Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Law, Ethics & Fraud

March 15, 2014

Appraising

,

Charts, Maps, Images, Infographics, Video

,

Continuing Education & Licensing

,

Credit, Finance, Mortgage, Rates

,

Homebuying Process

,

Law, Ethics & Fraud

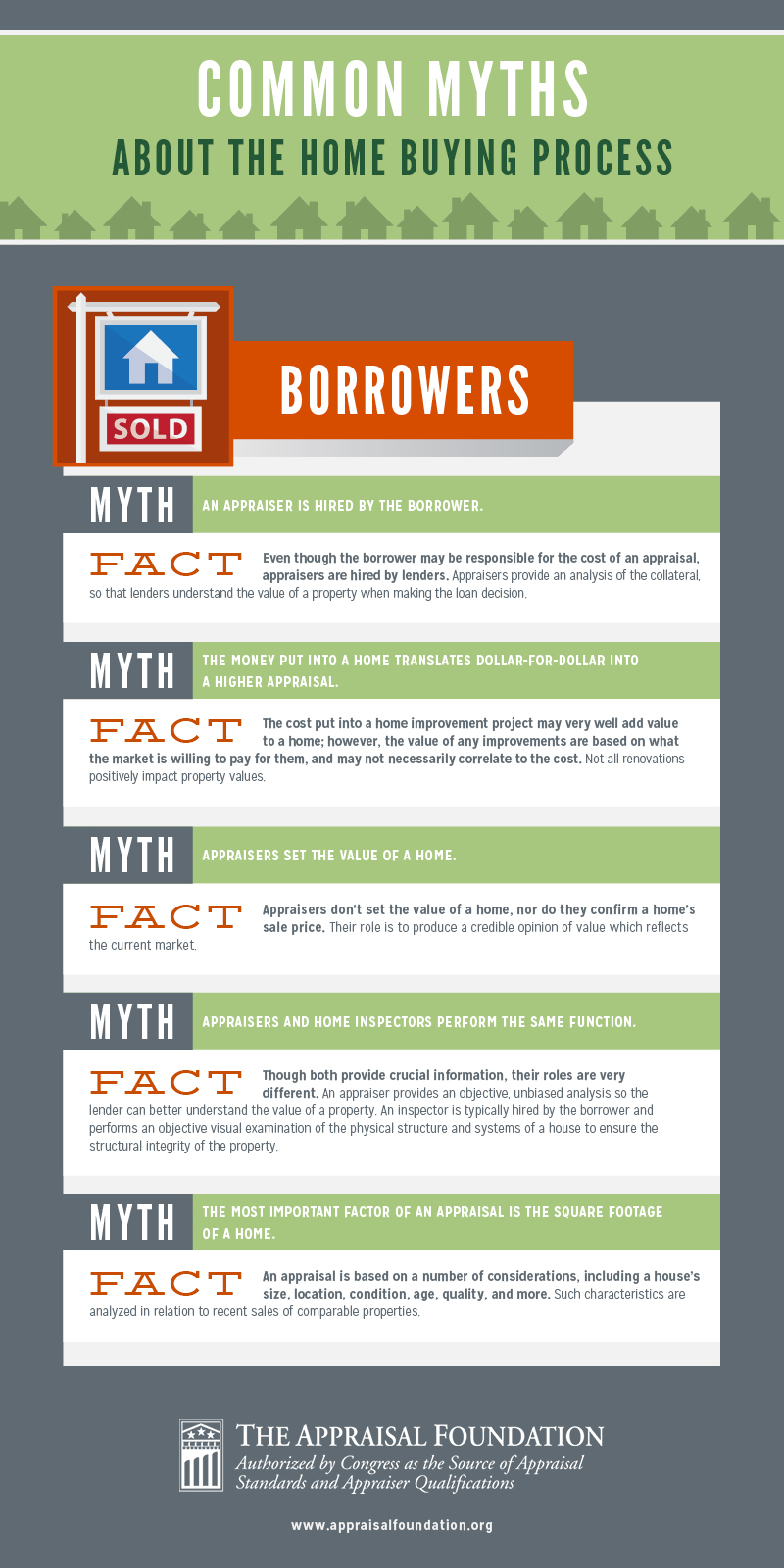

[Appraisal Infographic] Common Myths About The Homebuying Process

read more

February 24, 2014

Humor or Whimsy

,

Language, Jargon & Quotes

,

Law, Ethics & Fraud

Best Real Estate Lawsuit Prose EVER

read more

February 5, 2013

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Humor or Whimsy

,

Law, Ethics & Fraud

,

New York Times

Talking Heads: Burning Down The House, S&P Style

read more

December 1, 2012

Appraising

,

Law, Ethics & Fraud

,

Media

,

Wall Street Journal

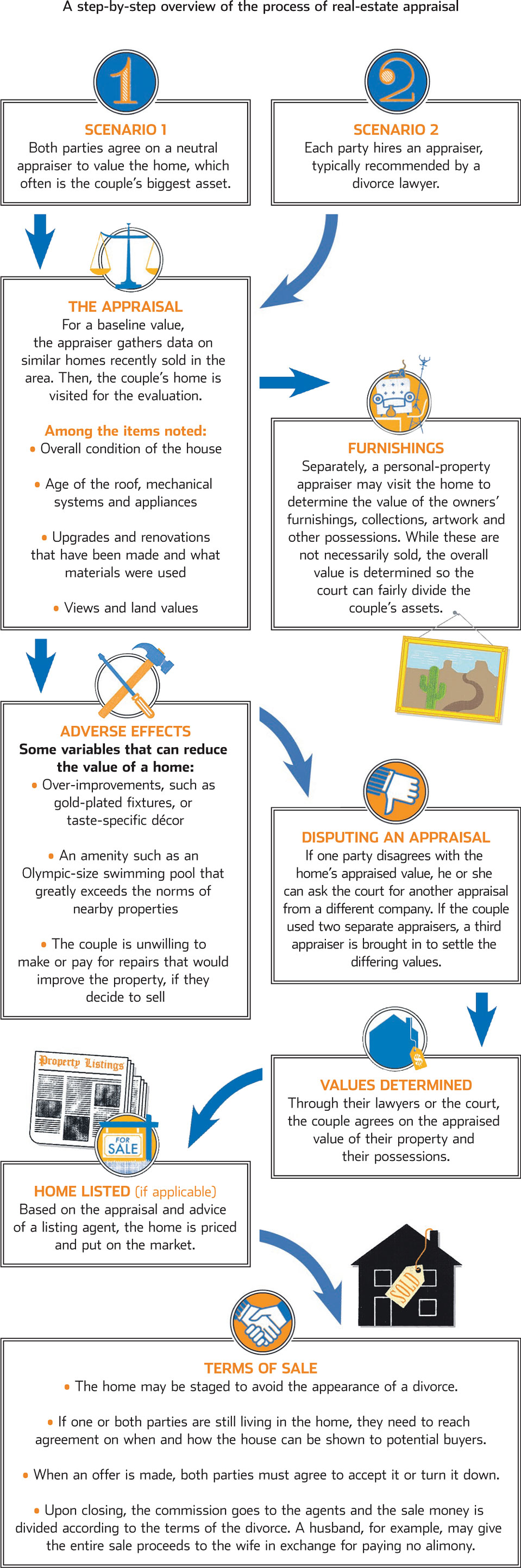

Divorce Valuations: Appraiserville Meets Splitsville

read more

June 11, 2012

Development, Construction, Architecture & Land

,

Law, Ethics & Fraud

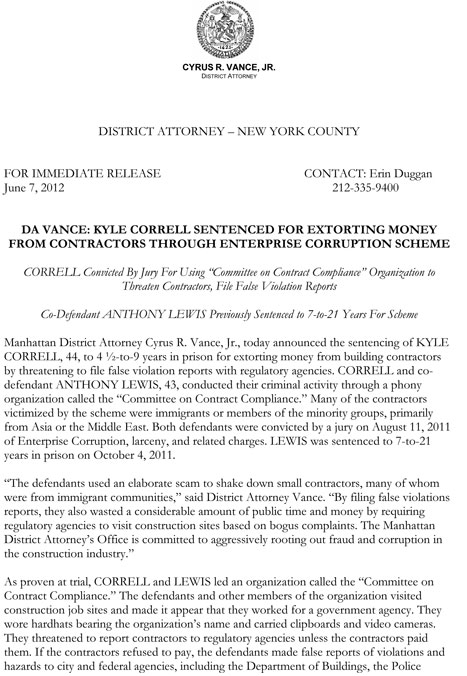

Fraud Never Sleeps – 2 Contractors Sentenced

read more

October 13, 2010

Development, Construction, Architecture & Land

,

Interviews

,

Law, Ethics & Fraud

,

New York Times

,

The Housing Helix

