Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Housing Trends & Cycles

February 22, 2024

Analysis & Research

,

Economy

,

Explainer

,

Housing Trends & Cycles

[27 Speaks Podcast] Jonathan Miller Provides A 2024 Hamptons Outlook

read more

January 23, 2024

Affordability, Affordable Housing

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Homebuying Process

,

Housing Trends & Cycles

Central Bank Central Video Podcast: Miller Samuels’ Chief Sees Stubbornly High Mortgage Rates, Low Inventories

read more

September 5, 2023

Bloomberg Radio

,

Homebuying Process

,

Housing Trends & Cycles

Bloomberg’s Masters in Business: Jonathan Miller on High Mortgage Rates

read more

August 1, 2023

Bloomberg TV

,

Housing Trends & Cycles

,

Sales

Bloomberg Surveillance 8-1-23: The Pandemic Wiped Out Housing Inventory: Miller

read more

July 18, 2023

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Housing Trends & Cycles

,

Language, Jargon & Quotes

,

Social, Tech, Gadgets, Software

[Business of Home Podcast] A Real Estate Check-In With Jonathan Miller

read more

December 8, 2022

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Housing Trends & Cycles

,

New York City

,

New York City Suburbs

,

Statistics, Metrics & Data

Elliman Magazine Column “Market Update” – New Inventory Is Falling

read more

October 10, 2022

Analysis & Research

,

Appraising

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Homebuying Process

,

Housing Trends & Cycles

,

Public Speaking

[Podcast] Slate Money: Felix Learns What A Condo Is – Jonathan Miller joins to talk all things real estate.

read more

April 14, 2022

Douglas Elliman

,

Elliman Reports

,

Housing Trends & Cycles

,

Statistics, Metrics & Data

Elliman Magazine Column – A Symptom of Chronic Inventory Lows: Bidding Wars Are Everywhere

read more

November 7, 2021

Analysis & Research

,

Explainer

,

Homebuying Process

,

Housing Indices & Portals

,

Housing Trends & Cycles

Zillow Offers As A Proxy For ‘Big Data’ Shows The Lack Of Qualitative Analysis

read more

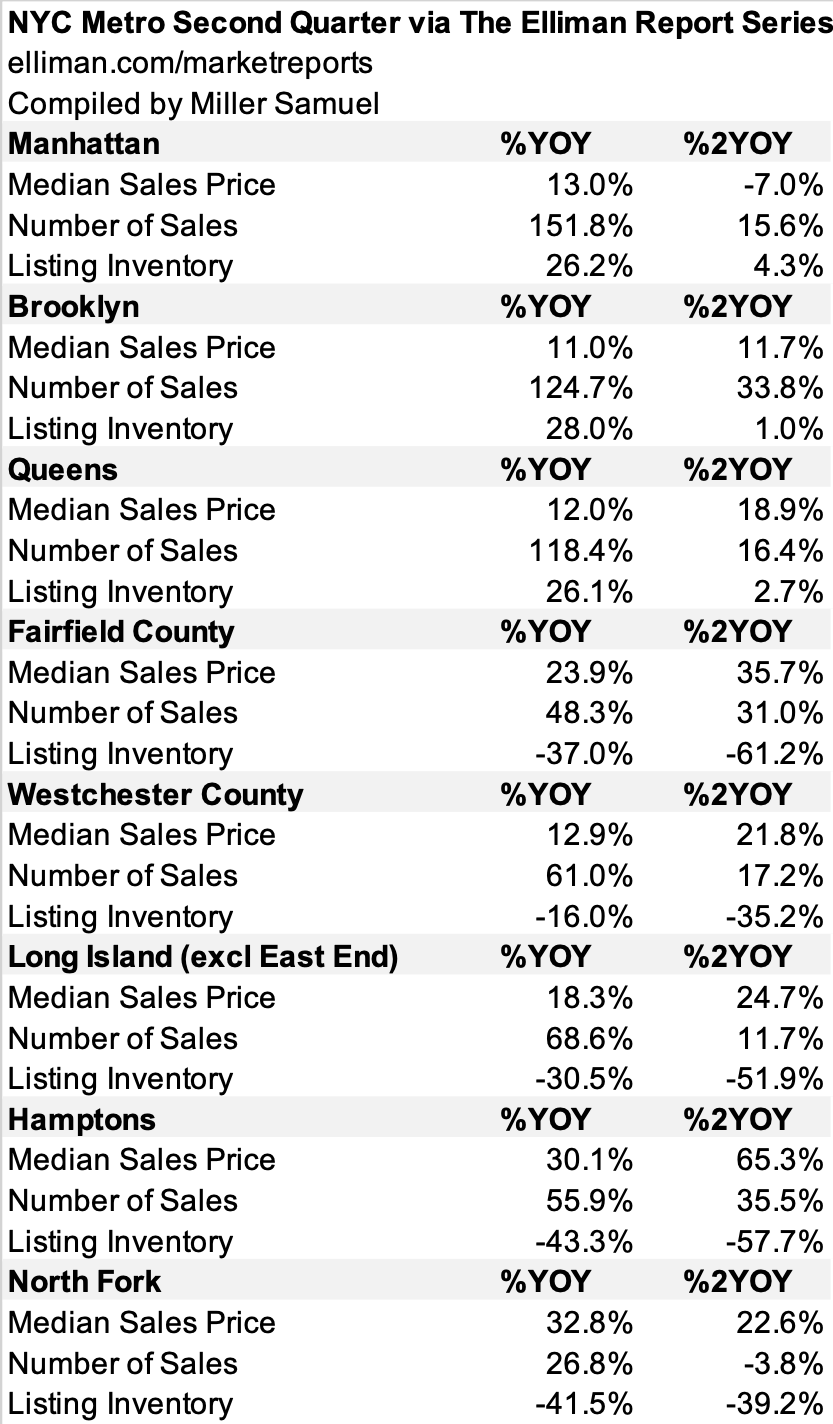

August 20, 2021

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Fairfield County, CT

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

Queens

,

Westchester County, NY

NYC Metro Conditions Much More Robust Than Two Years Ago

read more

June 18, 2021

Elliman Reports

,

Housing Trends & Cycles

,

Long Island

TV: Newsday Live: Hot Tips For a Hot Market: For Sellers

read more

May 1, 2021

Appraising

,

Bloomberg Radio

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Note

,

Housing Trends & Cycles

[Podcast] Masters In Business: Jonathan Miller on the Real Estate Industry

read more

1

2

Next

Load More Posts

Page load link

Go to Top