Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Analysis & Research

February 22, 2024

Analysis & Research

,

Economy

,

Explainer

,

Housing Trends & Cycles

[27 Speaks Podcast] Jonathan Miller Provides A 2024 Hamptons Outlook

read more

October 3, 2023

Analysis & Research

,

Explainer

,

Manhattan

Urban Digs Webinar: Valuing Outdoor Space

read more

October 10, 2022

Analysis & Research

,

Appraising

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Homebuying Process

,

Housing Trends & Cycles

,

Public Speaking

[Podcast] Slate Money: Felix Learns What A Condo Is – Jonathan Miller joins to talk all things real estate.

read more

November 7, 2021

Analysis & Research

,

Explainer

,

Homebuying Process

,

Housing Indices & Portals

,

Housing Trends & Cycles

Zillow Offers As A Proxy For ‘Big Data’ Shows The Lack Of Qualitative Analysis

read more

May 18, 2021

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Manhattan

[WNBC] The State of New York Real Estate

read more

July 6, 2020

Analysis & Research

,

Bloomberg TV

,

Charts, Maps, Images, Infographics, Video

,

Elliman Reports

,

Housing Trends & Cycles

,

New York City

[Bloomberg TV] Bloomberg Markets 7-6-20: A Busy Housing Market This Summer

read more

May 12, 2020

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Explainer

,

Housing Note

,

Housing Trends & Cycles

,

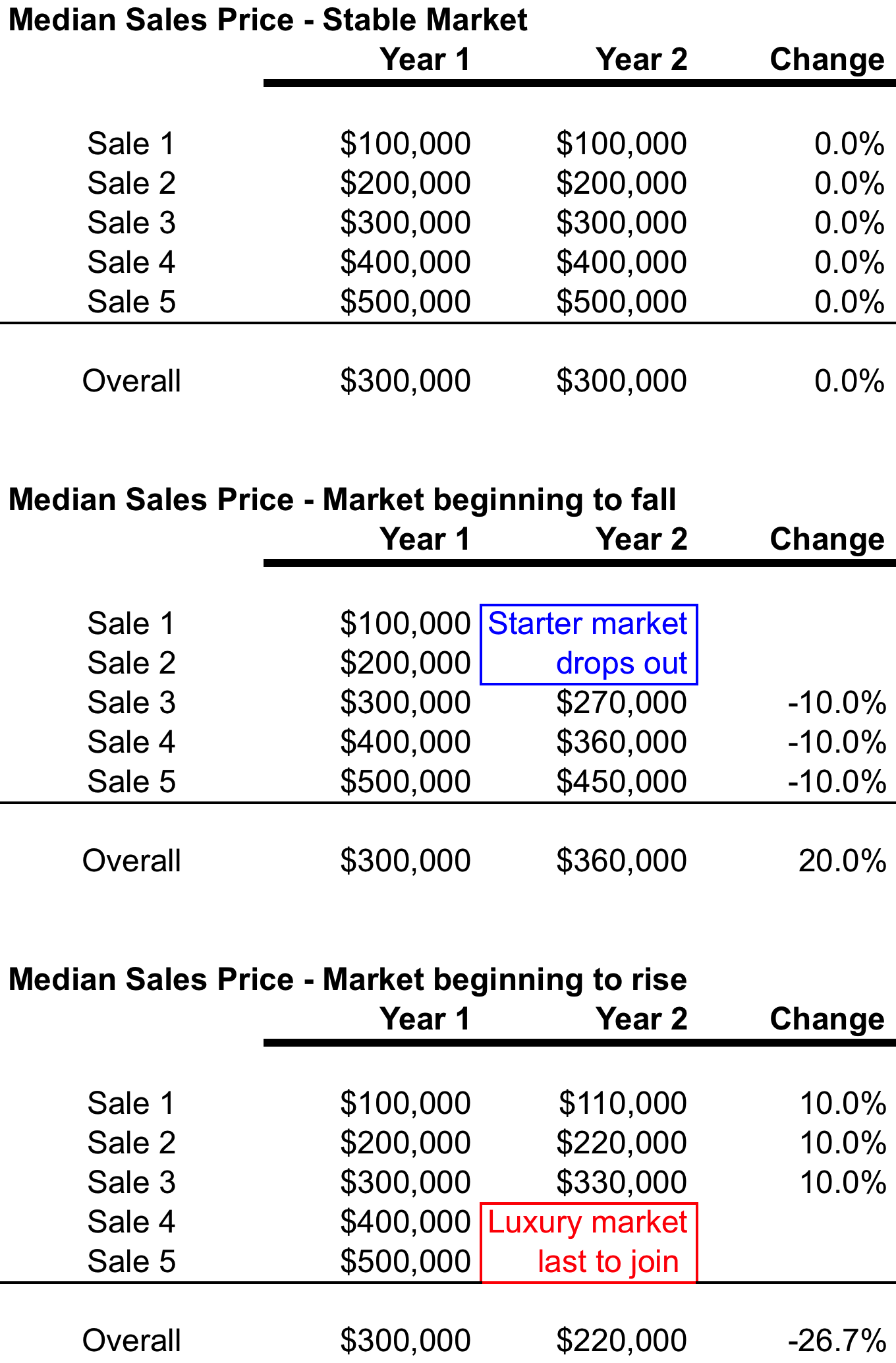

