Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Appraising

May 31, 2015

Appraising

,

Charts, Maps, Images, Infographics, Video

Infographic: 25 Year Demise of the Bank Appraisal Industry and the Rise of AMCs

read more

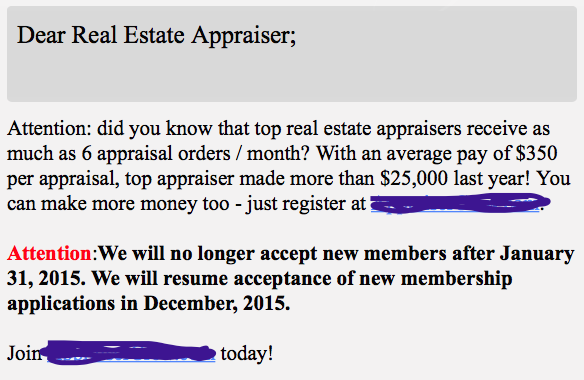

January 28, 2015

Appraising

Getting excited about the “Top Appraiser” making $25K last year!

read more

December 26, 2014

Appraising

,

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

Bloomberg View Column: Do Experts Value Your Home More Than You?

read more

December 26, 2014

Appraising

,

Bloomberg View

,

Boom Bubble Bust

Bloomberg View Column: Real-Estate Appraisals Are Bubbly Again

read more

October 20, 2014

Appraising

,

Government, Politics, Regulations & Policy

,

Public Speaking

,

Social, Tech, Gadgets, Software

Bad Actors: AMC Appraisal Perspective Through Rhetorical Misdirection

read more

September 27, 2014

Appraising

,

Op-Ed

Lone Wolves: Appraisers Fighting Everyone, Including Appraisers

read more

September 27, 2014

Appraising

,

Blogging Off The Matrix

,

Bloomberg View

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

Bloomberg View Column: Guess What’s Holding Back Housing

read more

June 18, 2014

Appraising

,

Law, Ethics & Fraud

My First Post: July 31, 2005 APM Marketplace Radio’s “Appraising the Appraiser”

read more

June 13, 2014

Appraising

,

Law, Ethics & Fraud

AMC Structure Systematically Pushes Good Appraisers Out of Business

read more

June 11, 2014

Appraising

,

Relocation Appraisers & Consultants

RAC: The Best Appraisers in North America

read more

June 9, 2014

Appraising

,

Books & Movies

,

Development, Construction, Architecture & Land

,

Environmental

,

Housing Trends & Cycles

,

International

,

Luxury, Super, Ultra, Mega

[London Calling] ‘Mike Mulligan and his Steam Shovel’ New Development Edition

read more

May 31, 2014

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Law, Ethics & Fraud

,

Wall Street, Financial Services

Spectacular TED Talk on The US Financial Crisis: How it Happened + How to Prevent

read more

Previous

3

4

5

Next

Load More Posts

Page load link

Go to Top