Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Zillow

November 7, 2021

Analysis & Research

,

Explainer

,

Homebuying Process

,

Housing Indices & Portals

,

Housing Trends & Cycles

Zillow Offers As A Proxy For ‘Big Data’ Shows The Lack Of Qualitative Analysis

read more

November 7, 2021

Appraising

,

Boom Bubble Bust

,

Explainer

,

Homebuying Process

This Just In: The ‘A’ in ‘Zillow’ Stands for ‘Accuracy’

read more

February 9, 2021

Housing Indices & Portals

,

Humor or Whimsy

Zillow Gets Pillowed

read more

June 28, 2020

Brokers, Agents, MLS, NAR

,

Explainer

,

Housing Trends & Cycles

,

New York City

,

Op-Ed

My Forbes Column: Keeping Housing Market Results From The Public Is Never Justified: An Expansive View

read more

June 1, 2017

Celebrity, Pop Culture

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Westchester County, NY

Homes with Blue Bathrooms Sell for More?

read more

September 1, 2015

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

,

Migration, Psychology, Demographics

,

Suburban, Urban, Commuting

,

Trulia

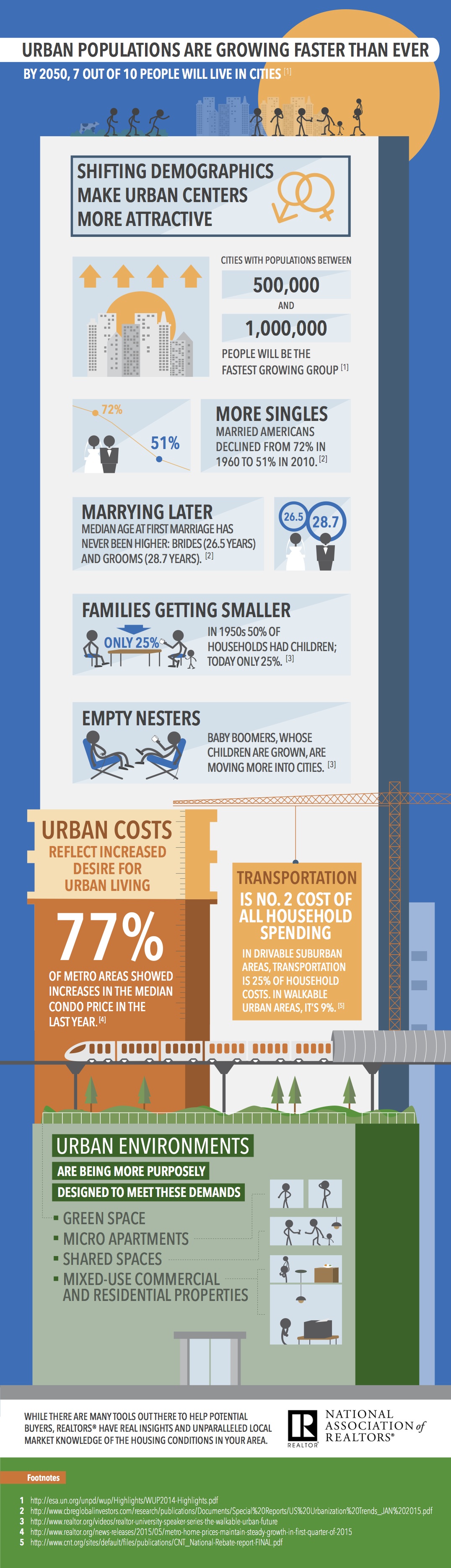

[Infographic] NAR gets into the Urbanization Conversation

read more

August 31, 2014

Blogging Off The Matrix

,

Bloomberg View

,

Crime, Protests, Social-Unrest

,

Housing Indices & Portals

,

Migration, Psychology, Demographics

,

Weather & Natural Disasters

Bloomberg View Column: The Myth of Real Estate Stigma

read more

July 28, 2014

Blogging Off The Matrix

,

Bloomberg View

,

Brokers, Agents, MLS, NAR

,

Op-Ed

,

Trulia

,

Wall Street, Financial Services

,

Washington DC

My First Post on Bloomberg View: Homebuying Gets a Housecleaning

read more

May 14, 2014

Amenities, Adjustments & Value Logic

,

Credit, Finance, Mortgage, Rates

,

Housing Trends & Cycles

,

New York City

Zillow is Forecasting Future Property Values

read more

April 15, 2014

Affordability, Affordable Housing

,

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Manhattan

,

New York City

,

New York Times

,

Rentals, Investing

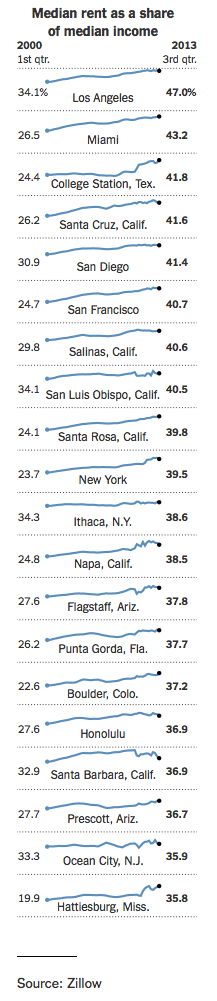

With Mortgage Lending Historically Tight, Renters Suffer Just As Much

read more

August 19, 2013

Analysis & Research

,

Bloomberg News

Zillow Acquires StreetEasy, Goes Vertical, Literally

read more

May 29, 2013

Bloomberg News

,

Elliman Reports

,

Housing Indices & Portals

,

Media

Talking Case Shiller on Bloomberg TV’s ‘Street Smart” with Betty Liu/Adam Johnson

read more

1

2

Next

Load More Posts

Page load link

Go to Top