Investors, real estate investors and consumers have all been scratching their heads lately. Everyone is looking at short-term inflation pressures and contradictions in data and wondering what affect that will have on the Fed’s next move.

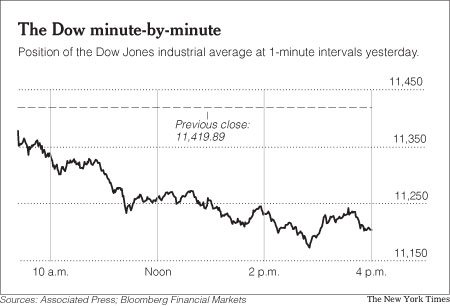

Yesterday, the stock markets dropped sharply [NYT] in response to new concerns about inflation as consumer prices increased. _[Wholesale inflation rose at a brisk pace in April [DFP]](http://www.freep.com/apps/pbcs.dll/article?AID=/20060517/BUSINESS07/605170351/1020/BUSINESS), pushed up by rising energy costs, as factory output rose and homebuilding slowed._

Just two days ago, a falling dollar and [weakening housing market suggested the Fed might pause and not raise rates at the next FOMC meeting [Bloomberg]](http://www.bloomberg.com/apps/news?pid=10000103&sid=amLBCKkir.6M&refer=us) causing _worries high commodity prices could slow the global economy._ [Oil prices have trended downward recently [Forbes]](http://www.forbes.com/markets/feeds/afx/2006/05/18/afx2755735.html). Core inflation was tame, posting a 0.1% increase in April and lower than expected and housing starts dropped 7.4% last month and down 20% since January.

_So which is it?_ Depending on the report you read, inflation is looming or it isn’t. The Fed will continue their policy of measured increases or they won’t.

The Fed has basically postioned itself to wait an see what the data tells them between now and the next FOMC meeting. So we get day to day changes in the interpretation of the state of inflation. The uncertainty of whether mortgage rates will continue to rise places further pressure on the housing market.

The [mixed economic reports [AR]](http://www.azcentral.com/arizonarepublic/business/articles/0517economy0517.html) should give the Fed a lot to think about.

The stock market seemed to show belief that inflation was not built into pricing yet. Even the zen-god of the bond market, Bill Gross of PIMCO [changed his forecast [Globe]](http://www.theglobeandmail.com/servlet/story/RTGAM.20060517.wbillgross0517/BNStory/Business/home).

>Bill Gross, the world’s most influential bond fund manager, raised his forecast for benchmark ten-year bond rates Wednesday, admitting he underestimated the strength of the global economy.

The takeaway from this economic stat chaos is that despite stronger consumer pricing, housing market participants are unsettled. It would seem to me that the impact of a weakening housing market has not impacted inflation data yet.

The economic repercussions of a weakening housing market is a significant economic unknown and additional rate increases will expose further weaknesses, compounding the problems. I remained concerned that inflation is more of a catalyst for a slowdown (in a weird twisted way) rather than a long term condition of an over heated economy.

Cart before the horse.

One Comment

Comments are closed.

I really don’t think housing or the weak dollar is playing a major role in the eyes of the fed, as they battle inflation red flags. Point is we are very near to the end of the rate hike campaign with a max of 50 basis points possible on future hikes.

Deep down I think inflation leading indicators such as the price of oil and precious metals are playing a much bigger role in the eyes of the fed and that this is the data they are looking at to see if it funnels down to Core CPI inflation, which it has over the past 12 months at 2.3% (comfort level is about 2% for the fed).

As long as energy prices and precious metal prices are high, how can the Fed Pause? The economy is strong which should keep housing from crashing, but the red flags are still there. Plus the fed funds futures spiked yesterday to about 61% in favor of a 1/4 point hike at June meeting after some fed governors had a Q & A with CNBC reporter Steve Liesman.

However, if oil prices correct to under $60/Barrel and precious metals correct as well before the June meeting I think the fed funds futures will lean more towards a pause as these inflation indicators are starting to get back to more ‘worry free’ levels.