Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› GSE

March 16, 2014

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Op-Ed

,

Wall Street Journal

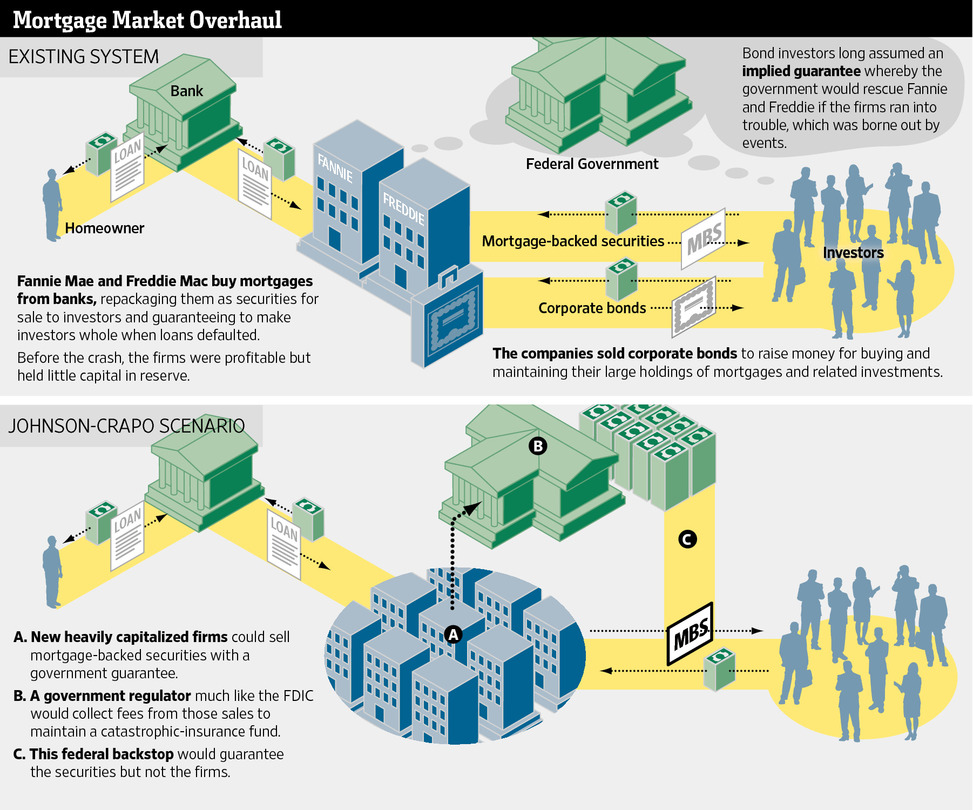

The Bi-Partisan Fannie and Freddie Solution That Isn’t A Fix

read more

March 11, 2013

Analysis & Research

,

Bloomberg News

,

Government, Politics, Regulations & Policy

,

Media

,

Statistics, Metrics & Data

On Bloomberg TV, Surveillance w/Tom Keene 3-11-13: Housing, Mortgages, Rising Prices

read more

June 23, 2010

Government, Politics, Regulations & Policy

,

IRS

,

Market Reports

[FHFA] U.S. Monthly House Price Index Up 0.8% M-O-M, Down 12.8% From Peak

read more

June 15, 2010

Credit, Finance, Mortgage, Rates

,

Furman Center

,

Government, Politics, Regulations & Policy

,

The Housing Helix

[The Housing Helix Podcast] Mark Willis, Research Fellow, NYU Furman Center

read more

June 15, 2010

Economy

,

Furman Center

,

Government, Politics, Regulations & Policy

,

Interviews

,

The Housing Helix

[Interview] Mark Willis, Research Fellow, NYU Furman Center

read more

June 7, 2010

Credit, Finance, Mortgage, Rates

,

Federal Reserve, New York

,

Furman Center

,

Government, Politics, Regulations & Policy

[Furman Center] Improving U.S. Housing Finance through Reform of Fannie Mae and Freddie Mac

read more

October 7, 2009

Federal Reserve Bank

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

,

IRS

,

Wall Street Journal

Weening Off Quantitative Easing, But Who Buys GSE Debt?

read more

May 19, 2009

Economy

,

Government, Politics, Regulations & Policy

[DMV-Like Executives] Placing All Our Housing Hopes On Institutions Losing Billions

read more

March 22, 2009

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Rentals, Investing

,

Wall Street Journal

[Seeing only 70% of the Risk] Fannie Mae Crushed Condo New Development Sales

read more

January 14, 2009

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

,

New York Times

,

Rentals, Investing

,

Wall Street Journal

[Mortgage Appraisal Havoc] Of AMCs and Code of Conduct

read more

December 12, 2008

Boom Bubble Bust

,

Government, Politics, Regulations & Policy

,

List-o-links

,

New York Times

,

Wall Street Journal

[RE-Cap] Government Sucks, Mortgage-Mod, Car Commissar, Stop Enabling, Conceptual Error

read more

November 19, 2008

Books & Movies

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

New York Times

[FHFA /OFHEO] On A Mission, With Bear Oversight

read more

1

2

Next

Load More Posts

Page load link

Go to Top