Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Appraising

July 2, 2013

Appraising

,

Humor or Whimsy

Future Appraiser Discovered by String Cheese Incident

read more

February 3, 2013

Amenities, Adjustments & Value Logic

,

Appraising

,

Furman Center

,

New York Magazine

Valuing A Fireplace

read more

January 27, 2013

Adventures in Media & Marketing

,

Appraising

,

Brokers, Agents, MLS, NAR

,

New York Times

Broken Appraisal: Lack of Market Knowledge Overpowers Lack of Data

read more

January 13, 2013

Appraising

,

Credit, Finance, Mortgage, Rates

,

Homebuying Process

,

Media

,

New York Times

Having Fits With Appraisal In Home Buying Process

read more

December 27, 2012

Appraising

,

Credit, Finance, Mortgage, Rates

Appraising for AMCs Can Be Like Delivering Pizza

read more

December 11, 2012

Appraising

,

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Manhattan

When We Say “Gut Rehab” We Mean It

read more

December 10, 2012

Analysis & Research

,

Appraising

,

Boom Bubble Bust

,

Celebrity, Pop Culture

,

Statistics, Metrics & Data

,

Wall Street, Financial Services

Serious Jibber-Jabber: Lessons from Nate Silver to Filter Out Housing Noise

read more

December 5, 2012

Adventures in Media & Marketing

,

Appraising

A La Mode Software Tells Our Appraisal Story

read more

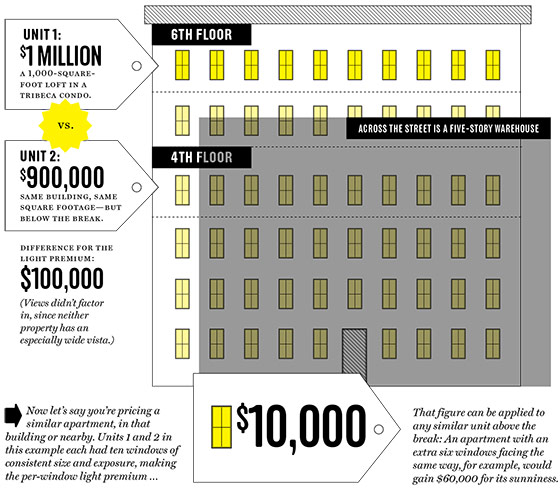

December 3, 2012

Amenities, Adjustments & Value Logic

,

Appraising

,

New York Magazine

,

New York Times

Valuing the Light in Your Condo or Co-op

read more

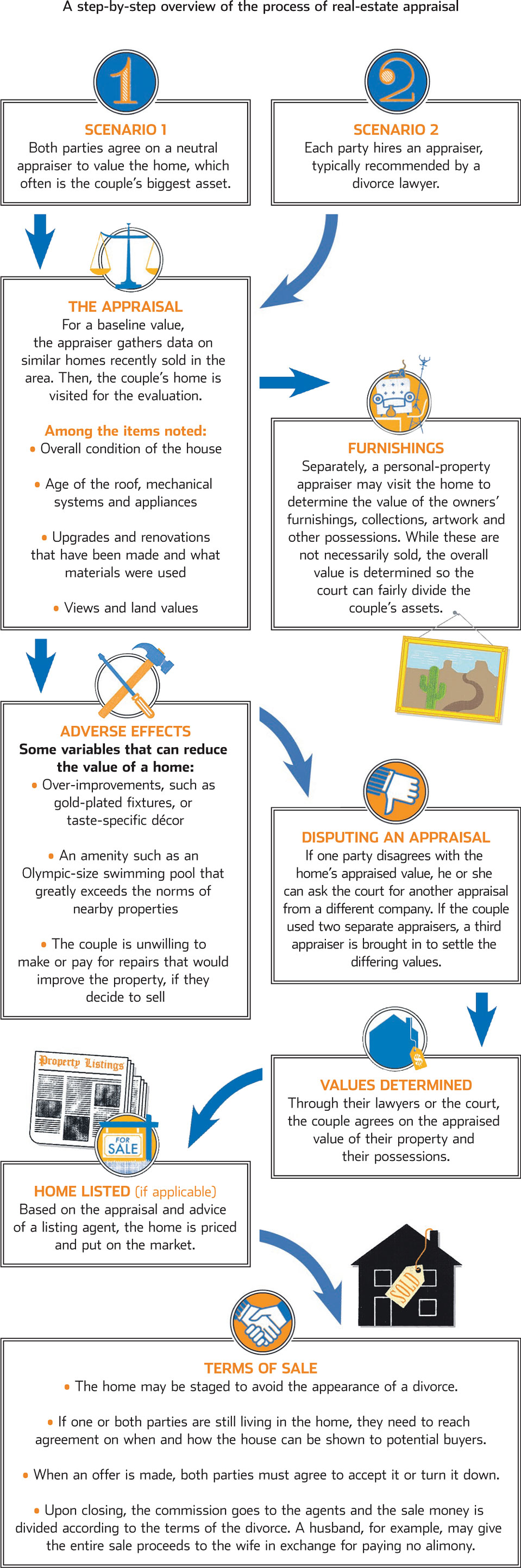

December 1, 2012

Appraising

,

Law, Ethics & Fraud

,

Media

,

Wall Street Journal

Divorce Valuations: Appraiserville Meets Splitsville

read more

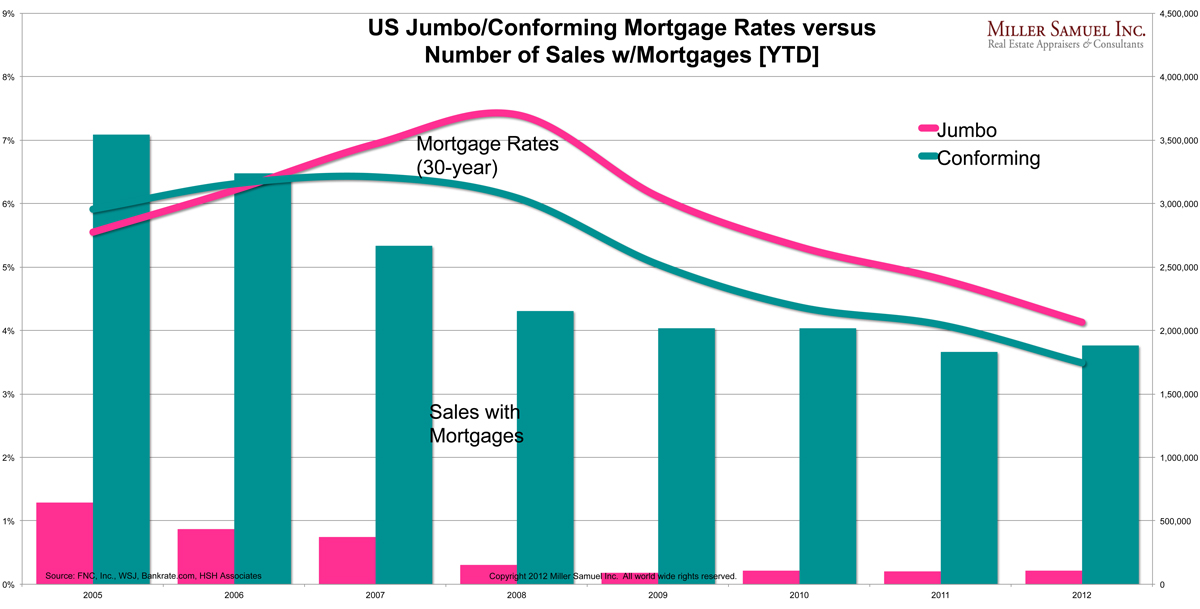

November 27, 2012

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

Get Down With It: Falling Mortgage Rates Are Not Creating Housing Sales

read more

November 6, 2012

Amenities, Adjustments & Value Logic

,

Appraising

,

International

,

Knight Frank

,

Luxury, Super, Ultra, Mega

,

Market Reports

,

New York Magazine

,

The Real Deal

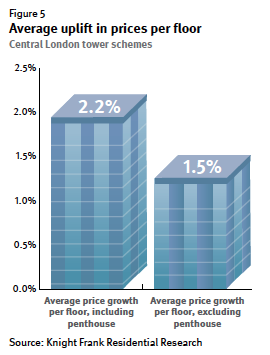

Knight Frank Tall Towers Report Shows London With Similar Manhattan Height Premium

read more

Previous

5

6

7

Next

Load More Posts

Page load link

Go to Top