Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Analysis & Research

March 4, 2014

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

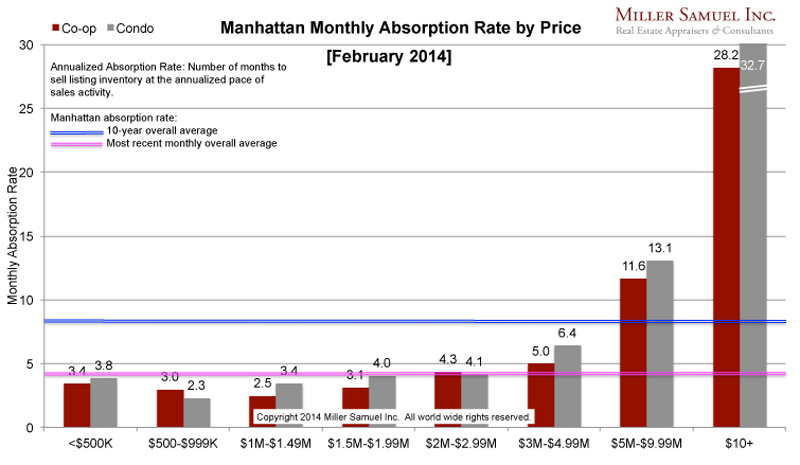

[Manhattan Absorption] February 2014 – “Tight Supply” as a Market Rant

read more

March 3, 2014

Analysis & Research

,

Backyard BBQ Talk

,

Manhattan

,

South Florida

,

Suburban, Urban, Commuting

Price per Square Inch for Pizza, Slices for Real Estate Market

