Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Government, Politics, Regulations & Policy

May 21, 2023

Appraising

,

Government, Politics, Regulations & Policy

,

Washington DC

Three Hours On C-SPAN Yields One Granddaughter

read more

May 1, 2021

Appraising

,

Bloomberg Radio

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Note

,

Housing Trends & Cycles

[Podcast] Masters In Business: Jonathan Miller on the Real Estate Industry

read more

August 19, 2020

Appraising

,

Government, Politics, Regulations & Policy

,

Housing Note

,

Law, Ethics & Fraud

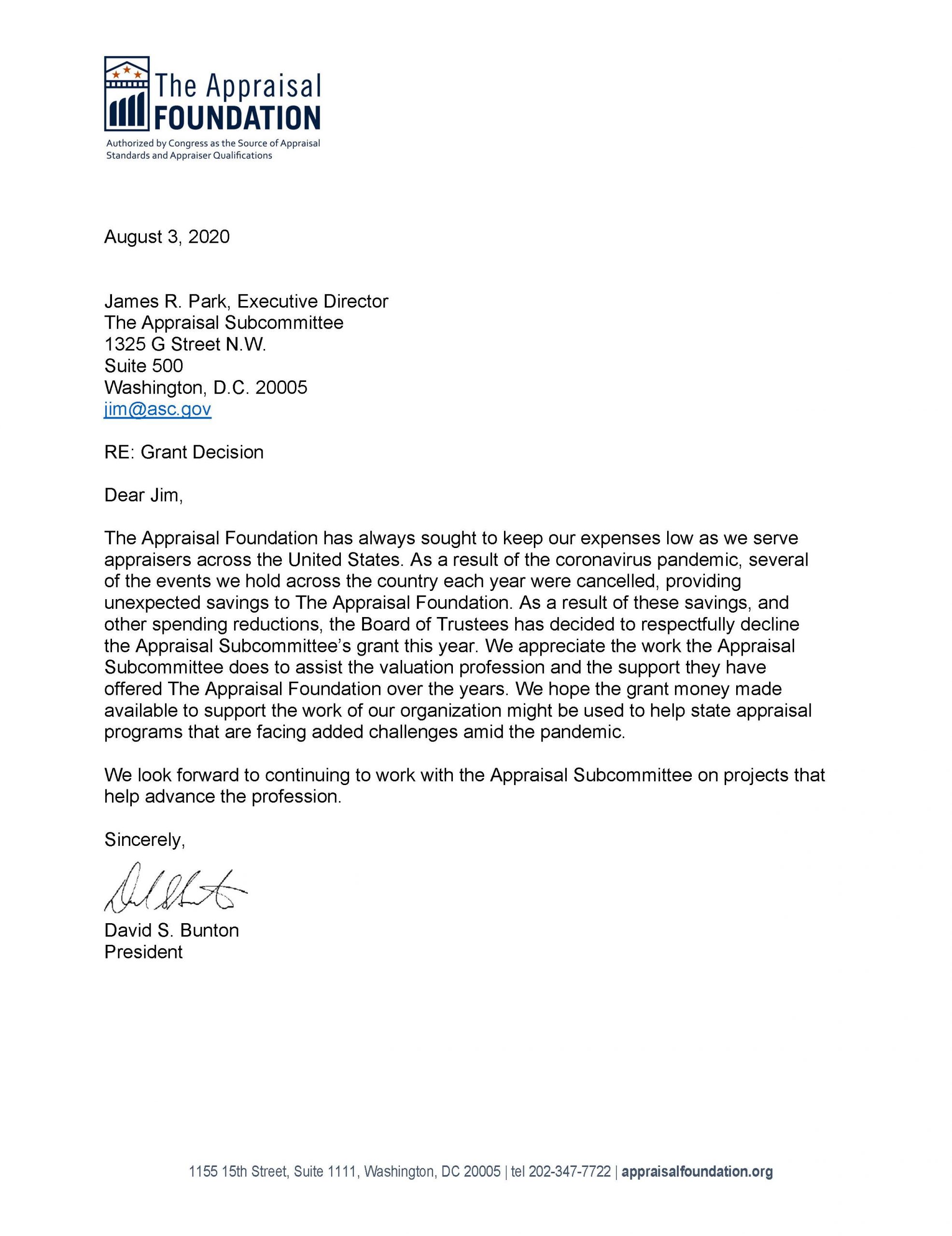

With All That PPP And Without All That Travel, The Appraisal Foundation Doesn’t Need A Grant From ASC This Year

