Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Analysis & Research

November 30, 2014

Analysis & Research

,

Bloomberg View

,

Boom Bubble Bust

,

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

Bloomberg View Column: Housing Bust Wasn’t About the House

read more

November 7, 2014

Analysis & Research

,

Blogging Off The Matrix

,

Bloomberg View

,

Distressed Housing

,

Rentals, Investing

,

Wall Street, Financial Services

Bloomberg View Column: Hedge-Fund Guys Have Foreclosure Fatigue

read more

September 27, 2014

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

Migration, Psychology, Demographics

,

Suburban, Urban, Commuting

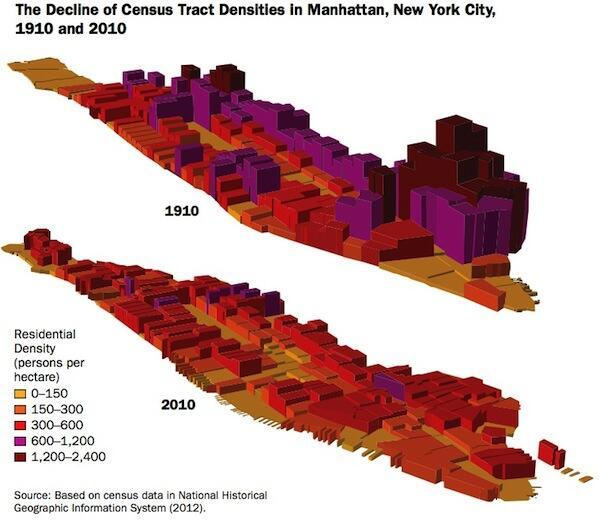

A Century Later: Manhattan Is Less Crowded

