Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Articles

September 28, 2012

Adventures in Media & Marketing

,

Appraising

,

Celebrity, Pop Culture

,

Manhattan

,

Media

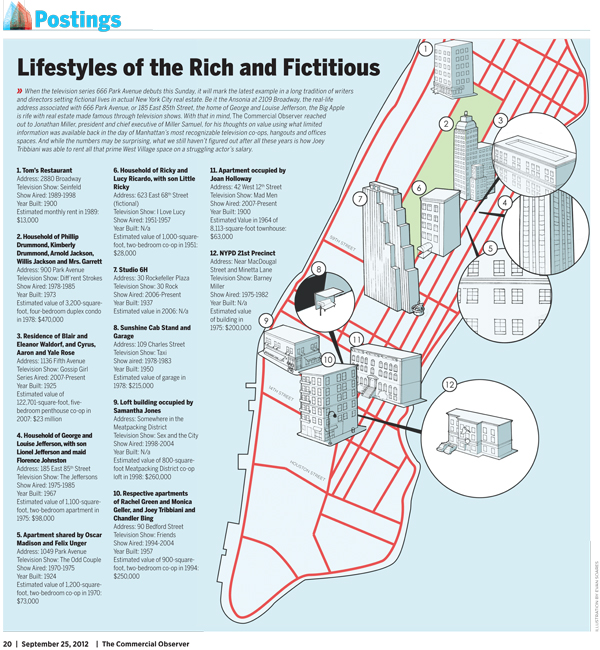

[666 Park Avenue] Appraising Fictitious TV Celebrity Apartments

read more

September 13, 2012

Blogging Off The Matrix

,

Curbed

,

Historical, Landmark, Milestone

,

Washington DC

[Three Cents Worth DC #208] Keep Your Eye On The Numbers (For The Past Decade)

read more

August 29, 2012

Blogging Off The Matrix

,

Curbed

,

Washington DC

[Three Cents Worth DC #205] Does The History of The DMV’s New Listings Predict The Next Housing Slogan?

read more

June 11, 2012

Blogging Off The Matrix

,

Curbed

,

Washington DC

[Three Cents Worth DC #194] DC’s Housing Market Turns The Tide; Good News For Sellers

read more

February 7, 2012

Douglas Elliman

,

Federal Reserve, New York

,

Historical, Landmark, Milestone

,

Manhattan

,

New York Times

Change is Constant: 100 Years of New York Real Estate

read more

January 29, 2010

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

New York Times

,

RealtyTrac

Appraisers and Foreclosure Sales Bring Havoc to Housing Markets

read more

September 26, 2009

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Media

,

New York Times

[NY Times Real Estate Cover Story] New York Appraisals Get Shortchanged

read more

December 18, 2006

Luxury, Super, Ultra, Mega

,

Manhattan

,

Media

[Haute Living Magazine] Buy The Numbers Column: December 2006

read more

October 23, 2006

Adventures in Media & Marketing

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Media

,

South Florida

[Haute Living Magazine] Buy The Numbers Column: October 2006

read more

July 5, 2006

Amenities, Adjustments & Value Logic

,

Luxury, Super, Ultra, Mega

,

Migration, Psychology, Demographics

Penthouse Article In New York Living

read more

March 30, 2006

Migration, Psychology, Demographics

Super-Sized Does Not Equal Family-Sized

read more

Previous

1

2

Load More Posts

Page load link

Go to Top