[Interview] Adam Leitman Bailey, Real Estate Attorney, Founder, Adam Leitman Bailey, P.C., Author

read more

June 14, 2010

Development, Construction, Architecture & Land

,

Law, Ethics & Fraud

,

New York Times

,

Taxes, Insurance, Fees

[Estate Tax] 2010: Throw Momma From the Train?

read more

June 10, 2010

Appraising

,

Bloomberg News

,

Law, Ethics & Fraud

,

New York Times

[eAppraiseIT Lawsuit] Cuomo Can Proceed Action Over “Inflated”, “Bogus” Appraisals

read more

April 25, 2010

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Interviews

,

Law, Ethics & Fraud

,

The Housing Helix

[Interview] Steven Einig, Esq, Einig & Bush LLP, Mortgage Foreclosures and Workouts

read more

March 16, 2010

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Law, Ethics & Fraud

,

New York Times

[HVCC and AMCs Violate RESPA?] Here’s a possible solution

read more

February 25, 2010

Interviews

,

Law, Ethics & Fraud

,

The Housing Helix

[Interview] Nancy Chemtob Esq., Chemtob Moss Forman & Talbert LLP

read more

February 22, 2010

Interviews

,

Law, Ethics & Fraud

,

New York Times

,

The Housing Helix

[Interview] Steven R. Wagner Esq., Wagner Davis, P.C.

read more

Previous

2

3

4

Next

Load More Posts

Page load link

Go to Top