read more

February 5, 2014

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

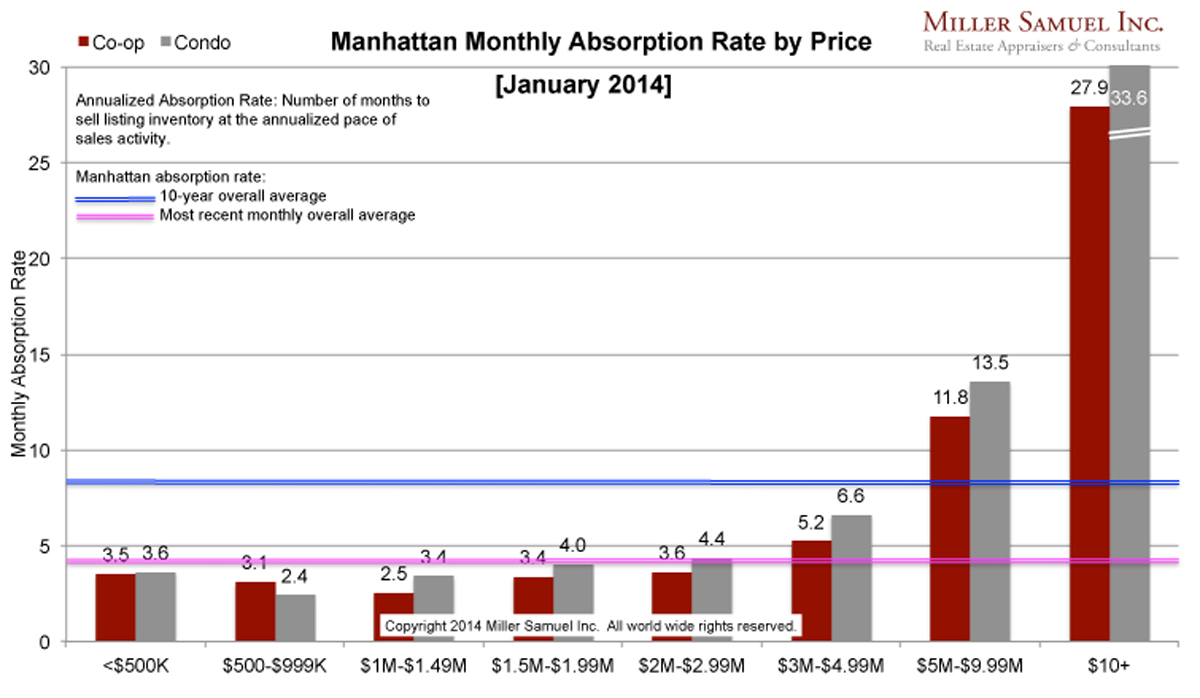

[Manhattan Absorption] January 2014 – “Bottom 99%” of Market Is Tight

read more

September 9, 2013

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

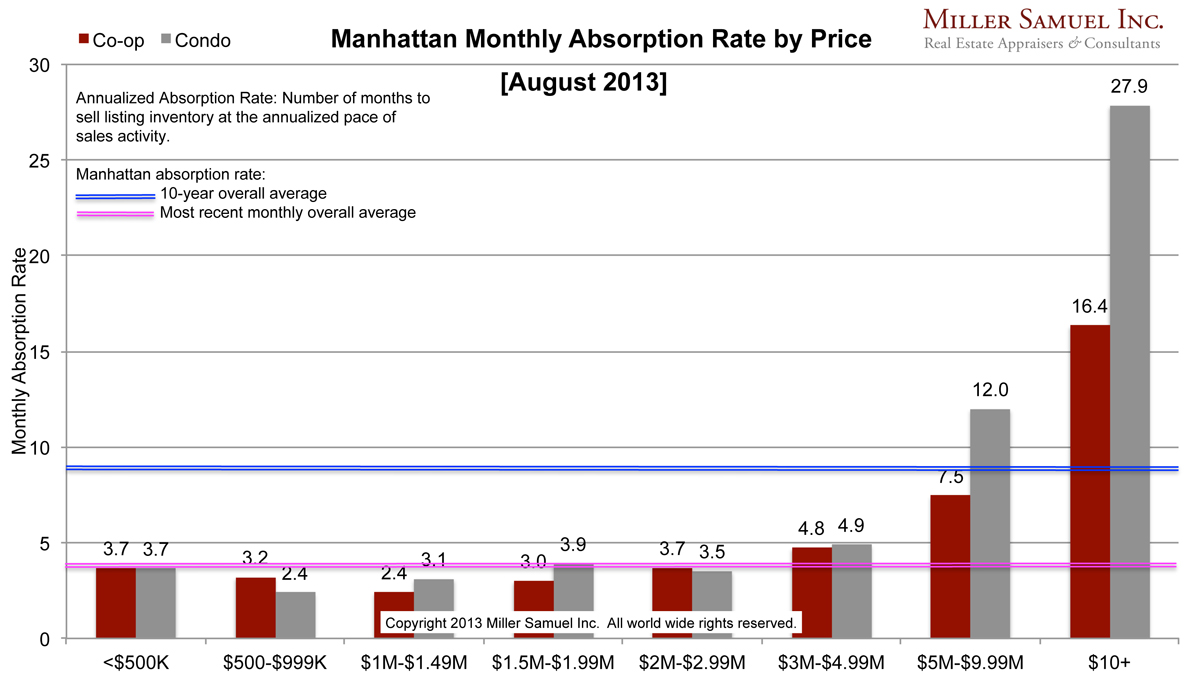

[Manhattan Absorption] August 2013 – Don’t Blink or It’s Gone (Except Trophies)