read more

July 25, 2020

Appraising

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

The Previous Victim Of The Appraisal Institute Sham Election Maneuver Shares What Happened

read more

May 20, 2020

Charts, Maps, Images, Infographics, Video

,

Dutchess County, NY

,

Government, Politics, Regulations & Policy

,

Hamptons/North Fork

,

Manhattan

,

New York City

,

Putnam County

,

Weather & Natural Disasters

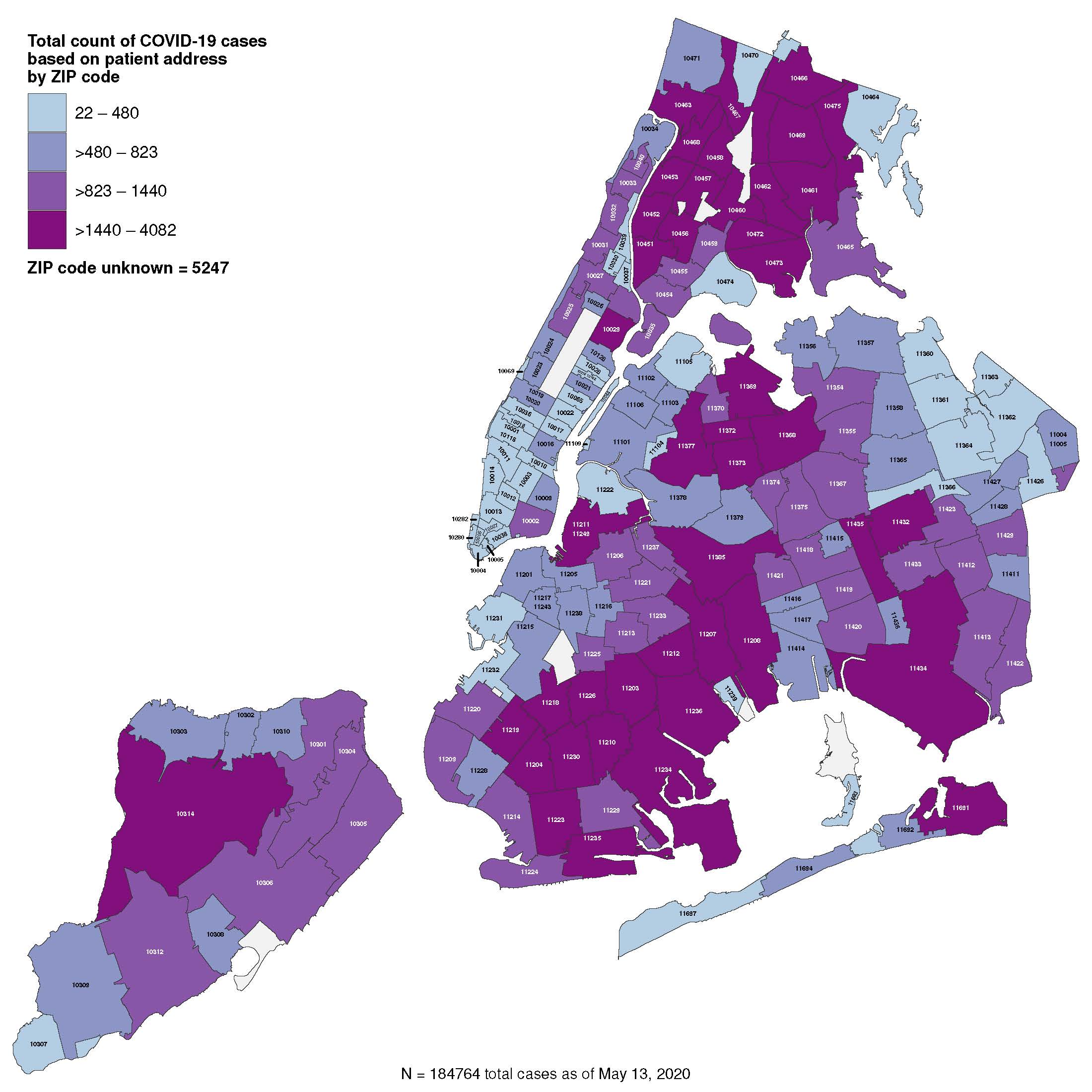

