Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Statistics, Metrics & Data

December 8, 2022

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Housing Trends & Cycles

,

New York City

,

New York City Suburbs

,

Statistics, Metrics & Data

Elliman Magazine Column “Market Update” – New Inventory Is Falling

read more

April 14, 2022

Douglas Elliman

,

Elliman Reports

,

Housing Trends & Cycles

,

Statistics, Metrics & Data

Elliman Magazine Column – A Symptom of Chronic Inventory Lows: Bidding Wars Are Everywhere

read more

May 12, 2020

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Explainer

,

Housing Note

,

Housing Trends & Cycles

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Statistics, Metrics & Data

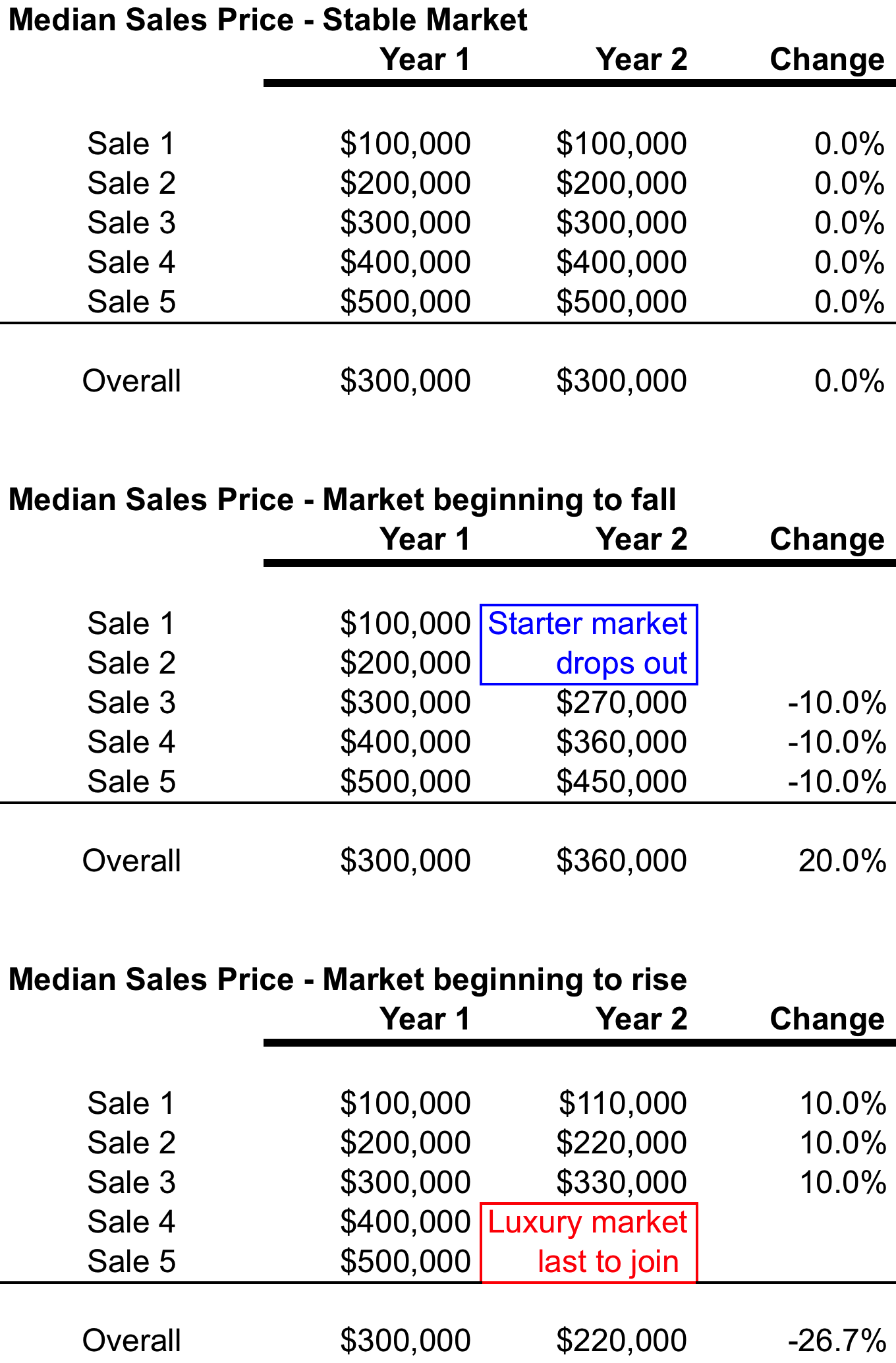

Median sales price can be subject to skew by consumer behavior more than math

read more

April 29, 2020

Analysis & Research

,

Brokers, Agents, MLS, NAR

,

Explainer

,

Housing Trends & Cycles

,

Statistics, Metrics & Data

Contract Data Is Pending Data Is Lagging Data

read more

May 16, 2019

Charts, Maps, Images, Infographics, Video

,

Elliman Reports

,

Hamptons/North Fork

,

Luxury, Super, Ultra, Mega

,

New York Times

,

Statistics, Metrics & Data

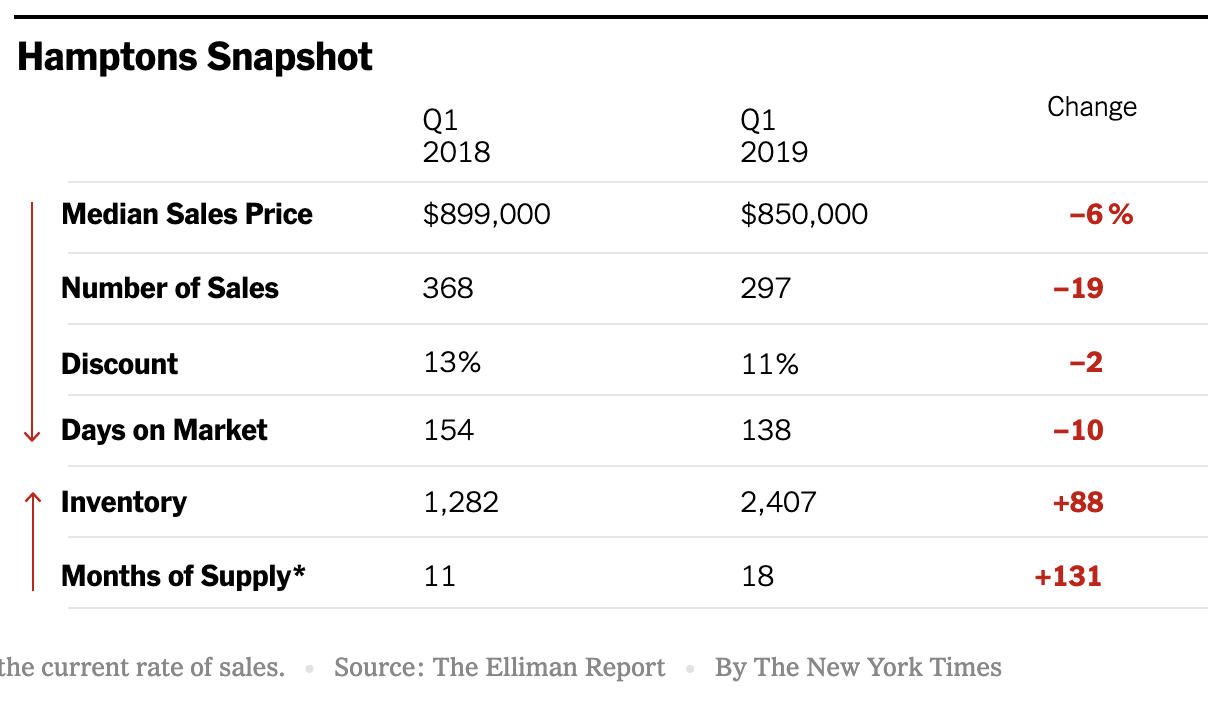

Hamptons Sellers Are Starting To Get The Message

read more

December 14, 2018

Aspen

,

Boca Raton

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Greenwich

,

Manhattan

,

Statistics, Metrics & Data

Elliman Magazine Winter 2019 – Market Update

read more

January 21, 2017

Charts, Maps, Images, Infographics, Video

,

Elliman Reports

,

