I’ve been a AWOL for a few days so pardon the long post…I had a lot to get out of my system.

There was great anticipation for President Bush’s mortgage plan, which was unveiled at a press conference at 1:40 PM EST yesterday, which was largely fleshed out in the media already. Treasury Secretary Paulson has been able to arrange a deal with the mortgage industry to provide relief to some sub-prime homeowners. I was interviewed for this page 1 story but didn’t make the cut ;-(

> the industry would voluntarily help as many as 1.2 million homeowners who are heading for trouble paying their subprime mortgages but aren’t yet lost causes. In some cases, loan-servicing companies will agree to freeze mortgages at their low introductory rates. In others, credit counselors or loan servicers will walk mortgage holders through refinancing processes.

Treasury Secretary Henry M. Paulson Jr. said

>“The approach announced today is not a silver bullet,” said Treasury Secretary Henry M. Paulson Jr., who hammered out the agreement. “We face a difficult problem for which there is no perfect solution.”

The 1.2M number that will be quoted repeatedly today is likely overstated 5x indicating this proposal will help a limited group of people, let along address the credit problem. I am also worried about litigation by investors since they are not getting the returns they thought they were paying for. In other words, the pricing didn’t reflect the risk. But then again, this may end up affecting very few borrowers relative to the 1.2M suggested.

>One of the financial industry’s lead negotiators estimated that at most 20 percent of subprime borrowers whose payments will increase sharply over the next 18 months — 360,000 out of 1.8 million people — would qualify for rapid consideration of a special five-year freeze on interest rates.

Does this send the right message to mortgage investors that are already on the sidelines because they are jittery about what’s in the mortgage pools? This action seems to open a whole new area of concern. An investor buys a package of loans and forecasts how much the rate will rise in a certain period of time. Thats the basis of the price paid. What if the interest rate you thought you were going to get from your investment was frozen at a much lower rate. As an investor, would you buy more paper until you felt comfortable that this sort of thing wouldn’t happen again?

Limited availability of mortgages =

higher mortgage rates =

higher default rates =

more personal hardship

Here’s a contrarian viewpoint on the Bush plan called “The Mother of all Bad Ideas.”

>Although there are mountains of uncertainty as to how the plan will be structured and implemented, there is no question that as lenders factor in the added risk of having their contracts re-written or of being held liable for defaulting borrowers, lending standards for new loans will become increasingly severe (higher down payments, mortgage rates, and required Fico scores, lower loan to income ratios, and perhaps the death of adjustable rate loans altogether). The result will be additional downward pressure on home prices, despite the fact that in the short term fewer homes will be sold in foreclosure than what might have been without the rescue plan.

The FDIC chair’s statement on the loan modification plan, basically said that they haven’t had time to read it but thinks its probably good. Suggestion: delay comment until you’ve read it.

As I have said many times, I continue to be amazed at the disconnect between the impact of the housing market on the economy.

According to the Mortgage Bankers Association, the total number of loans that are delinquent (5.59%), in foreclosure (1.69%), or going into foreclosure (0.78%) are the highest since 1986.

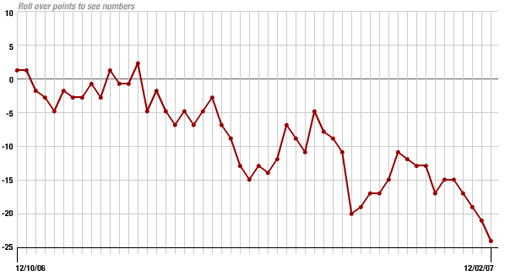

In other words, consumers are uncomfortable.

Washington Post-ABC News Consumer Comfort Index Survey

This is a humanistic gesture by President Bush and a monumental effort by Treasury Secretary Paulson that only few people on the planet could have made happen. This action will make many feel good and give the impression that the problem will go away or is being resolved. However, by neglecting to address the larger issue of subprime mortgages popping up in nearly every type of mortgage pool, effectively scarring away investment, the credit situation will continue to erode and life will be more difficult for millions of homeowners with a gun to their head.

Odds & Ends

We should all remember that foreclosures also hurt their neighbors.

Why Paulson Needn’t Worry About Litigation Risk in His Mortgage Plan

UPDATE

Here’s the Bush Administration Plan as a flowchart.

5 Comments

Comments are closed.

If I were a mortgage backed security investor I think I’d be ticked by these actions. You make a somewhat risky investment that won’t actually yield returns until the payment goes up, and then it doesn’t go up because the governement stops it?

In reality, I don’t think it will effect many people.

[…] No Silver Bullet: Lending Lip Service To Mortgage Service I’ve been a AWOL for a few days so pardon the long post…I had a lot to get out of my system. There was great anticipation for President Bush’s mortgage plan, which was unveiled at a press conference at 1:40 PM EST yesterday, which was largely fleshed out in the media already. Treas… […]

[…] No Silver Bullet: Lending Lip Service To Mortgage Service I’ve been a AWOL for a few days so pardon the long post…I had a lot to get out of my system. There was great anticipation for President Bush’s mortgage plan, which was unveiled at a press conference at 1:40 PM EST yesterday, which was largely fleshed out in the media already. Treas… […]

Bountiful – I originally thought the same way at first. But after a short while, I realized that this probably is better for holders of RMBS. These holders do NOT want foreclosures. Any plan that will help, even a little, is better for these guys because it may bring a bit more liquidity into the secondary mortgage market, that is still seized up.

Confidence & liquidity are the problems here. No one wants paper that will be worthless, and no bids are coming in even at these distressed levels. So, any plan, even if the plan wont work but will instill some confidence that actions are being taken by govt and private sector, may limit the losses for these investors.

thoughts?

While I agree with your basic premise Noah, its such a small solution to a huge problem. All this does it provide a little relief, when in fact it does not send the message to the secondary market investors. They don’t feel comfortable with the content of the mortgage pools hence they are not buying. Yes foreclosures are a bad and costly thing, but this approach only helps temper the damage and the issue continues to get worse than better.