Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Housing Trends & Cycles

August 5, 2014

Blogging Off The Matrix

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York City

,

Queens

,

Records, Thresholds and Outliers

[Three Cents Worth #267 NY] NYC Sets New Record Average Sales Price

read more

July 1, 2014

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Housing Trends & Cycles

,

Manhattan

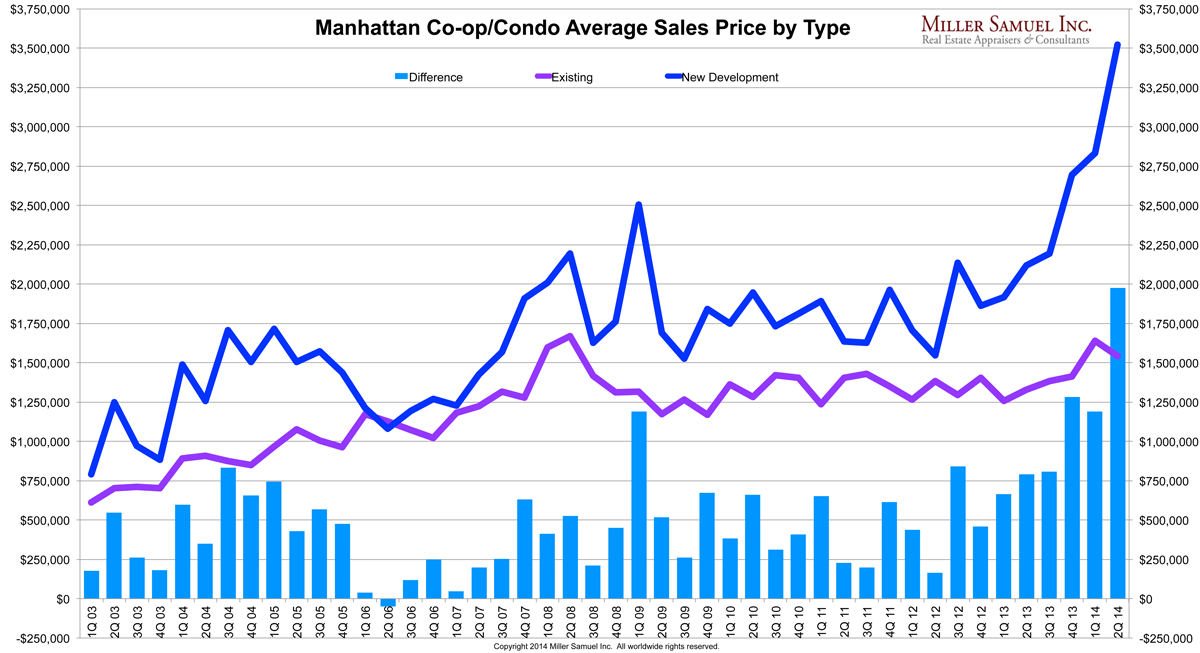

Rocket Ship: Manhattan New versus Existing Average Sales Price

read more

June 24, 2014

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Housing Indices & Portals

,

Housing Trends & Cycles

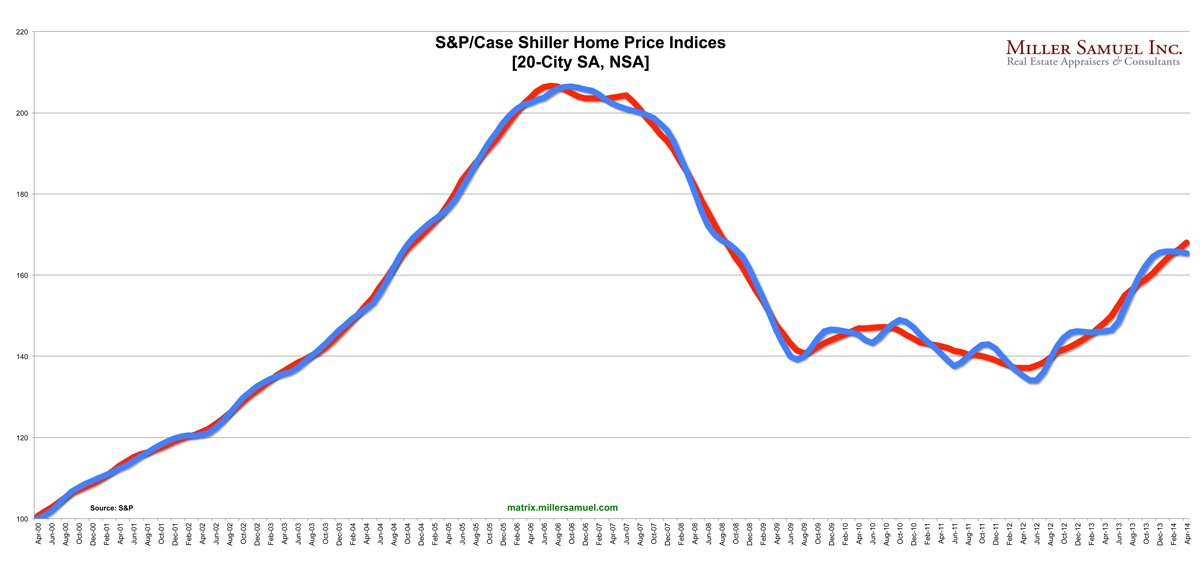

Time-Shifted Case Shiller: Dallas, Denver Crushing it, Polar Vortex a Non-Issue ‘Cause It’s Still December