Housing Trends & Cycles

,

Manhattan

,

New York Times

,

Statistics, Metrics & Data

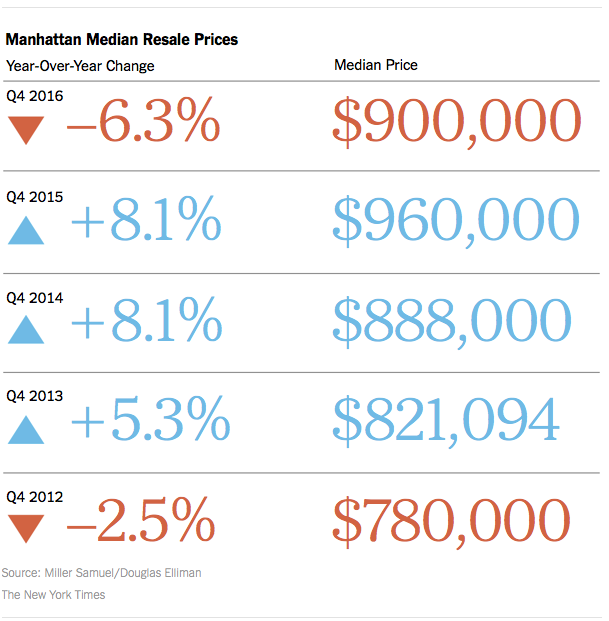

NYT Calculator Chart: The Resale Pendulum Swings Toward Middle

read more

June 3, 2015

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Douglas Elliman

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Manhattan

,

Market Reports

,

Sales

,

Statistics, Metrics & Data

,

Suburban, Urban, Commuting

,

Wall Street, Financial Services

[Three Cents Worth #288 Hamptons] Comparing Price Trends in the Hamptons and Manhattan

read more

May 30, 2015

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Curbed

,

Douglas Elliman

,

Housing Trends & Cycles

,

Manhattan

,

Statistics, Metrics & Data

[Three Cents Worth #286 NY] How Many NYC Apartments Are Bought With Cold Hard Cash?

read more

May 22, 2015

Aspen

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Douglas Elliman

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

,

Records, Thresholds and Outliers

,

Statistics, Metrics & Data

[Three Cents Worth #285 Ski] Aspen Real Estate Has Had Many Peaks, But It’s Not Peaking

read more

May 21, 2015

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Douglas Elliman

,

Housing Trends & Cycles

,

Los Angeles

,

Statistics, Metrics & Data

[Three Cents Worth #283 LA] How Much Does It End Up Costing When a House Lingers on the Market in Los Angeles?

read more

January 30, 2015

Analysis & Research

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

New York City

,

Statistics, Metrics & Data

NYC Economy is Expanding Rapidly

read more

1

2

Next

Load More Posts

Page load link

Go to Top