read more

August 22, 2013

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

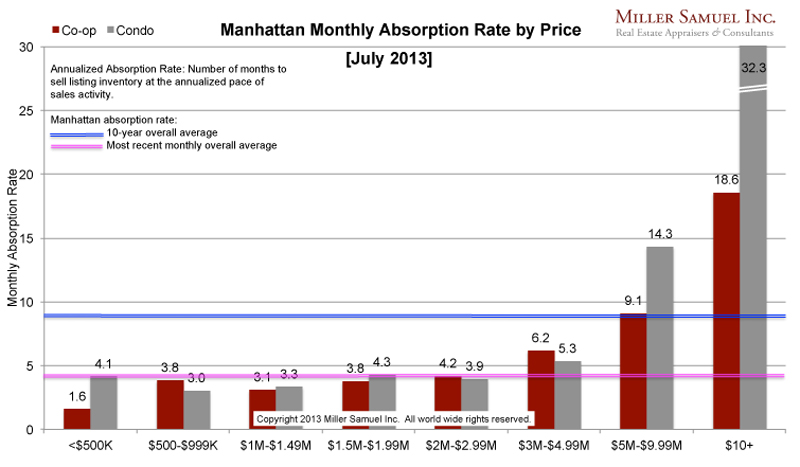

[Manhattan Absorption] July 2013 – Most of Market At Breakneck Pace, But North of $5M Slows