read more

June 23, 2014

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

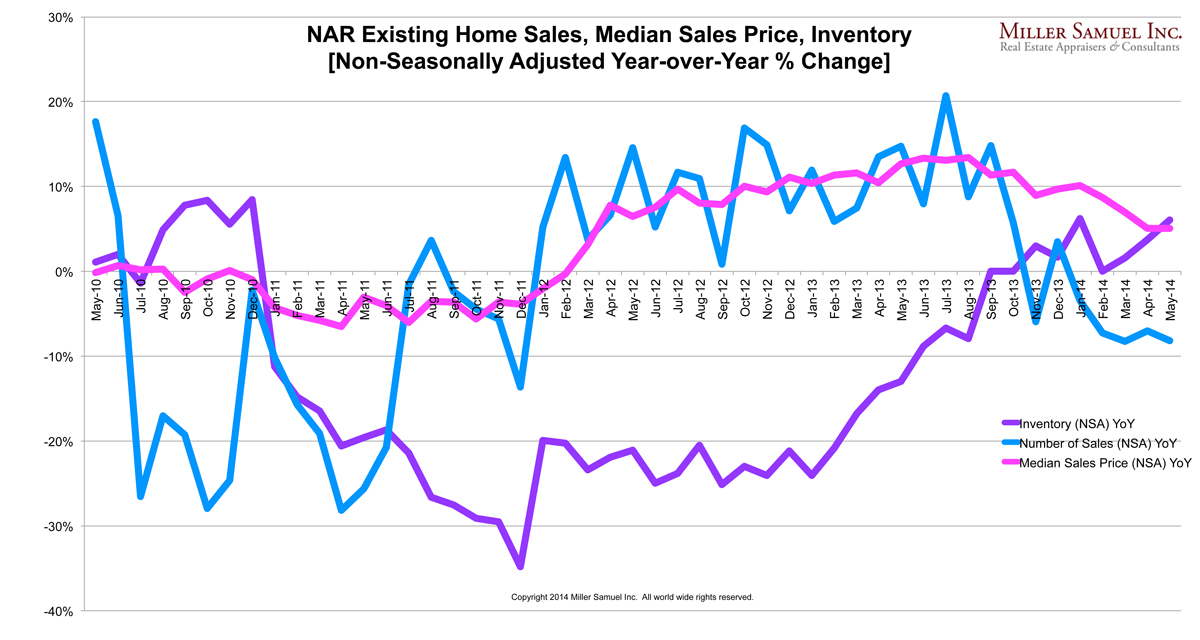