read more

August 1, 2014

Amenities, Adjustments & Value Logic

,

Analysis & Research

,

Historical, Landmark, Milestone

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Times

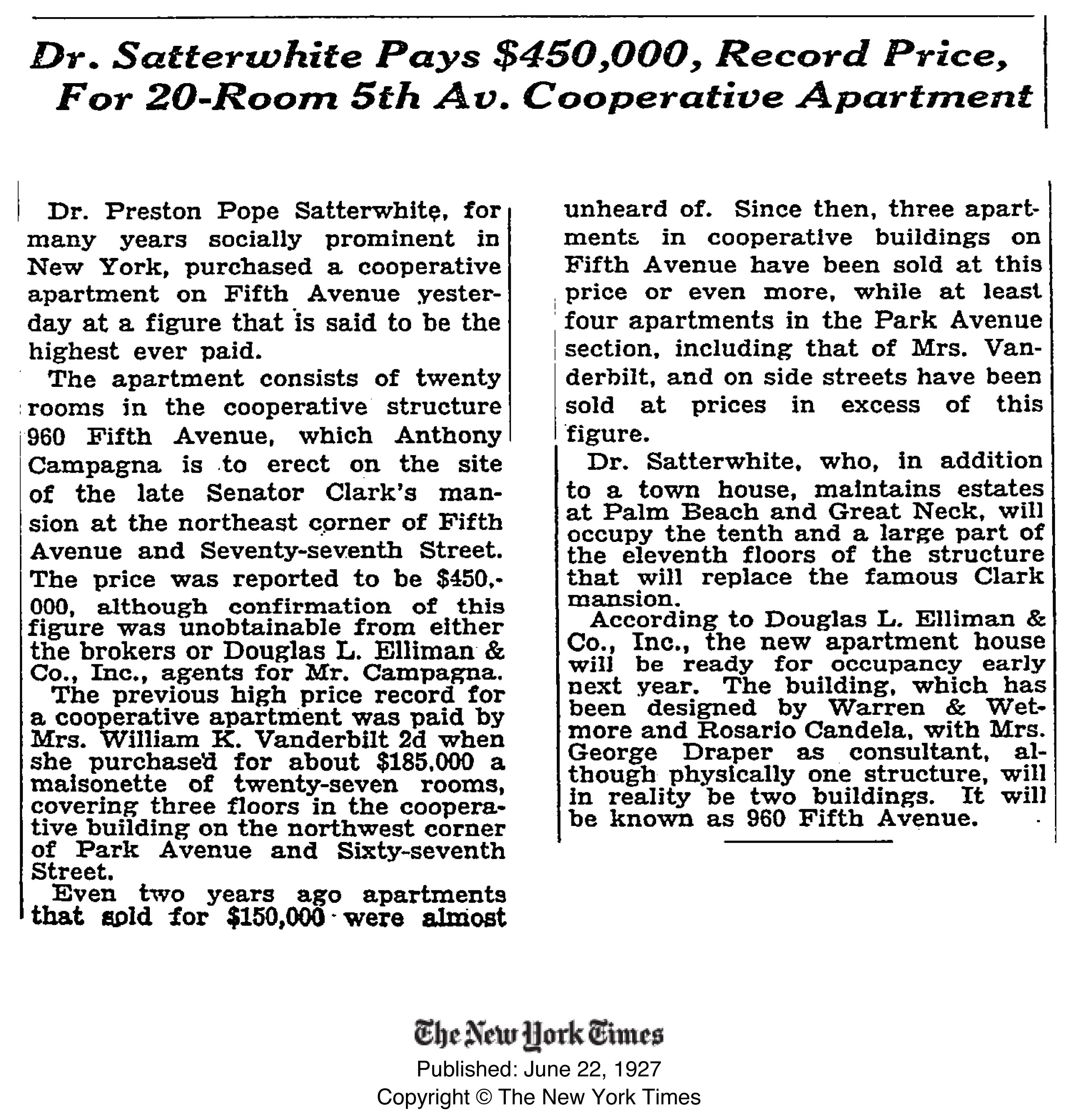

A Fifth Avenue Co-op’s 87-Year Price Increase was 3.6X Rate of Inflation

read more

June 24, 2014

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Housing Indices & Portals

,

Housing Trends & Cycles

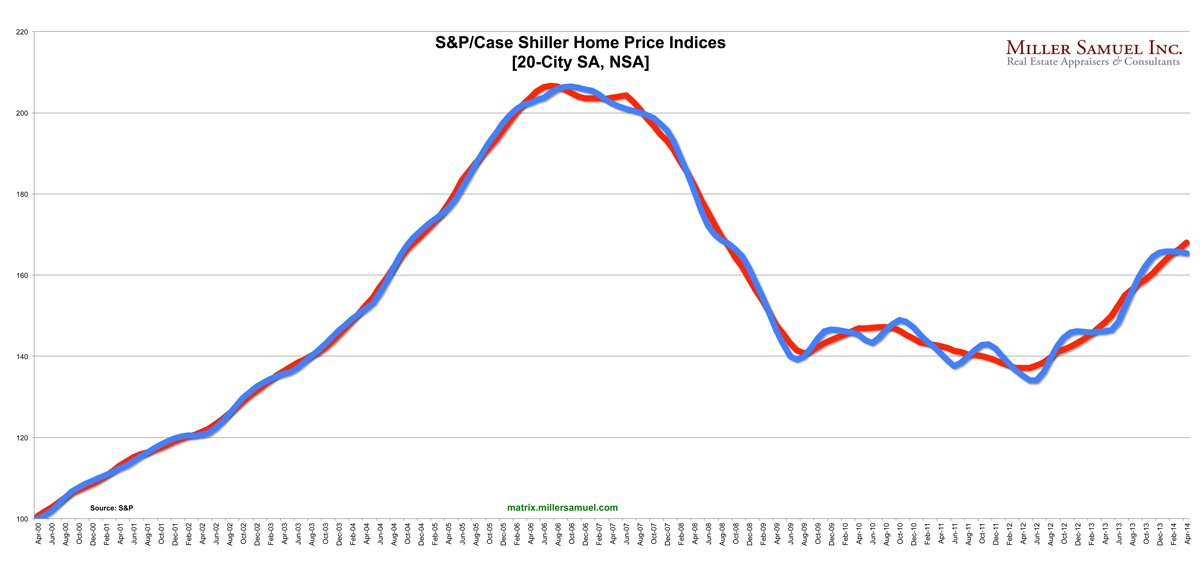

Time-Shifted Case Shiller: Dallas, Denver Crushing it, Polar Vortex a Non-Issue ‘Cause It’s Still December

read more

June 8, 2014

Analysis & Research

,

Brokers, Agents, MLS, NAR

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Migration, Psychology, Demographics