read more

August 19, 2013

Analysis & Research

,

Bloomberg News

Zillow Acquires StreetEasy, Goes Vertical, Literally

read more

June 6, 2013

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

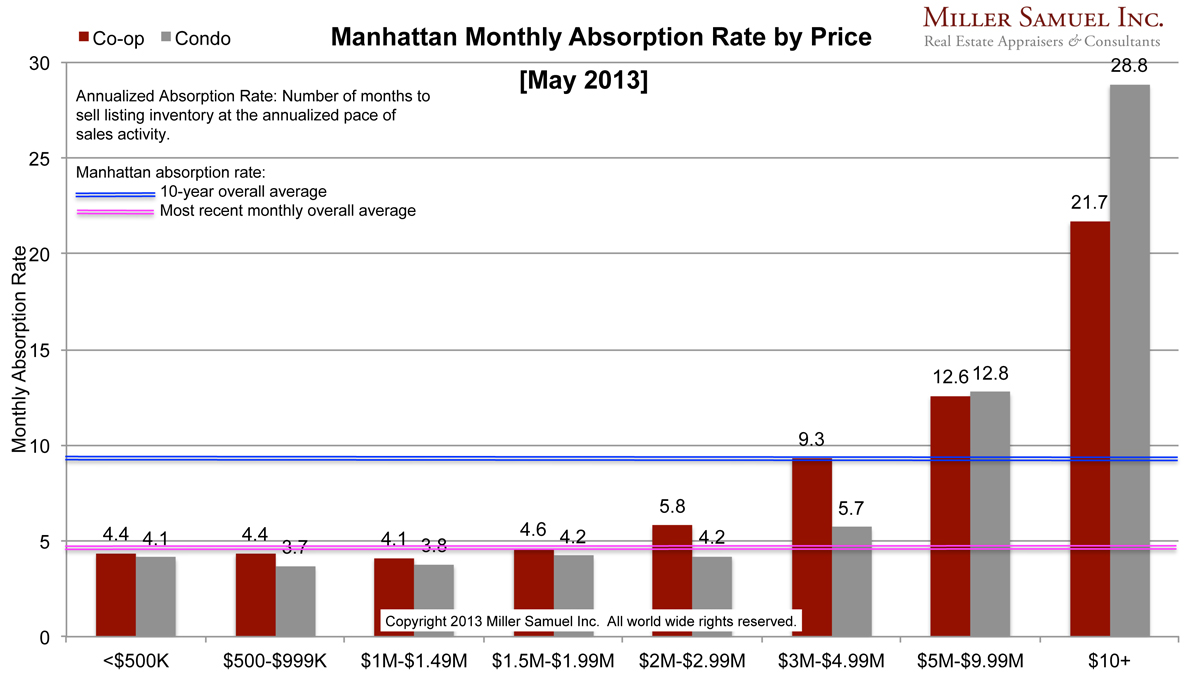

[Manhattan Absorption] May 2013 – Fast Pace Below $2M Remains, Slowing On Top

read more

May 12, 2013

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

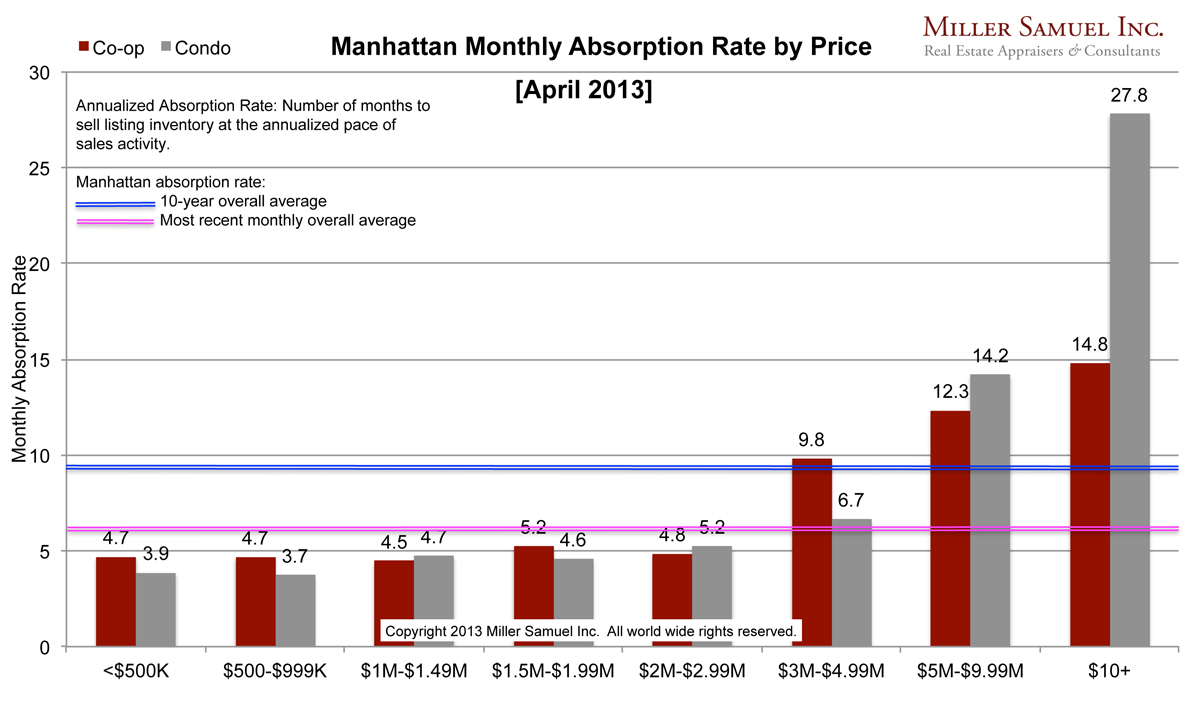