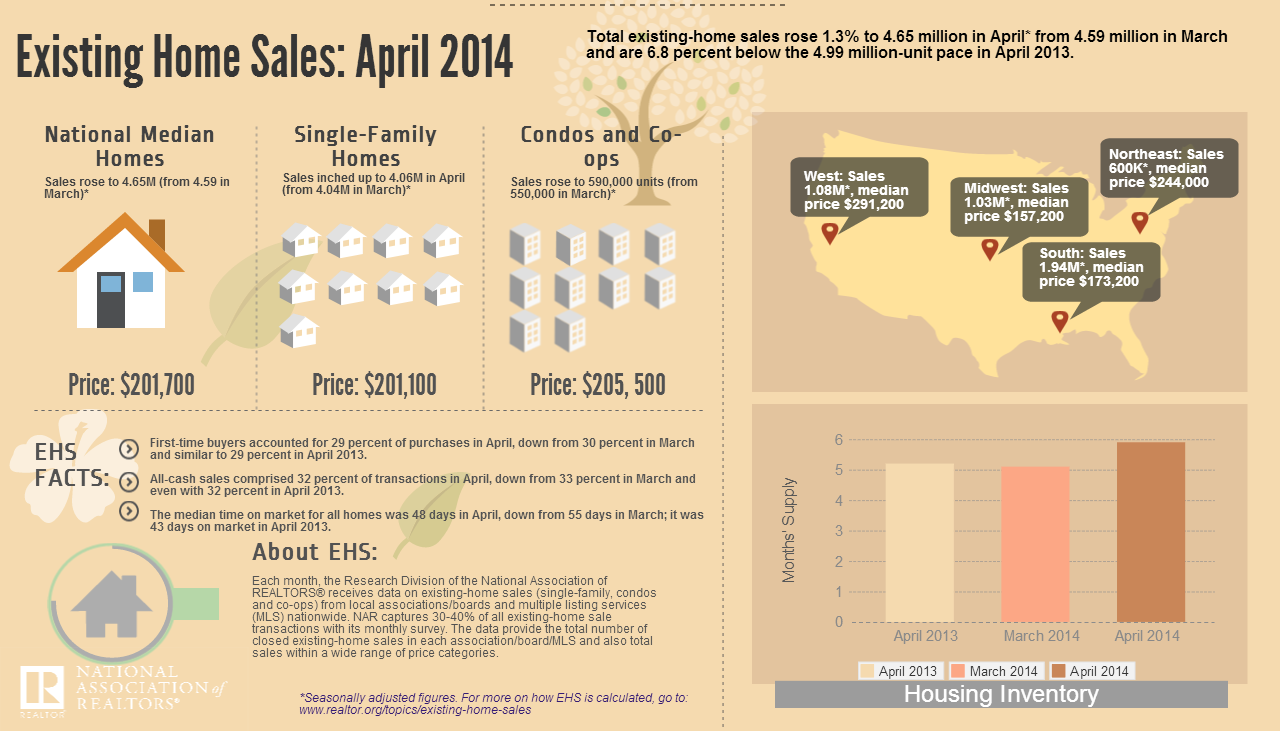

NAR May 2014 Existing Home Sales: ‘Heat-up’