Status Quo Bias: ‘Linear” Thinking in the Real Estate Industry

read more

May 17, 2014

Analysis & Research

,

Backyard BBQ Talk

,

Credit, Finance, Mortgage, Rates

,

Douglas Elliman

,

Manhattan

,

RealtyTrac

,

Statistics, Metrics & Data

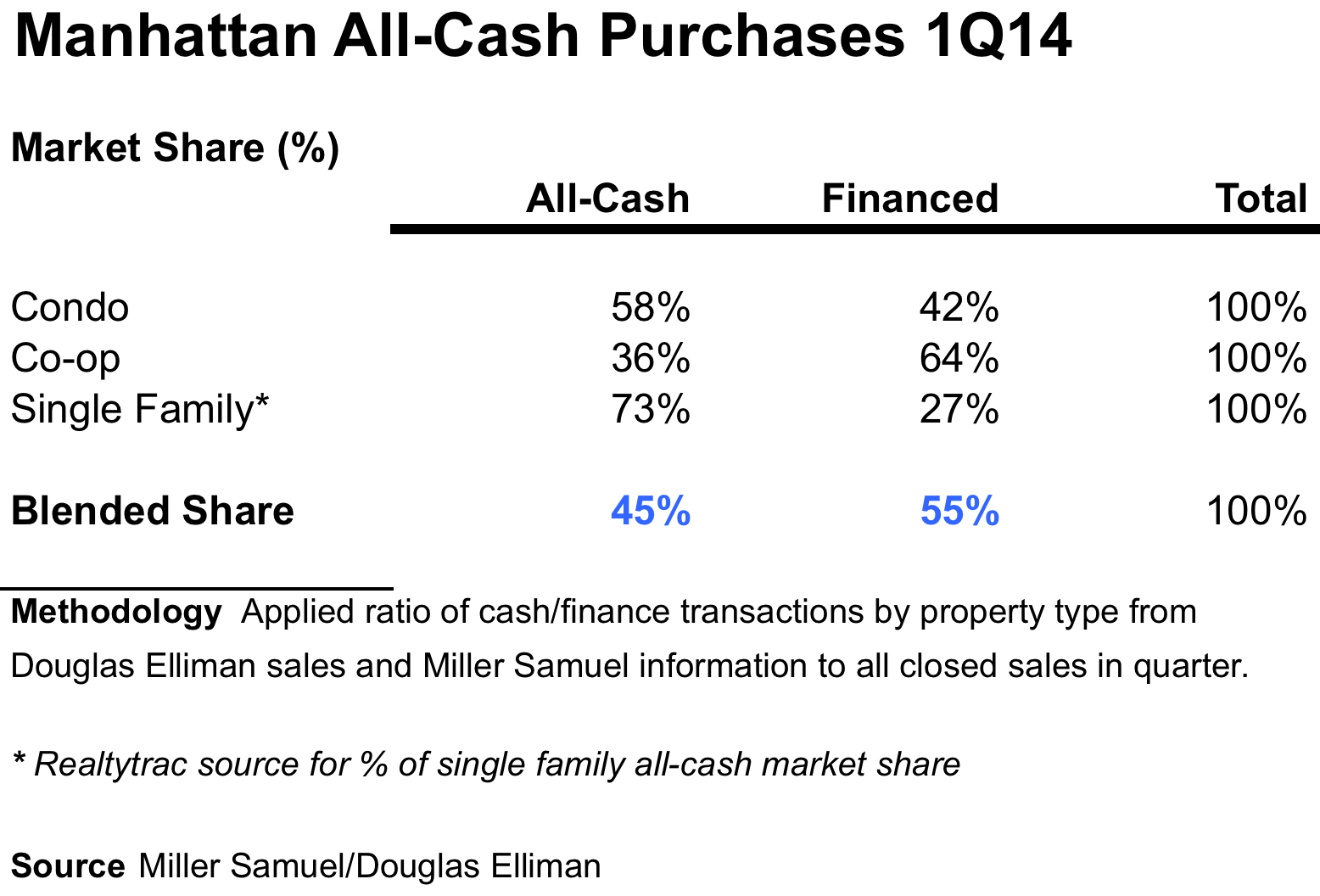

Manhattan Home Sales Are NOT 80% All-Cash (They Are 45%)