[Manhattan Absorption] April 2013 – The Bottom 90% is Brisk

read more

April 7, 2013

Analysis & Research

,

Manhattan

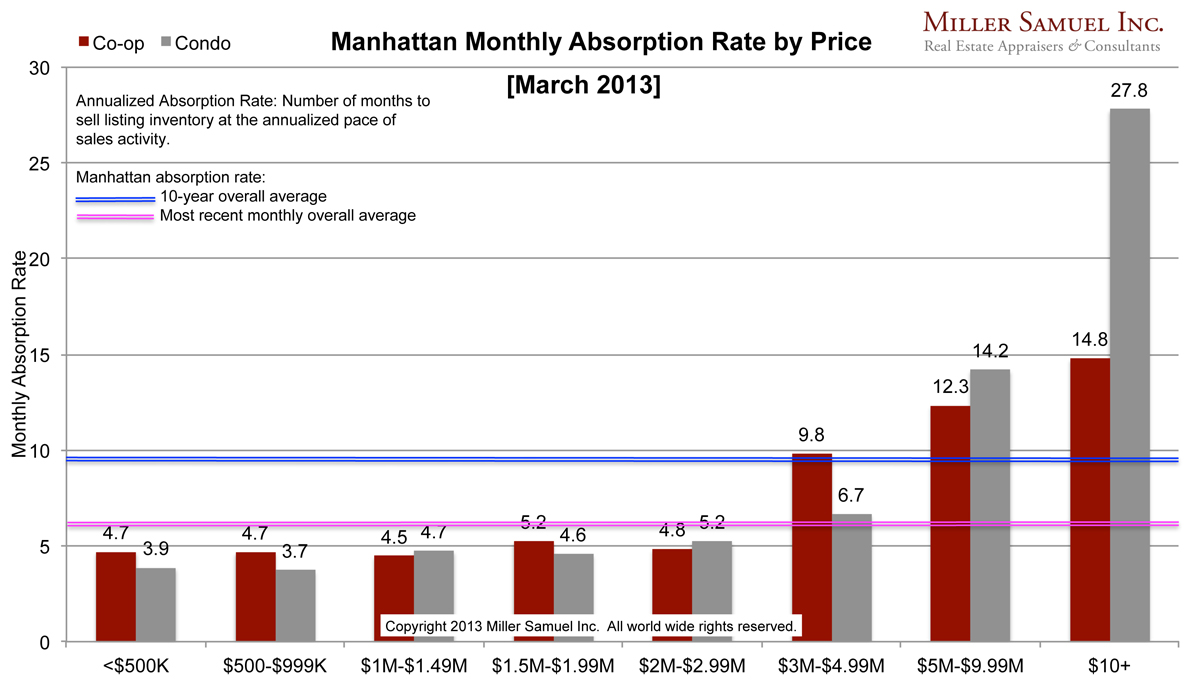

[Manhattan Absorption] March 2013 – What a Difference a Year Makes

read more

March 18, 2013

Analysis & Research

,

Manhattan

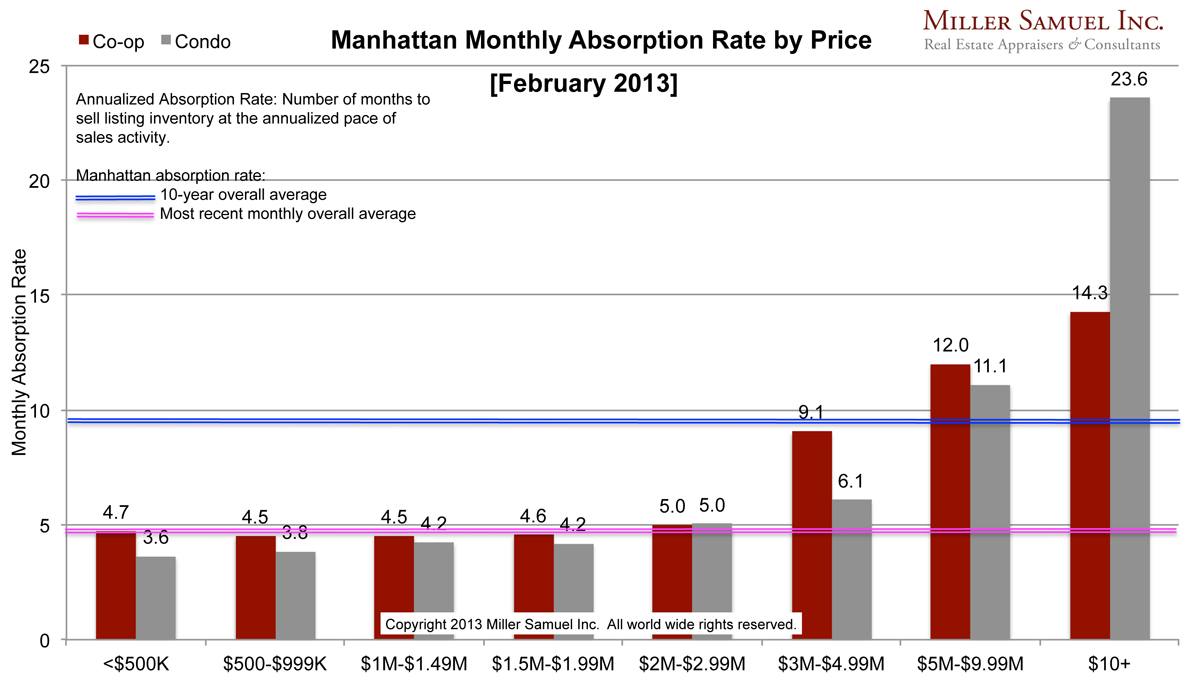

[Manhattan Absorption] February 2013 Shows Not Enough Supply To Wet A Sponge

read more

March 11, 2013

Analysis & Research