read more

June 20, 2014

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Douglas Elliman

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Sales

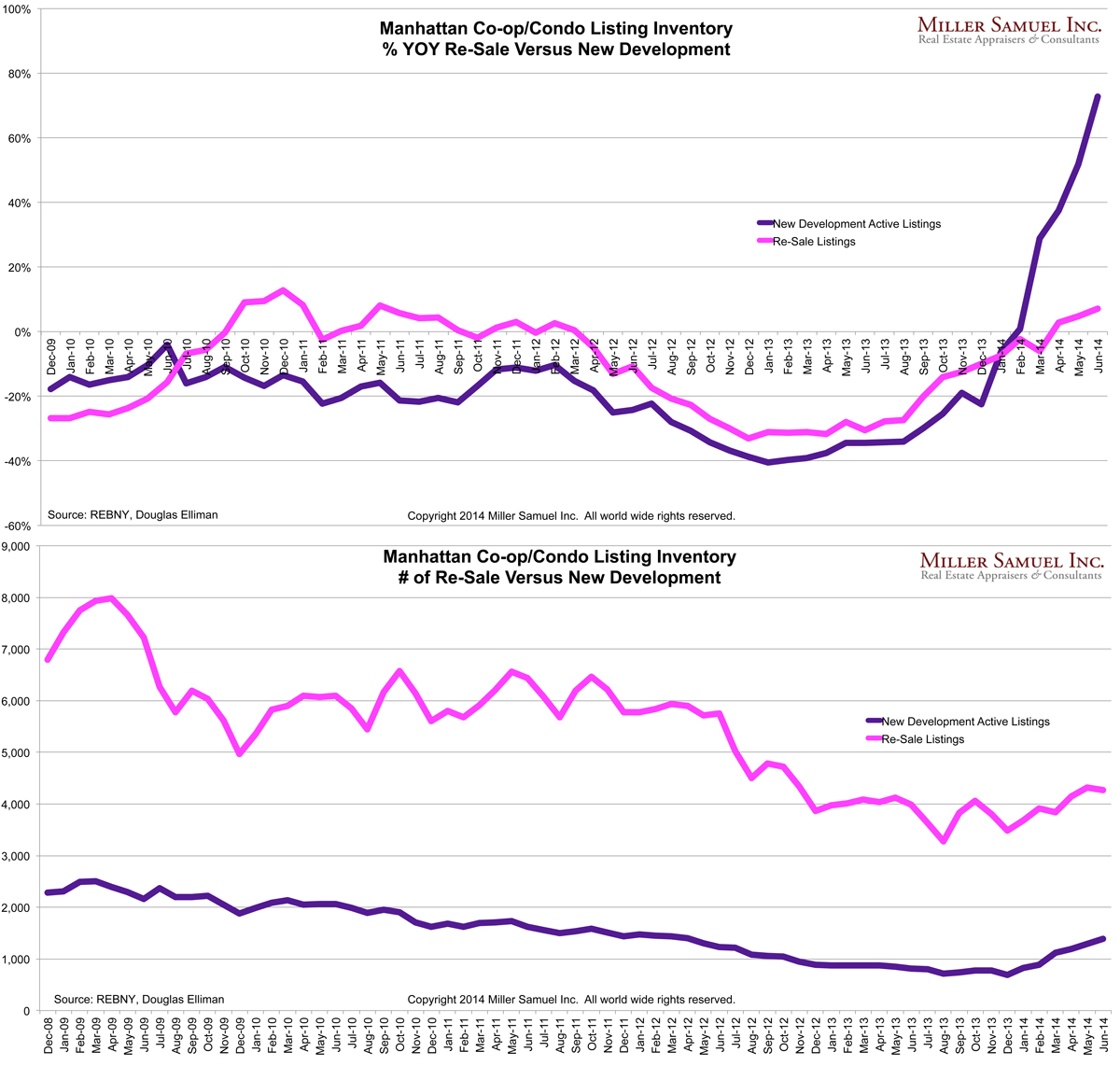

Manhattan New Development: Small Share, But Rising Sharply

read more

June 12, 2014

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Housing Trends & Cycles

,

Manhattan

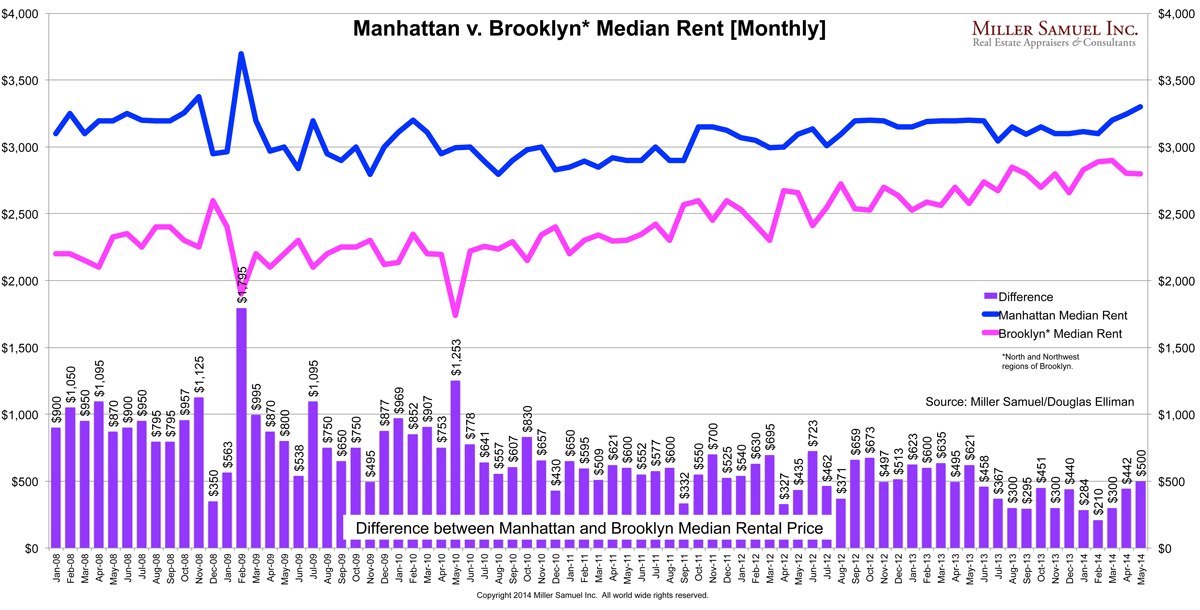

Manhattan-Brooklyn Rental Price Spread Widens to $500

read more

June 9, 2014

Charts, Maps, Images, Infographics, Video

,

Distressed Housing

,

Housing Trends & Cycles

,

Op-Ed

,

