Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Appraising

May 21, 2014

Appraising

,

Law, Ethics & Fraud

,

Op-Ed

Room 666: Providing court testimony as an expert witness makes you better

read more

May 6, 2014

Appraising

,

Boards & Associations

,

Manhattan

,

Migration, Psychology, Demographics

,

New York City

,

Queens

Floored: Can/Should A Governing Body Set Minimum Sales Prices?

read more

April 20, 2014

Amenities, Adjustments & Value Logic

,

Appraising

,

Credit, Finance, Mortgage, Rates

,

Language, Jargon & Quotes

,

Manhattan

Combinations: Creating a Larger Manhattan Co-op or Condo

read more

March 26, 2014

Appraising

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

Regulators Turn Focus on AMCs, Proposals Include Hiring “Competent” Appraisers

read more

March 23, 2014

Appraising

,

Social, Tech, Gadgets, Software

[AppWatch] RoomScan – An Easy Way to Create A Floorplan

read more

March 19, 2014

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

Online Petition To Get “Customary & Reasonable Fees” Issue In Front of CFPB

read more

March 15, 2014

Appraising

,

Charts, Maps, Images, Infographics, Video

,

Continuing Education & Licensing

,

Credit, Finance, Mortgage, Rates

,

Homebuying Process

,

Law, Ethics & Fraud

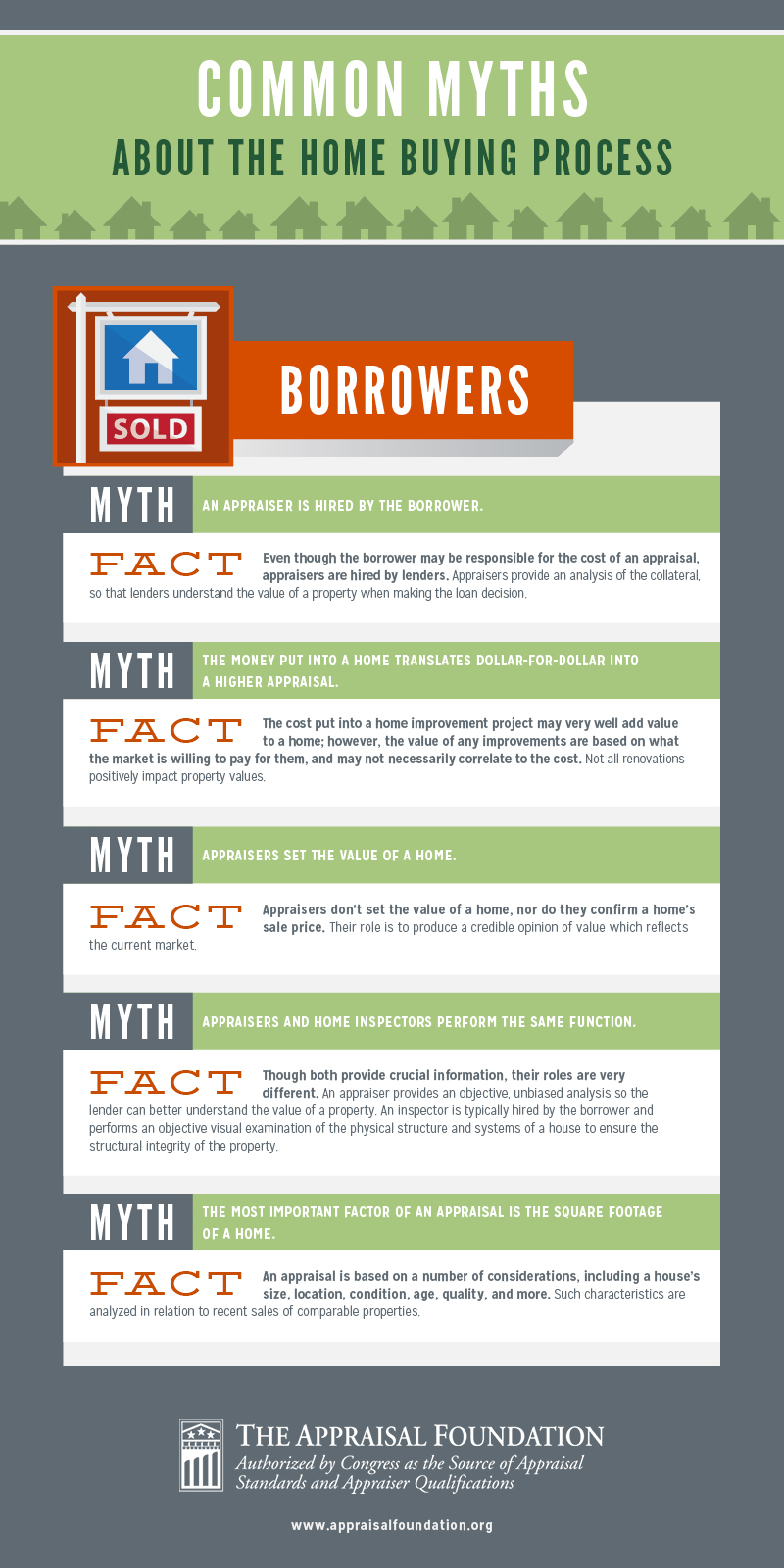

[Appraisal Infographic] Common Myths About The Homebuying Process

read more

March 9, 2014

Appraising

,

Continuing Education & Licensing

,

Public Speaking

[Speaking] 2014 RAC / TRN Conference in Frisco/Dallas Texas

read more

March 9, 2014

Appraising

,

Government, Politics, Regulations & Policy

,

Op-Ed

It’s time to debunk the debunking of the 3 biggest myths about your AMC

read more

February 27, 2014

Appraising

,

Op-Ed

Why AMC Addendums Are Bane of an Appraiser’s Existence

read more

February 12, 2014

Appraising

,

Continuing Education & Licensing

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve, New York

,

Long Island

,

Public Speaking

,

Weather & Natural Disasters

[Pre-Nor’easter Keynote] Long Island Housing Market: Transitioning from “Recovery” to “Recovered”

read more

September 16, 2013

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

New York Times

,

Wall Street Journal

The Low Appraisal “Hassle” is a Symptom of a Broken Mortgage Process

read more

Previous

4

5

6

Next

Load More Posts

Page load link

Go to Top