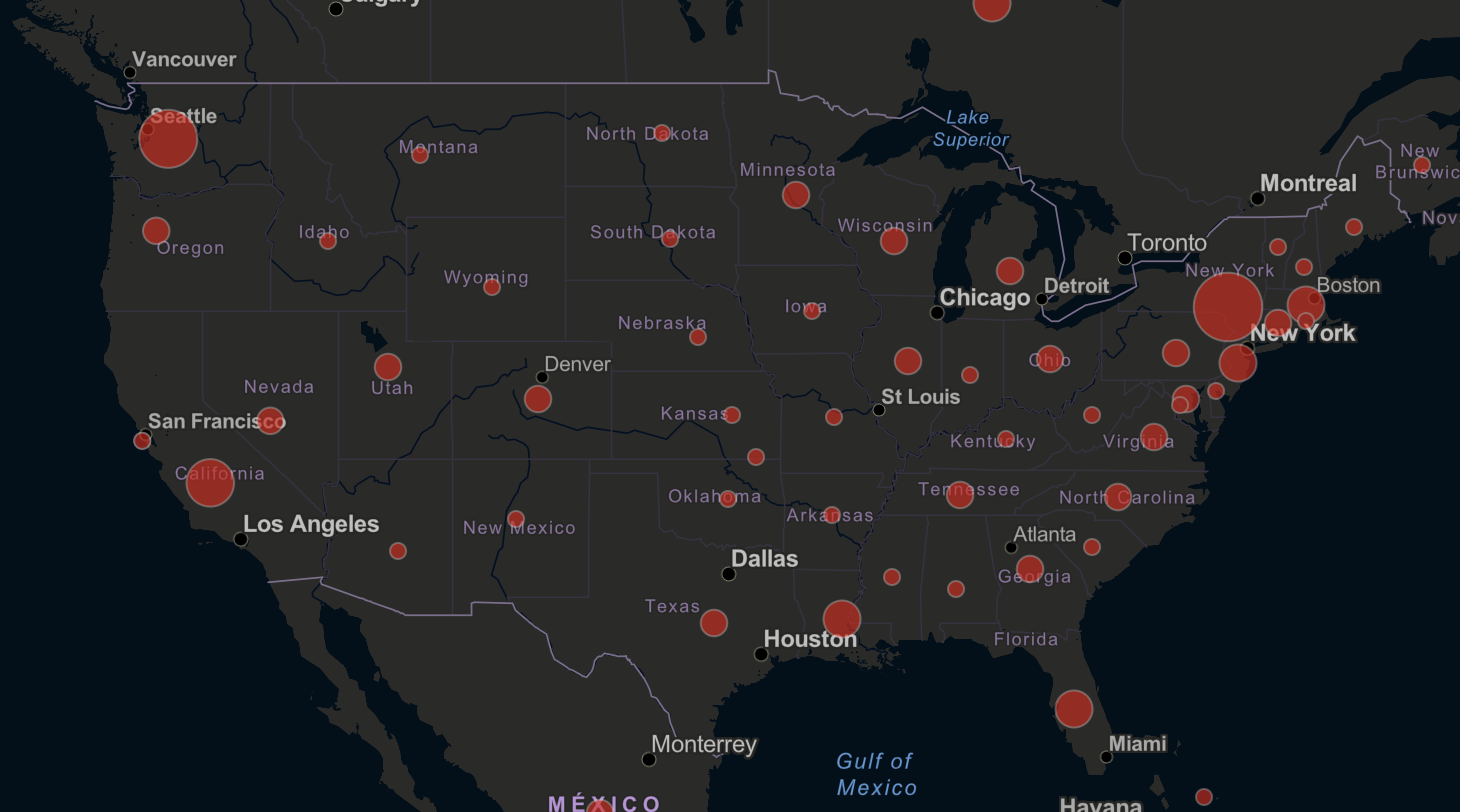

The Overstated COVID-19 Blame on Urban Density in Favor of Suburban Living

read more

May 3, 2020

Government, Politics, Regulations & Policy

,

New York City

,

New York City Suburbs

,

Suburban, Urban, Commuting

,

Weather & Natural Disasters

ABC World News Report 5-2-20 ‘Urban to Suburban’

read more

April 28, 2020

Amenities, Adjustments & Value Logic

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Historical, Landmark, Milestone