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Statistics, Metrics & Data

Median sales price can be subject to skew by consumer behavior more than math

read more

April 29, 2020

Analysis & Research

,

Brokers, Agents, MLS, NAR

,

Explainer

,

Housing Trends & Cycles

,

Statistics, Metrics & Data

Contract Data Is Pending Data Is Lagging Data

read more

February 7, 2019

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

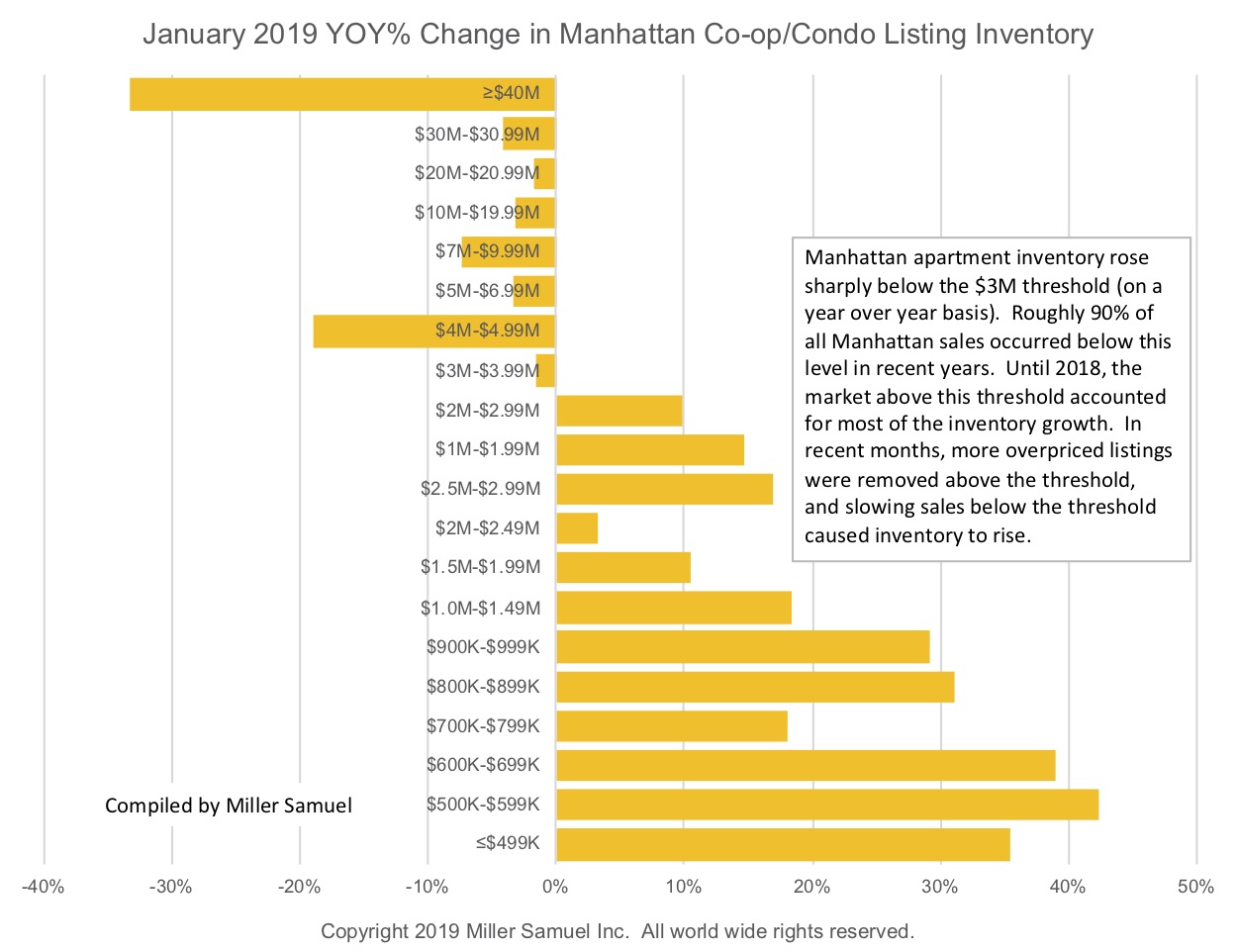

January 2019 YOY% Change in Manhattan Co-op/Condo Listing Inventory

read more

December 13, 2018

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

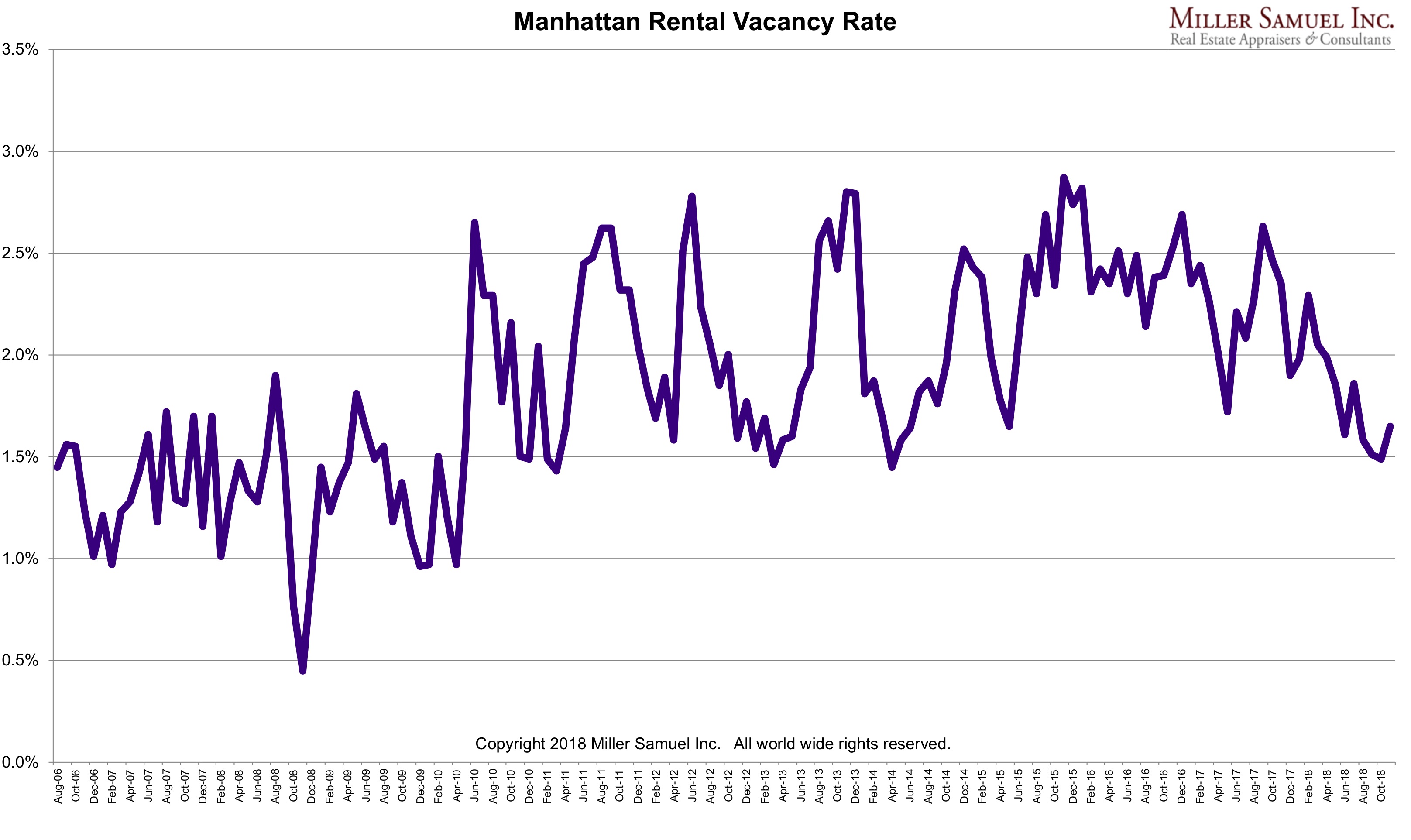

Manhattan Residential Vacancy Rate Isn’t Seasonal?