Statistics, Metrics & Data

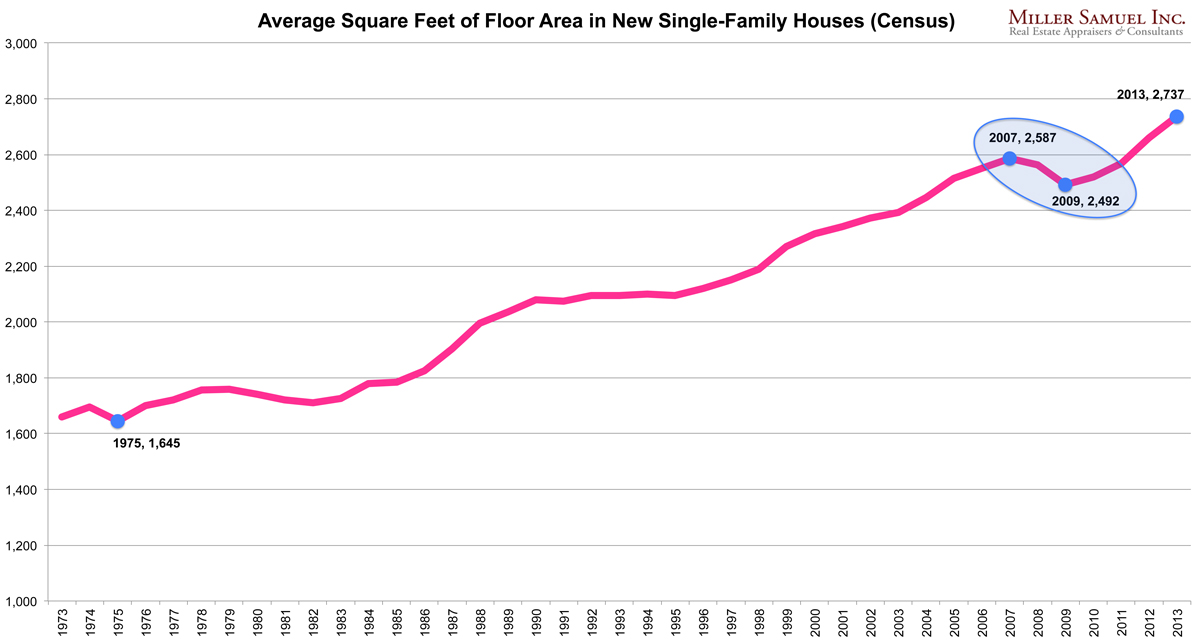

Trends in Home Size and Home Ownership React to Economic Conditions, Not Taste

read more

June 9, 2014

Appraising

,

Books & Movies

,

Development, Construction, Architecture & Land

,

Environmental

,

Housing Trends & Cycles

,

International

,

Luxury, Super, Ultra, Mega

[London Calling] ‘Mike Mulligan and his Steam Shovel’ New Development Edition

read more

June 8, 2014

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Housing Trends & Cycles

,

Manhattan

[Manhattan Absorption] May 2014 – Swimming in high-end condos.

