

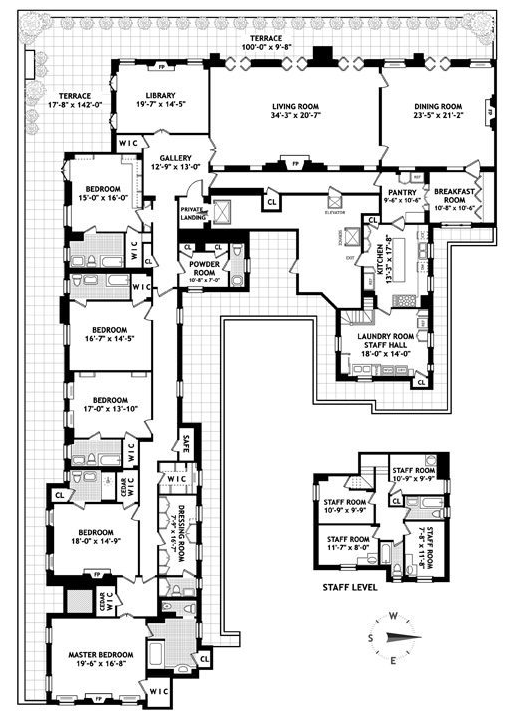

Manhattan Penthouse Co-op Sold For 2nd Highest PPSF in History

read more

May 6, 2014

Appraising

,

Boards & Associations

,

Manhattan

,

Migration, Psychology, Demographics

,

New York City

,

Queens

Floored: Can/Should A Governing Body Set Minimum Sales Prices?

read more

April 20, 2014

Amenities, Adjustments & Value Logic

,

Appraising

,

Credit, Finance, Mortgage, Rates

,

Language, Jargon & Quotes

,

Manhattan

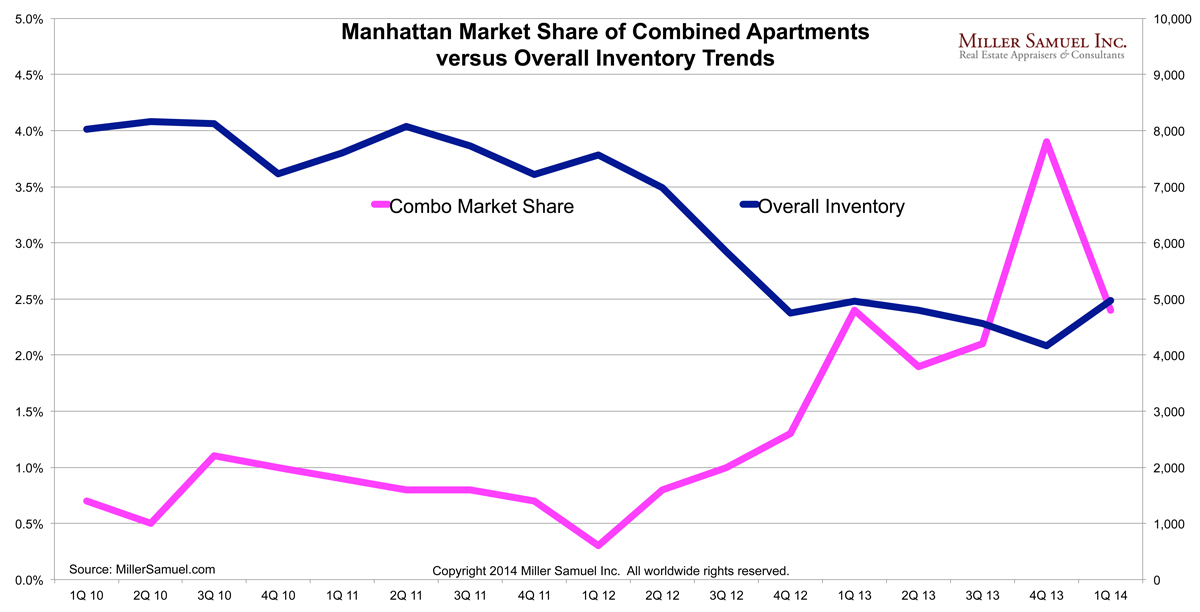

Combinations: Creating a Larger Manhattan Co-op or Condo

read more

Page load link

Go to Top