,

Housing Note

,

Manhattan

,

Weather & Natural Disasters

Establishing the COVID-19 Demarcation Line: From ‘Hanks To Banks’

read more

March 24, 2020

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Weather & Natural Disasters

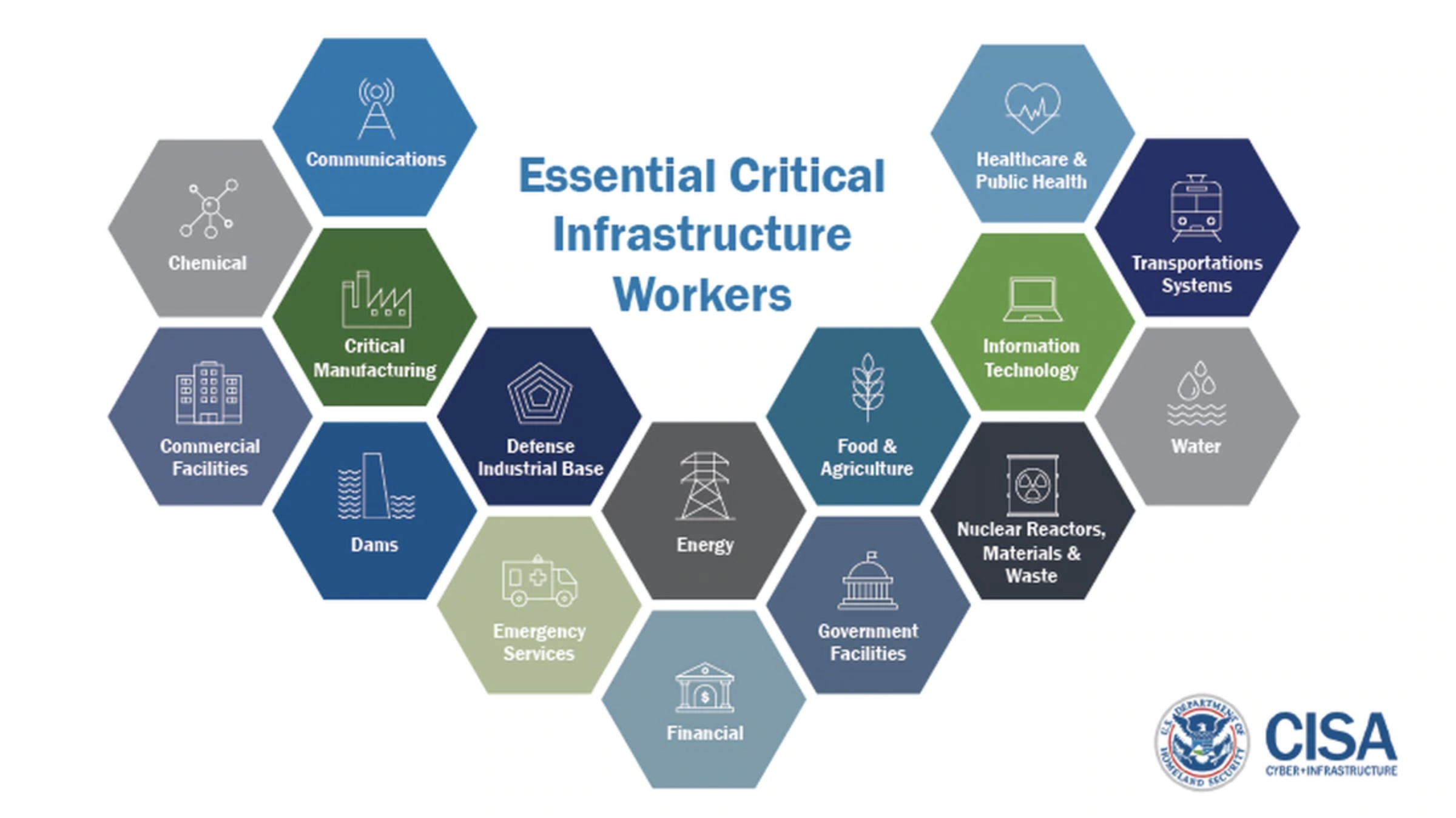

Real estate appraisers are an essential business and here to protect the public trust

read more

March 18, 2020

Appraising

,

Explainer

,

Government, Politics, Regulations & Policy

Some Financial Institutions Care About The Safety Of Appraisers, While Most Do Not