read more

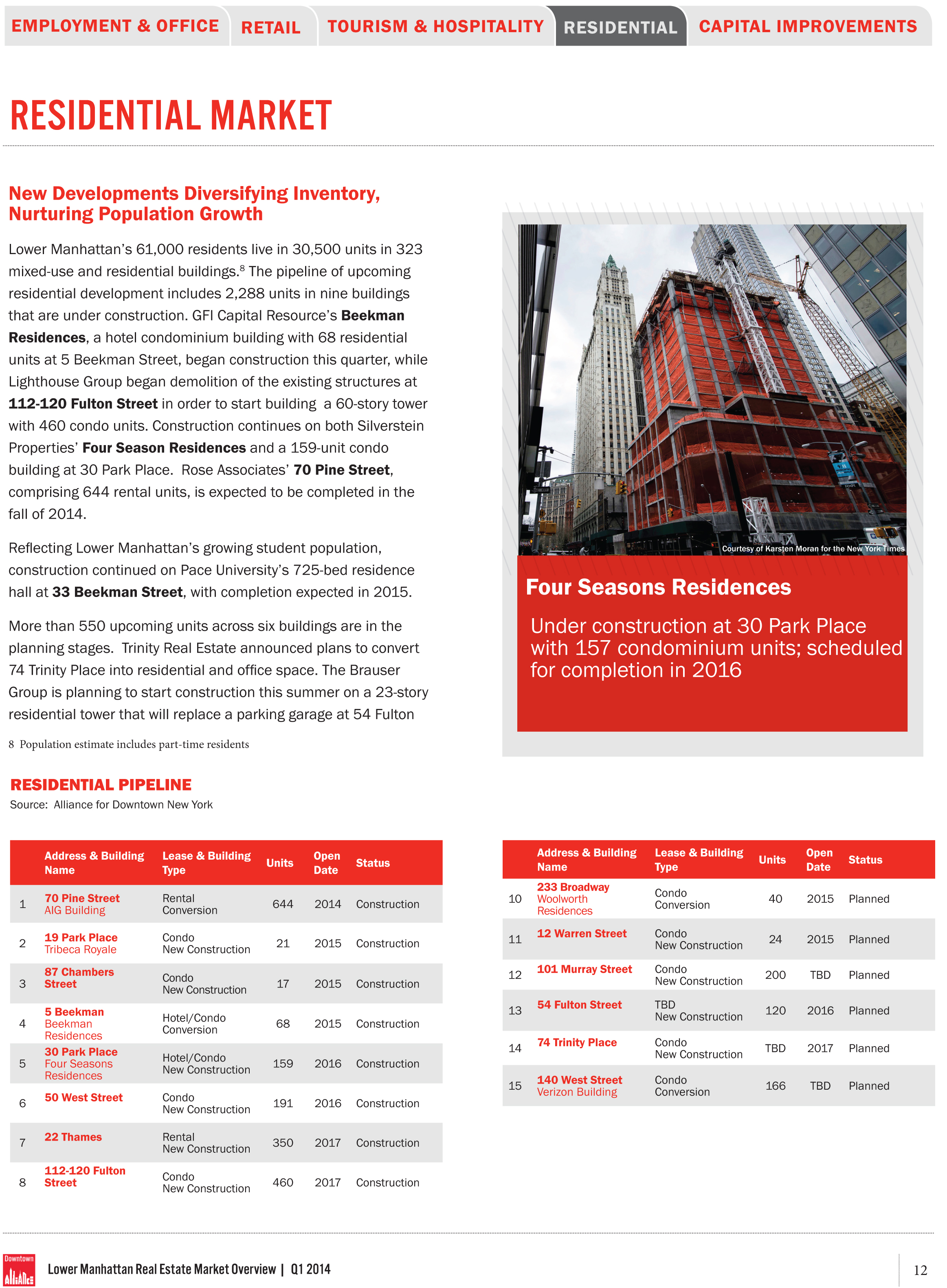

May 5, 2014

Analysis & Research

,

Downtown Alliance

,

Manhattan

Q1 2014 Lower Manhattan Real Estate Market: “Vigorous,” “Expand,” “Bullish”