read more

May 29, 2014

Housing Trends & Cycles

,

Market Reports

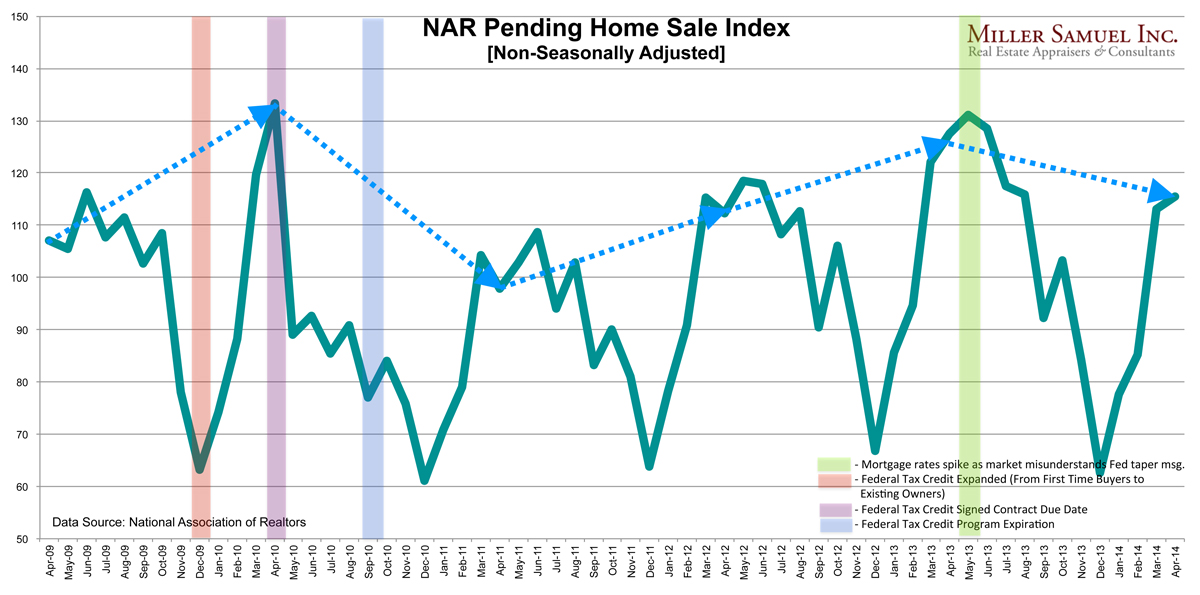

Pending Home Sales Fall Short of Year Ago Sales Surge

read more

May 27, 2014

Historical, Landmark, Milestone

,

Housing Indices & Portals

,

Housing Trends & Cycles

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

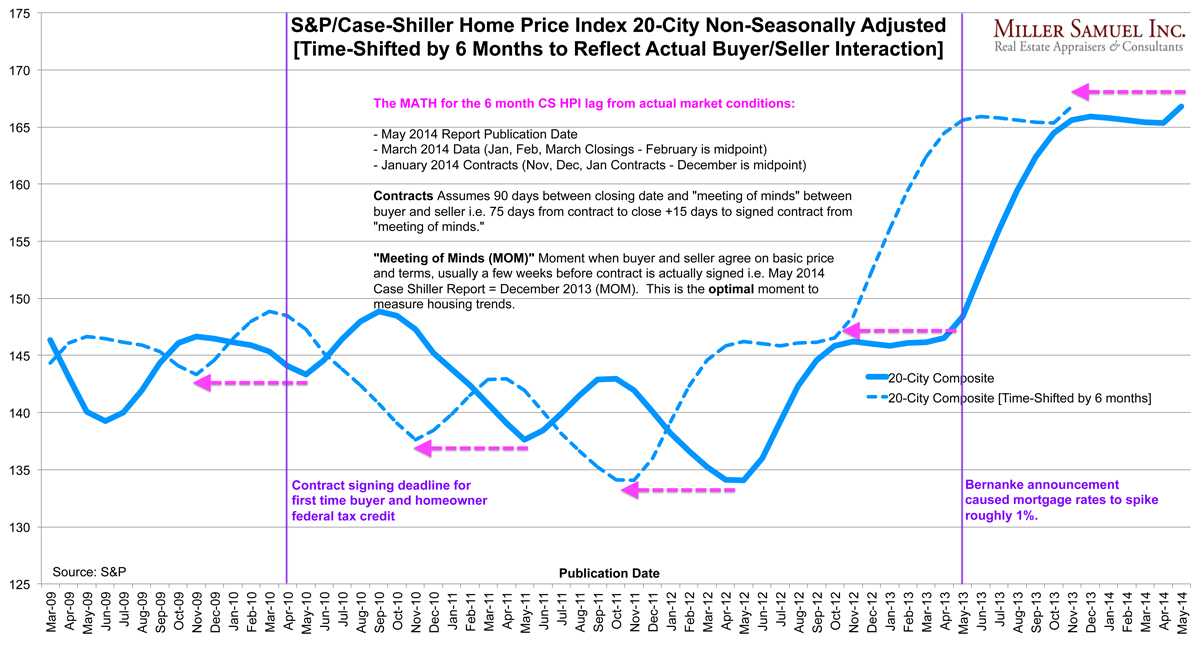

Pulling the Case-Shiller Index Back by 6 Months to Reflect Actual Buyer/Seller Behavior

read more

May 27, 2014

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

Thank Goodness The Pace of US Home Price Growth Will Cool

read more

Previous

7

8

9

Next

Load More Posts

Page load link

Go to Top