Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Appraising

September 28, 2012

Adventures in Media & Marketing

,

Appraising

,

Celebrity, Pop Culture

,

Manhattan

,

Media

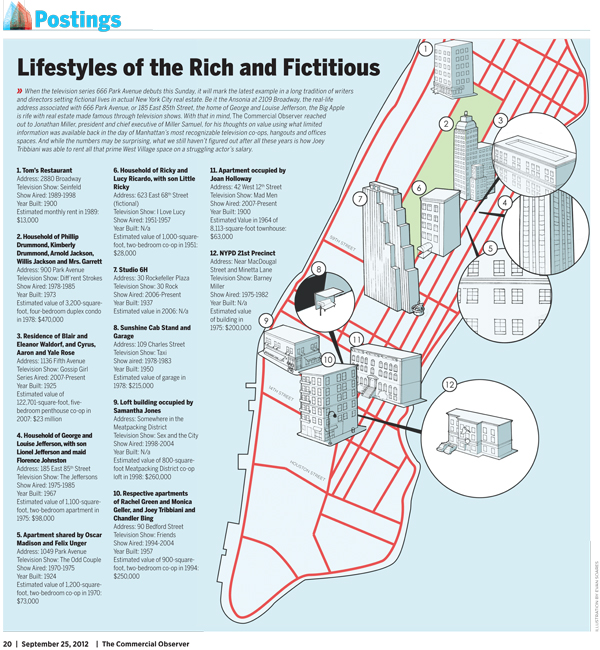

[666 Park Avenue] Appraising Fictitious TV Celebrity Apartments

read more

September 25, 2012

Appraising

,

Elliman Reports

,

Housing Indices & Portals

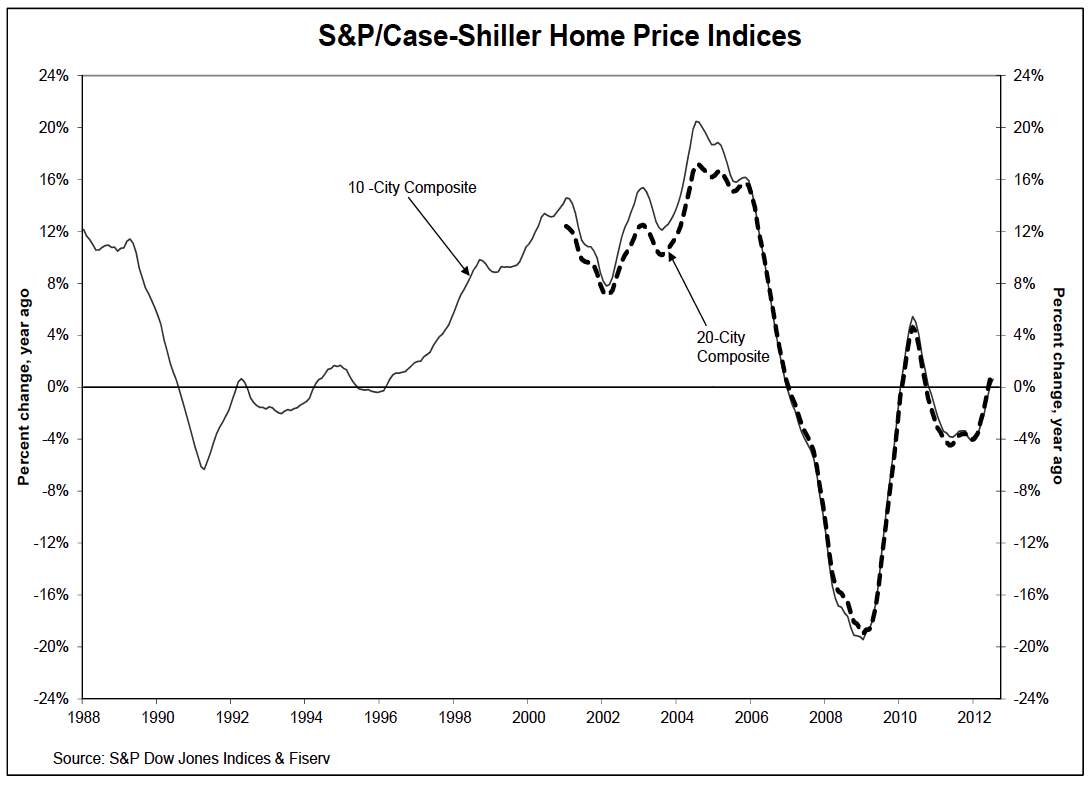

[Breaking News] CNN Gives Housing Followers Heart Attack, Case Shiller Up 1.2% YOY

read more

September 6, 2012

Appraising

,

Manhattan

,

Media

,

New York Magazine

Literally The Narrowest Housing Insight Ever Provided (Hint: Valuing Outdoor Space)

read more

September 3, 2012

Appraising

,

Social, Tech, Gadgets, Software

[a la mode] Here’s My Testimonial For Their Appraisal Software

read more

August 30, 2012

Appraising

,

Commercial, Retail

[Appraising The Decade] Miller Cicero’s 10-Year Anniversary

read more

July 23, 2012

Appraising

,

Homebuying Process

,

Media

Money Mag Shows Us How To ‘Think Like an Appraiser’

read more

July 23, 2012

Appraising

,

International

,

Media

,

New York Times

Why “Pull From Air” (P.F.A.) Is An Appraisal Term, Pig v. Sheep Explained

read more

July 9, 2012

Appraising

,

Credit, Finance, Mortgage, Rates

,

Social, Tech, Gadgets, Software

[a la mode] I Find Myself in an Ad for Appraisal Software

read more

June 22, 2012

Amenities, Adjustments & Value Logic

,

Appraising

,

Credit, Finance, Mortgage, Rates

,

Curbed

9 Feet Under: Some Thoughts About Valuing Basements and Cellars

read more

June 7, 2012

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

IRS

‘Defensibility’ of Property Values [Part II of Trilogy]

read more

May 22, 2012

Appraising

,

Canada

[Vortex] Did We Get There? The Promise of Licensing Appraisers

read more

May 21, 2012

Appraising

,

Social, Tech, Gadgets, Software

A Twitter Shout-out from Valuation Review on their 10th Anniversary

read more

Previous

6

7

8

Next

Load More Posts

Page load link

Go to Top