Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Dodd-Frank

March 8, 2017

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

Banks Make Regulations Onerous By Over-Interpreting Them

read more

October 7, 2016

Appraising

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

,

Media

Voice of Appraisal Podcast: E123 “Solving Problems with Jonathan Miller!”

read more

September 27, 2014

Appraising

,

Blogging Off The Matrix

,

Bloomberg View

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

Bloomberg View Column: Guess What’s Holding Back Housing

read more

March 27, 2014

Analysis & Research

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Market Reports

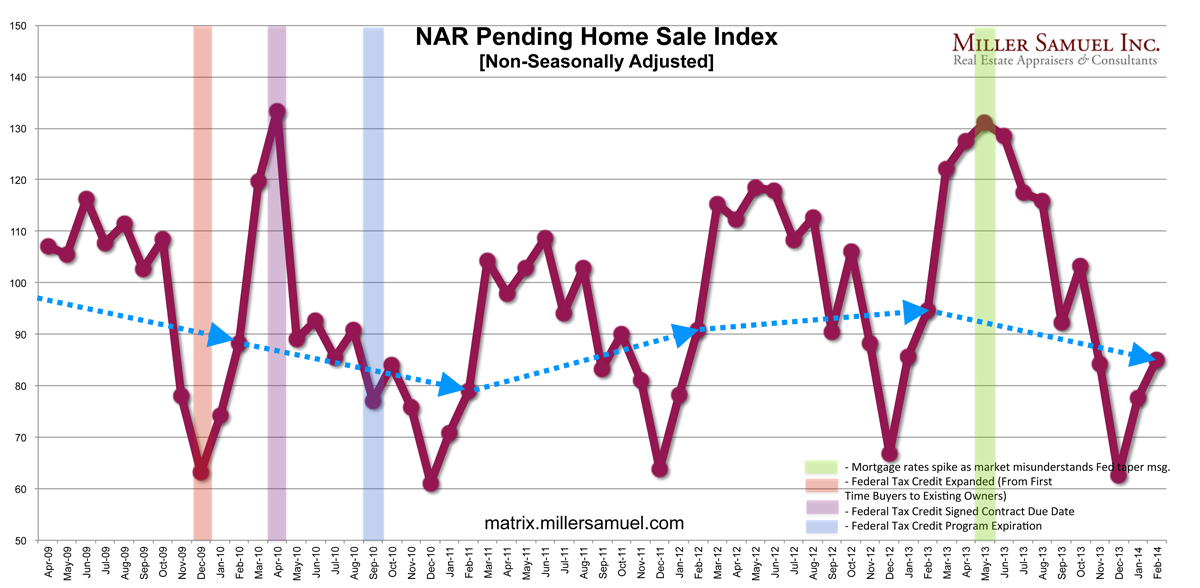

Pending Home Sales Down 10.2% YOY And That’s Not A Bad Thing

read more

Page load link

Go to Top