read more

January 11, 2018

Analysis & Research

,

Bloomberg TV

,

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Housing Trends & Cycles

,

Interviews

,

Manhattan

,

Market Reports

,

Queens

,

Westchester County, NY

[Media] Bloomberg Markets Interview January 11, 2018

read more

September 18, 2017

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Greenwich

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Los Angeles

,

Manhattan

,

Miami (Beach + Mainland)

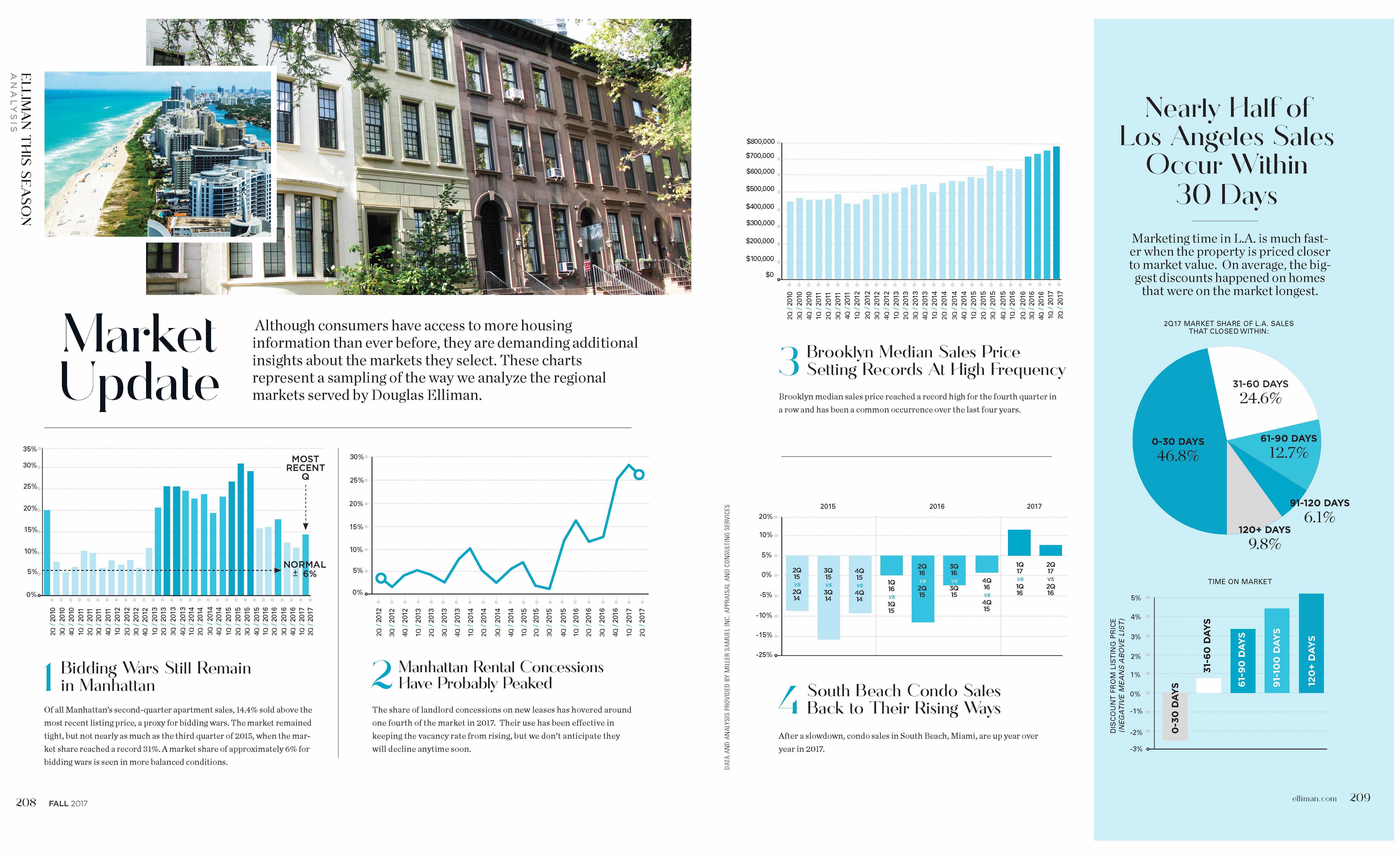

Real Estate ChartArt in Elliman Magazine’s Fall 2017 Issue

read more

1

2

Next

Load More Posts

Page load link

Go to Top