read more

February 5, 2020

Charts, Maps, Images, Infographics, Video

,

Government, Politics, Regulations & Policy

,

Manhattan

,

The Real Deal

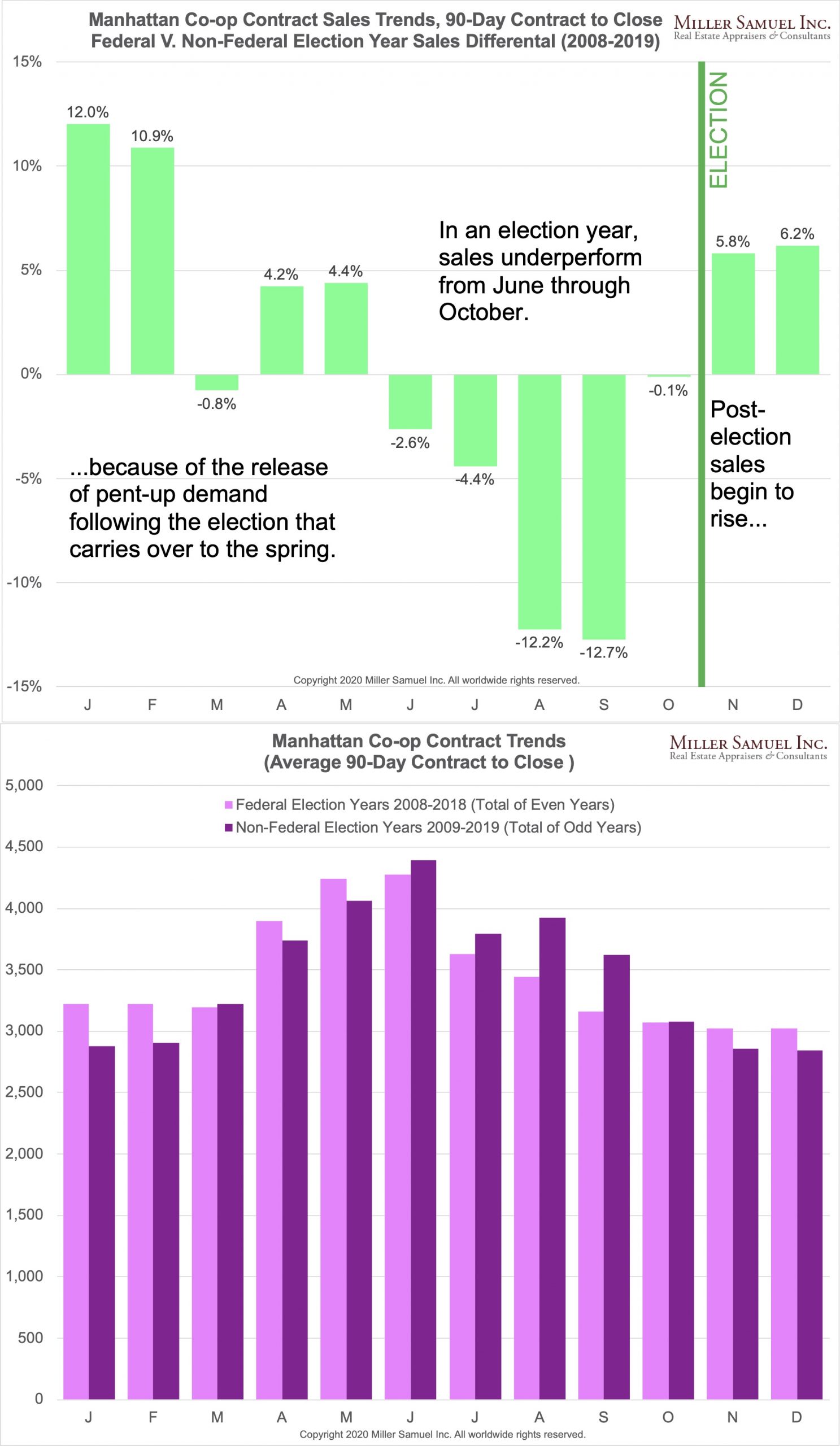

Manhattan Co-op Sales Fall During Federal Election Year

read more

January 23, 2020

Affordability, Affordable Housing

,

Brick Underground

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

The Brick Underground Podcast: 1-23-20 Talking Peak Uncertainty

read more

September 26, 2019

Amenities, Adjustments & Value Logic

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Trends & Cycles

,

Manhattan

Talking Manhattan Podcast: The Market’s Underlying Issues, and How to Value Outdoor space

read more

1

2

Next

Load More Posts

Page load link

Go to Top