,

Bloomberg News

,

Government, Politics, Regulations & Policy

,

Media

,

Statistics, Metrics & Data

On Bloomberg TV, Surveillance w/Tom Keene 3-11-13: Housing, Mortgages, Rising Prices

read more

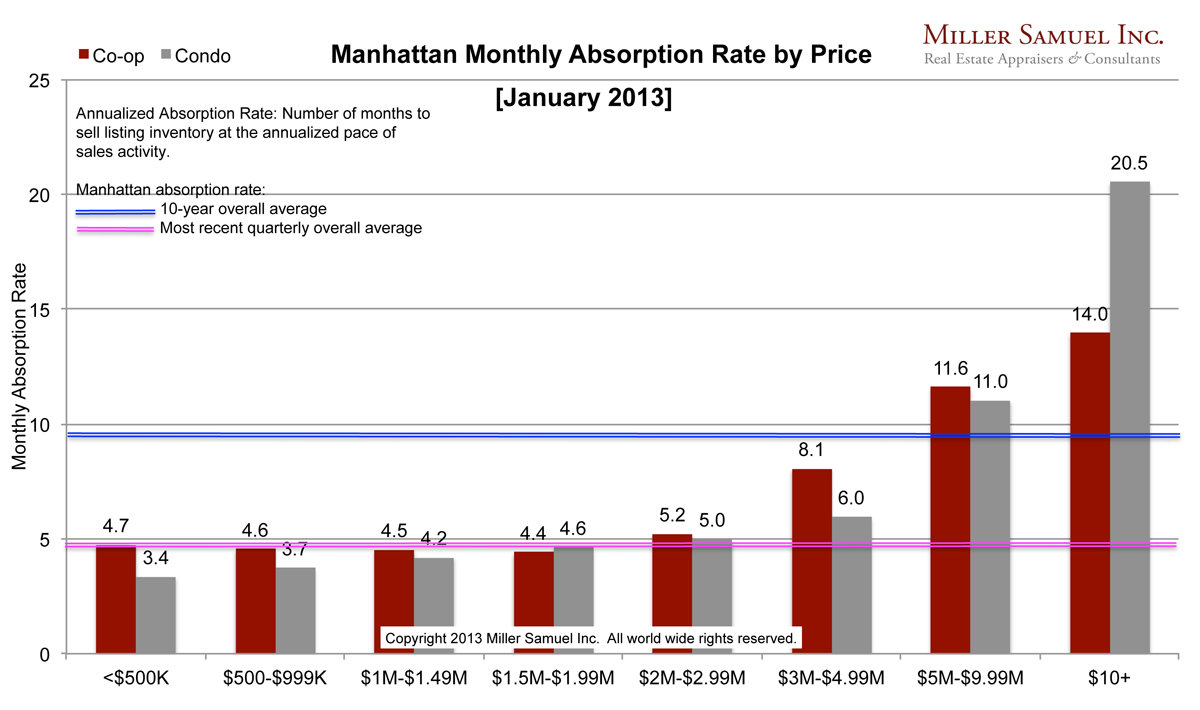

February 4, 2013

Analysis & Research

,

Manhattan

[Manhattan Absorption] January 2013 Absorbing Faster Than Paper Towels

read more

Previous

3

4

5

Next

Load More Posts

Page load link

Go to Top