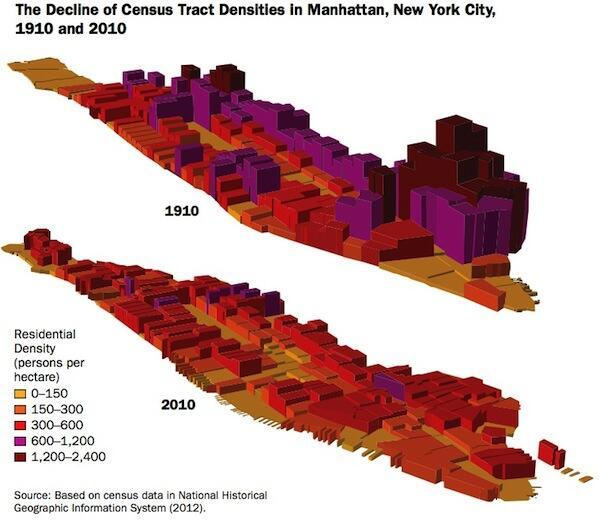

The density of the Five Points in 1910 was absolutely... Read More

21 West 38th Street, 15th Floor New York, NY 10018

© Miller Samuel Inc. 2024 • All Rights Reserved • Website by BlankSlate

21 West 38th Street, 15th Floor New York, NY 10018

© Miller Samuel Inc. 2024 • All Rights Reserved • Website by BlankSlate