Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Amenities, Adjustments & Value Logic

June 9, 2010

Amenities, Adjustments & Value Logic

,

Appraising

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

The Real Deal

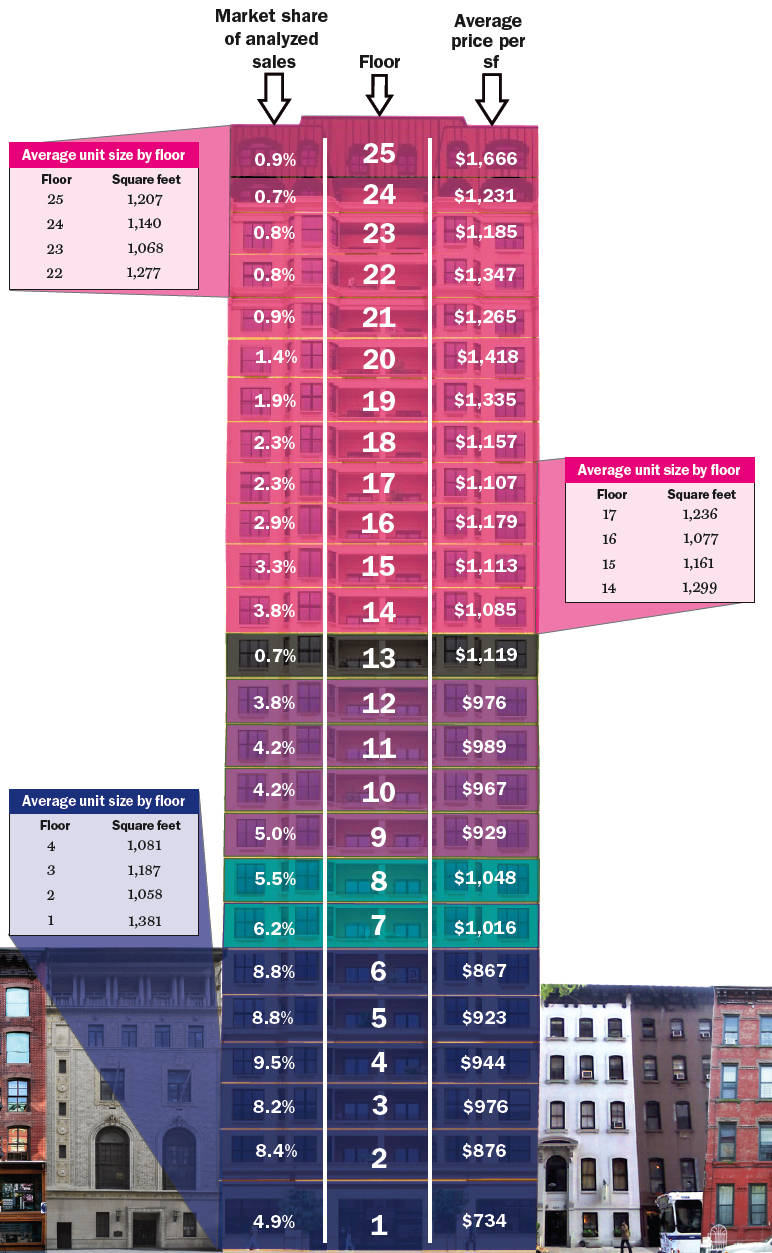

[ChartFloor] Manhattan Price Per Floor Breakdown

read more

May 5, 2010

Amenities, Adjustments & Value Logic

,

Appraising

,

Manhattan

[Terra Logic] Understanding The Value of Manhattan Apartment Outdoor Space

read more

October 26, 2009

Amenities, Adjustments & Value Logic

,

Distressed Housing

,

Humor or Whimsy

,

New York Magazine

[Central Park v. Detroit] $363,538,692,000 v. $4,500,000

read more

May 12, 2008

Amenities, Adjustments & Value Logic

,

Appraising

,

Guest Post (Vortex)

[The Hall Monitor] The Argument For Seasonal Time Adjustments

read more

June 11, 2007

Amenities, Adjustments & Value Logic

,

Appraising

,

Guest Post (Vortex)

[The Hall Monitor] Appraisers And Micrometers Don’t Mix

read more

March 5, 2007

Amenities, Adjustments & Value Logic

,

Appraising

,

Guest Post (Vortex)

[The Hall Monitor] Adjustments For The Maladjusted

read more

July 5, 2006

Amenities, Adjustments & Value Logic

,

Luxury, Super, Ultra, Mega

,

Migration, Psychology, Demographics

Penthouse Article In New York Living

read more

February 13, 2006

Amenities, Adjustments & Value Logic

,

Appraising

,

Homebuying Process

,

Migration, Psychology, Demographics

I See Dead People And They Want Me To Make An Adjustment

read more

January 9, 2006

Amenities, Adjustments & Value Logic

,

Appraising

The Changing Values Of Renovations

read more

December 27, 2005

Amenities, Adjustments & Value Logic

,

Appraising

Central Park: No Price Can Be Attached To The Center Of The Universe

read more

October 31, 2005

Amenities, Adjustments & Value Logic

,

Appraising

,

Taxes, Insurance, Fees

A Taxing View Leads To A Revolt

read more

October 25, 2005

Amenities, Adjustments & Value Logic

,

Appraising

Adjusting for Dragons

read more

Previous

2

3

Load More Posts

Page load link

Go to Top