read more

April 28, 2014

Analysis & Research

,

Backyard BBQ Talk

,

Housing Indices & Portals

,

Market Reports

PBS Newshour – Making Sense of Weak US Housing Reports

read more

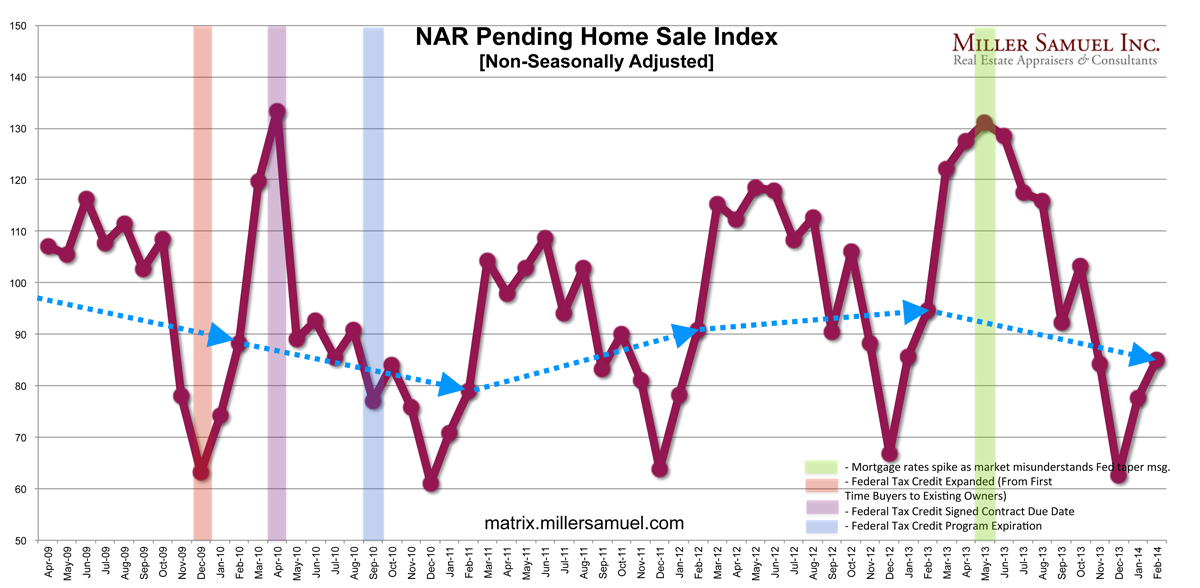

March 27, 2014

Analysis & Research

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Market Reports

Pending Home Sales Down 10.2% YOY And That’s Not A Bad Thing

read more

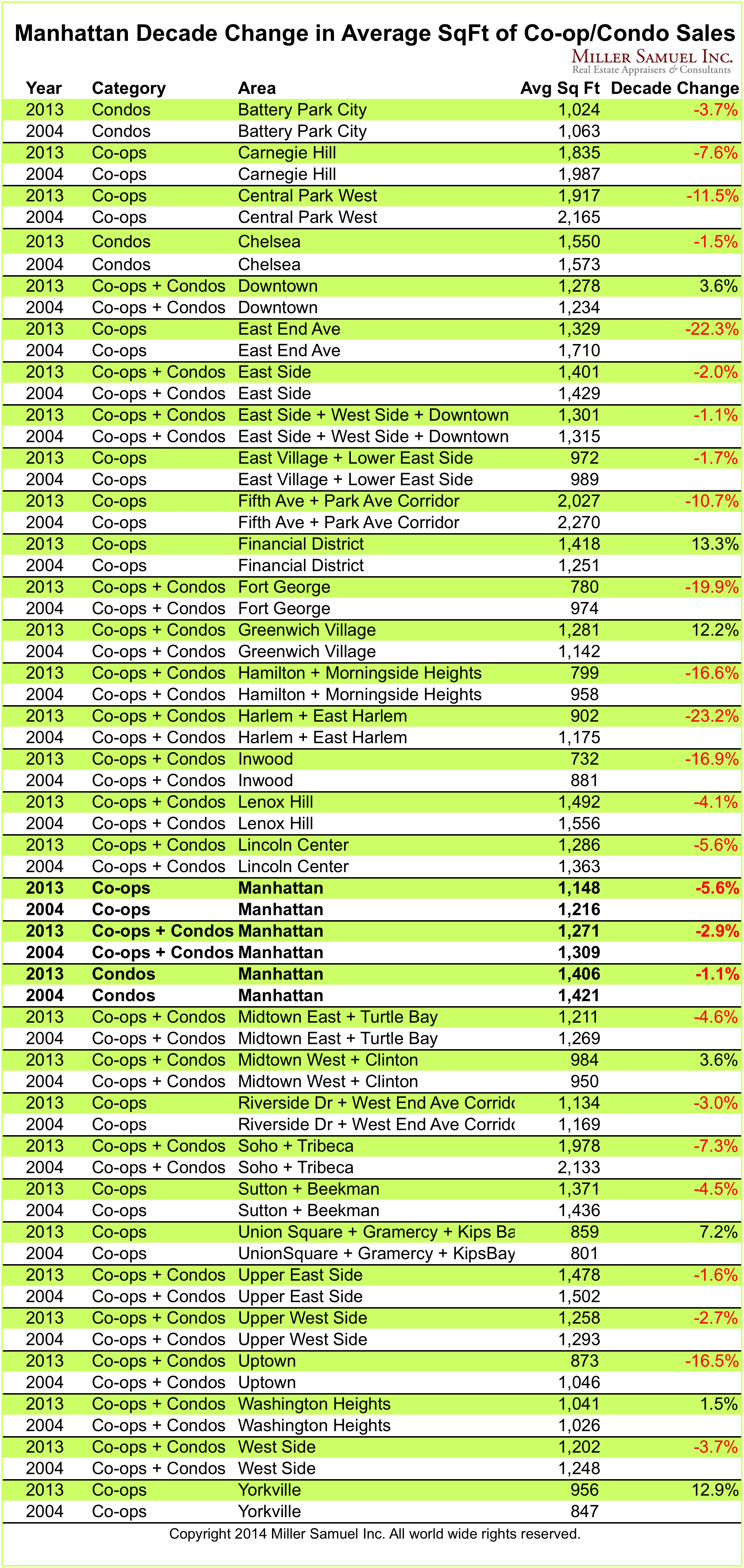

March 19, 2014

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

,

Manhattan

Manhattan’s Decade of Incredible Shrinking Apartment Sizes

read more

March 17, 2014

Analysis & Research

,

Economy

,

New York City

,

Wall Street, Financial Services

Bonus for NYC Housing: Wall Street Comp Up 15.1%, Most Cash Paid Out Since ’08 Crash

read more

Previous

2

3

4

Next

Load More Posts

Page load link

Go to Top