Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› FHFA

May 21, 2023

Appraising

,

Government, Politics, Regulations & Policy

,

Washington DC

Three Hours On C-SPAN Yields One Granddaughter

read more

March 26, 2014

Appraising

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

Regulators Turn Focus on AMCs, Proposals Include Hiring “Competent” Appraisers

read more

March 11, 2013

Analysis & Research

,

Bloomberg News

,

Government, Politics, Regulations & Policy

,

Media

,

Statistics, Metrics & Data

On Bloomberg TV, Surveillance w/Tom Keene 3-11-13: Housing, Mortgages, Rising Prices

read more

December 26, 2012

Economy

,

Government, Politics, Regulations & Policy

,

Homebuying Process

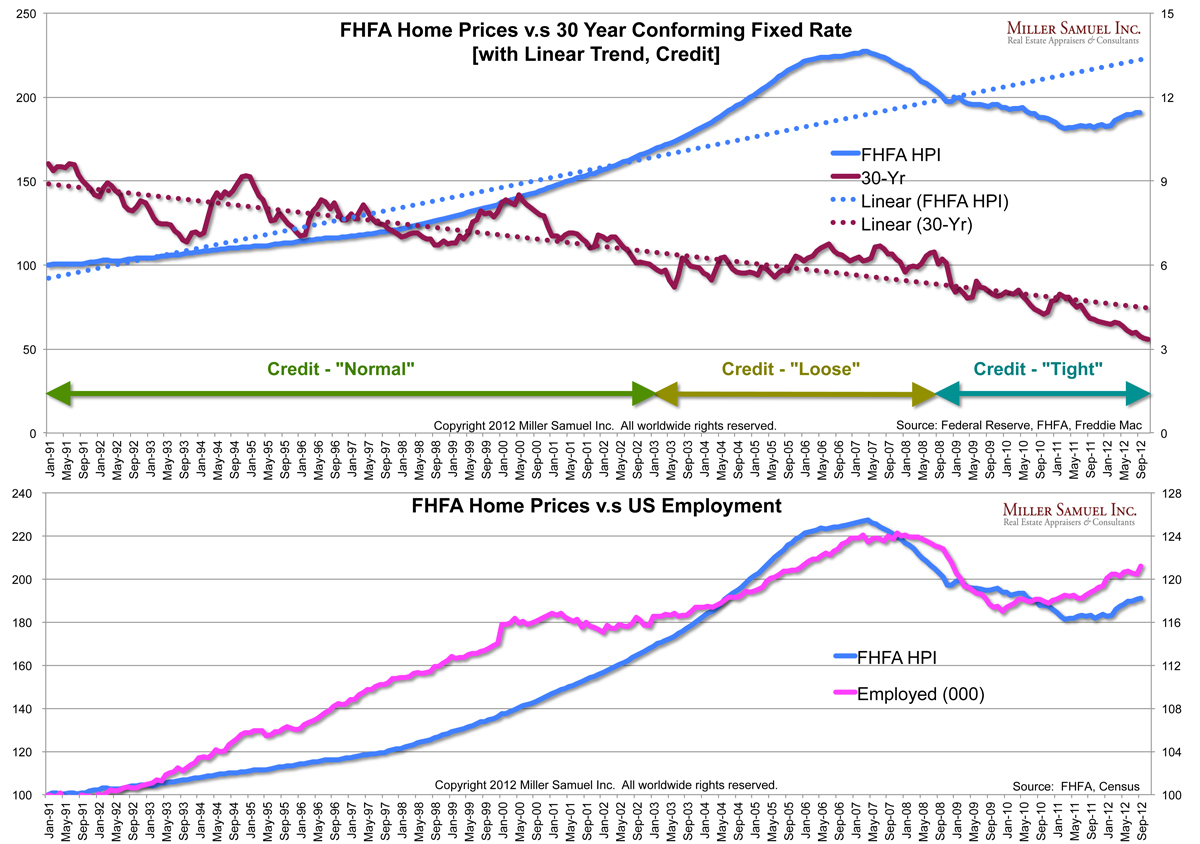

Yes, Mortgage Rates Impact Housing Prices

read more

November 18, 2010

Analysis & Research

,

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

Interviews

,

Market Reports

,

The Housing Helix

[Interview] Robert Dorsey, Chief Data and Analytics Officer, FNC Co-Founder

read more

June 23, 2010

Government, Politics, Regulations & Policy

,

IRS

,

Market Reports

[FHFA] U.S. Monthly House Price Index Up 0.8% M-O-M, Down 12.8% From Peak

read more

November 2, 2009

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

[St. Louis Fed] Home Prices: A Case for Cautious Optimism?

read more

September 22, 2009

Bloomberg News

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

IRS

,

Market Reports

[FHFA] July 2009 Monthly House Price Index

read more

August 31, 2009

Bloomberg News

,

Economy

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

Wall Street Journal

[Sentiment versus Confidence] Dow Jones Sentiment Index Shows Improvement

read more

July 30, 2009

Blogging Off The Matrix

,

Books & Movies

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

IRS

,

New York Times

,

Statistics, Metrics & Data

[HuffPost] Current Wave of Housing Euphoria May Extend Downturn

read more

June 22, 2009

Books & Movies

,

Economy

,

Government, Politics, Regulations & Policy

,

Market Reports

[Brookings’ MetroMonitor] 1Q 09 Tracking the Recession and Recovery

read more

June 22, 2009

Boom Bubble Bust

,

Government, Politics, Regulations & Policy

,

Market Reports

[New York Has 40% To Go?] Deutsche Bank Residential Real Estate Forecast

read more

1

2

Next

Load More Posts

Page load link

Go to Top