Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Market Reports

June 21, 2010

IRS

,

Market Reports

,

Washington DC

[CoreLogic] Home Price Index 2.6% YOY and 0.8% MOM Increase

read more

June 17, 2010

Government, Politics, Regulations & Policy

,

Market Reports

,

Statistics, Metrics & Data

[Commerce Dept] US Housing Starts May 2010

read more

June 15, 2010

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Market Reports

[Shadow Inventory] S&P: New York Metro Highest at 103 Months

read more

June 14, 2010

IRS

,

Market Reports

[Harvard Study] Jobs Needed For Housing To Recover

read more

June 2, 2010

Brokers, Agents, MLS, NAR

,

IRS

,

Market Reports

,

Wall Street Journal

[NAR] Pending Home Sales Index

read more

May 25, 2010

Brokers, Agents, MLS, NAR

,

IRS

,

Market Reports

[NAR] Existing Home Sales Jump Artificially

read more

April 26, 2010

Housing Indices & Portals

,

Market Reports

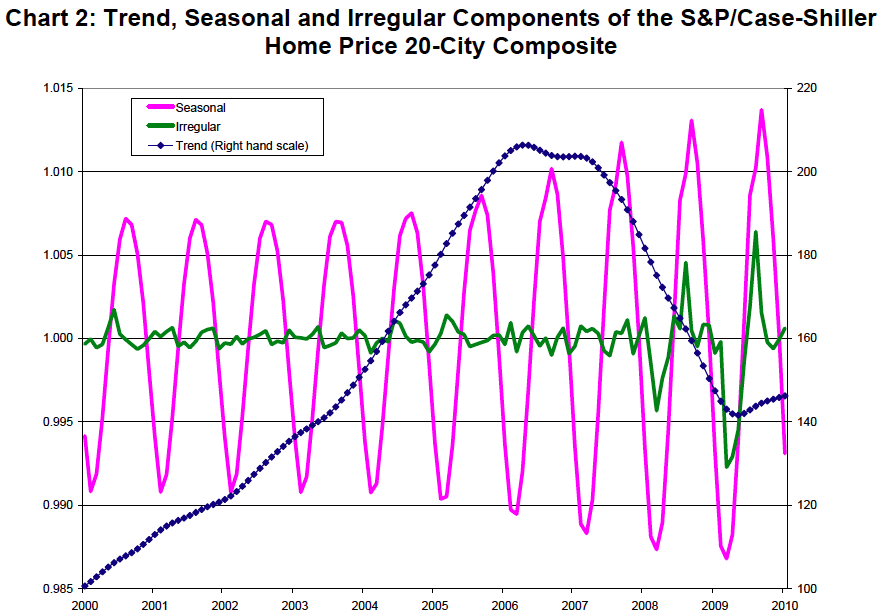

[Seasonality Adjustments] are Confusing and Perhaps, Misleading

read more

April 25, 2010

Analysis & Research

,

Market Reports

,

The Housing Helix

[Special Report] 1Q 2010 Hamptons/North Fork Market Overview

read more

April 25, 2010

Analysis & Research

,

Douglas Elliman

,

Market Reports

,

The Housing Helix

[Special Report] 1Q 2010 Long Island Market Overview

read more

April 22, 2010

Douglas Elliman

,

Elliman Reports

,

Hamptons/North Fork

,

Market Reports

[Back to Normal?] 1Q 2010 Hamptons/North Fork Market Overview Available For Download

read more

April 22, 2010

Douglas Elliman

,

Elliman Reports

,

Long Island

,

Market Reports

[Limping Into Better Times] 1Q 2010 Long Island Market Overview Available For Download

read more

April 19, 2010

Analysis & Research

,

Brooklyn

,

Market Reports

,

The Housing Helix

[Special Report] 1Q 2010 Brooklyn Market Overview

read more

Previous

4

5

6

Next

Load More Posts

Page load link

Go to Top