Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› college tuition

June 16, 2014

Affordability, Affordable Housing

,

Boom Bubble Bust

,

Charts, Maps, Images, Infographics, Video

,

Economy

,

Federal Reserve, New York

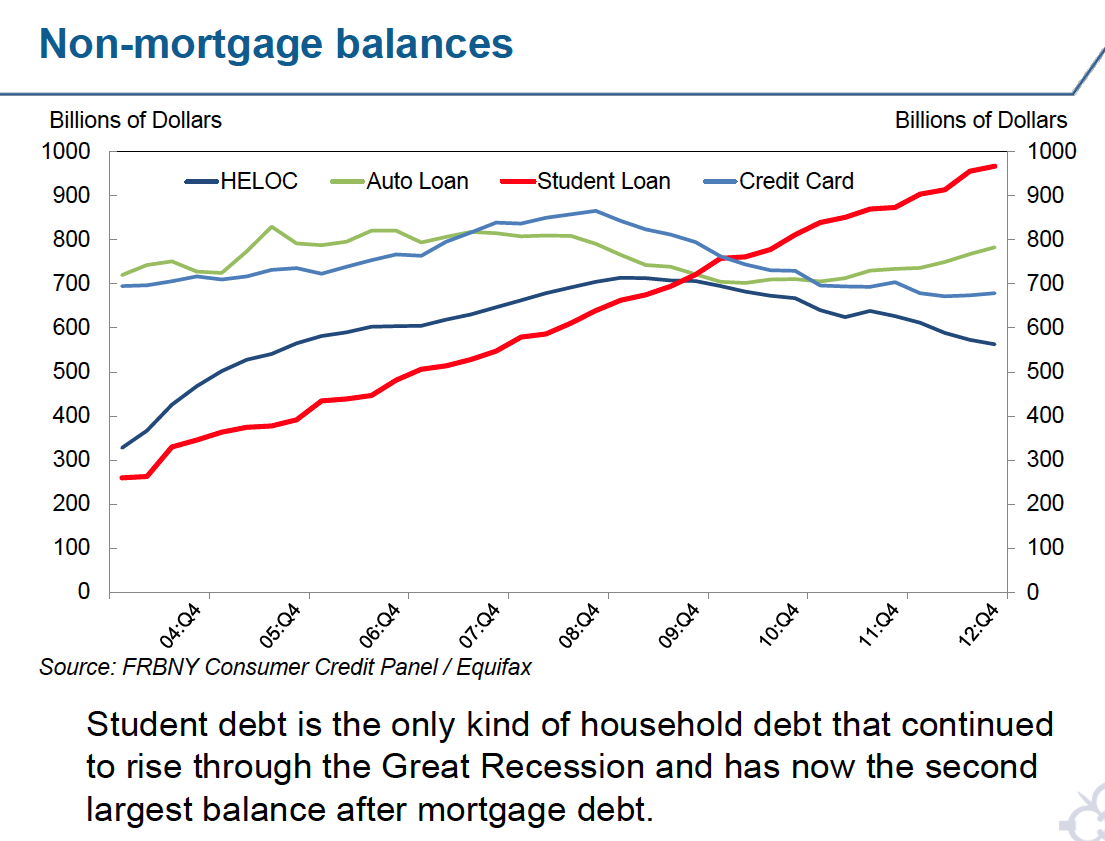

Housing is a Drag: US Student Debt Bubble Made Worse by the Baby Boomer Nanny State

read more

Page load link

Go to Top