Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Appraising

May 21, 2012

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Guest Post (Vortex)

[Vortex] ‘Sustainability’ of Property Values [Part I of Trilogy]

read more

November 18, 2010

Analysis & Research

,

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

Interviews

,

Market Reports

,

The Housing Helix

[Interview] Robert Dorsey, Chief Data and Analytics Officer, FNC Co-Founder

read more

September 15, 2010

Appraising

,

Continuing Education & Licensing

,

Government, Politics, Regulations & Policy

,

Interviews

,

The Housing Helix

[Interview] David C. Wilkes, Esq. CRE FRICS, Huff Wilkes & Cavallaro LLP, Chairman The Appraisal Foundation

read more

June 17, 2010

Appraising

,

Continuing Education & Licensing

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Guest Post (Vortex)

[Vortex] Palumbo on USPAP: The Fool’s Gold of AMC Licensing

read more

June 10, 2010

Appraising

,

Bloomberg News

,

Law, Ethics & Fraud

,

New York Times

[eAppraiseIT Lawsuit] Cuomo Can Proceed Action Over “Inflated”, “Bogus” Appraisals

read more

June 9, 2010

Amenities, Adjustments & Value Logic

,

Appraising

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

The Real Deal

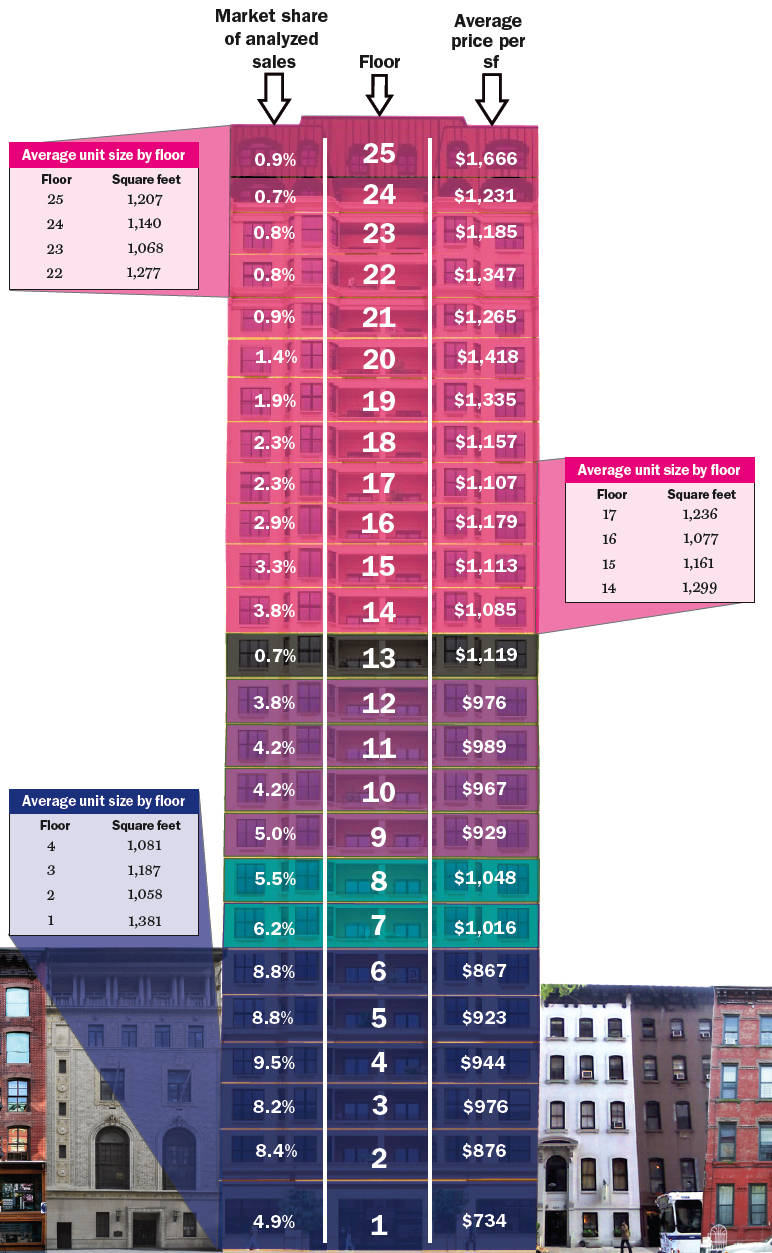

[ChartFloor] Manhattan Price Per Floor Breakdown

read more

June 7, 2010

Appraising

,

Brooklyn

[Brownstoner] Navigating Property Values Through Mass Opinions

read more

June 3, 2010

Adventures in Media & Marketing

,

Appraising

Don’t Assume Your Customers/Clients Are Giving Endorsements

read more

June 2, 2010

Appraising

,

Credit, Finance, Mortgage, Rates

,

New York Times

[Westwood Capital] Punting On Financial Industry Regulatory Reform

read more

May 18, 2010

Adventures in Media & Marketing

,

Appraising

,

Media

,

New York Times

,

Wall Street Journal

[Newspaper Wars] Appraisers Finally Get Editorial Recognition

read more

May 13, 2010

Appraising

,

Credit, Finance, Mortgage, Rates

,

The Housing Helix

[The Housing Helix Podcast] Chris Williams, President and Chief Technology Officer, AIMSdashboard

read more

May 13, 2010

Appraising

,

Credit, Finance, Mortgage, Rates

,

Interviews

,

Social, Tech, Gadgets, Software

,

The Housing Helix

[Interview] Chris Williams, President and Chief Technology Officer, AIMSdashboard

read more

Previous

7

8

9

Next

Load More Posts

Page load link

Go to Top