Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Charts

April 1, 2023

Luxury, Super, Ultra, Mega

,

New York City

,

Wall Street, Financial Services

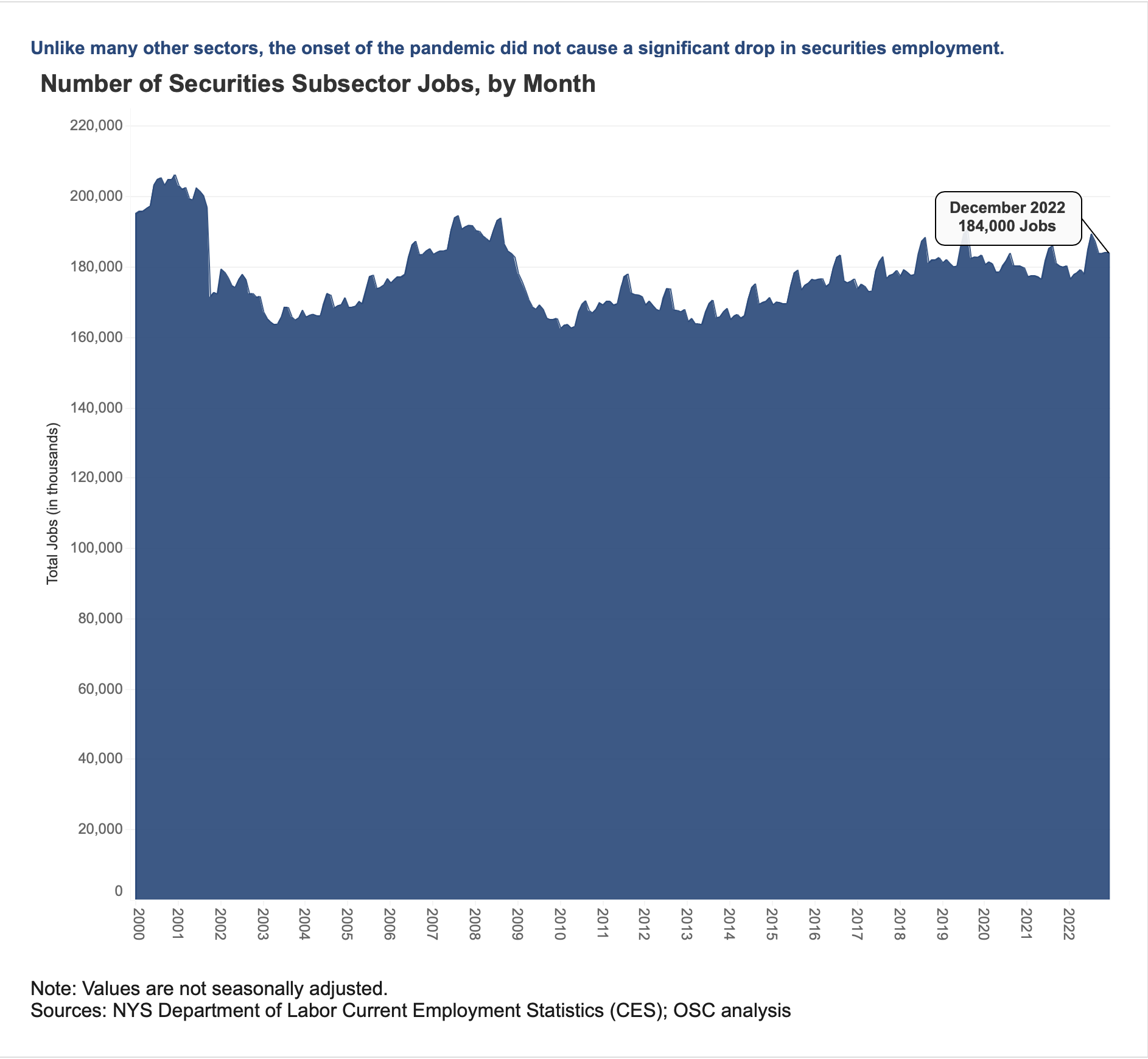

Wall Street Bonuses Fall To Pre-Pandemic Levels

read more

April 14, 2022

Douglas Elliman

,

Elliman Reports

,

Housing Trends & Cycles

,

Statistics, Metrics & Data

Elliman Magazine Column – A Symptom of Chronic Inventory Lows: Bidding Wars Are Everywhere

read more

December 2, 2021

Aspen

,

Douglas Elliman

,

Greenwich

,

Hamptons/North Fork

,

Los Angeles

,

Manhattan

,

Miami (Beach + Mainland)

,

Palm Beach

Listing Inventory Trends In The Time Of COVID

read more

December 28, 2020

Bloomberg News

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Greenwich

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

New York Times

,

Rentals, Investing

,

Sales

,

Westchester County, NY

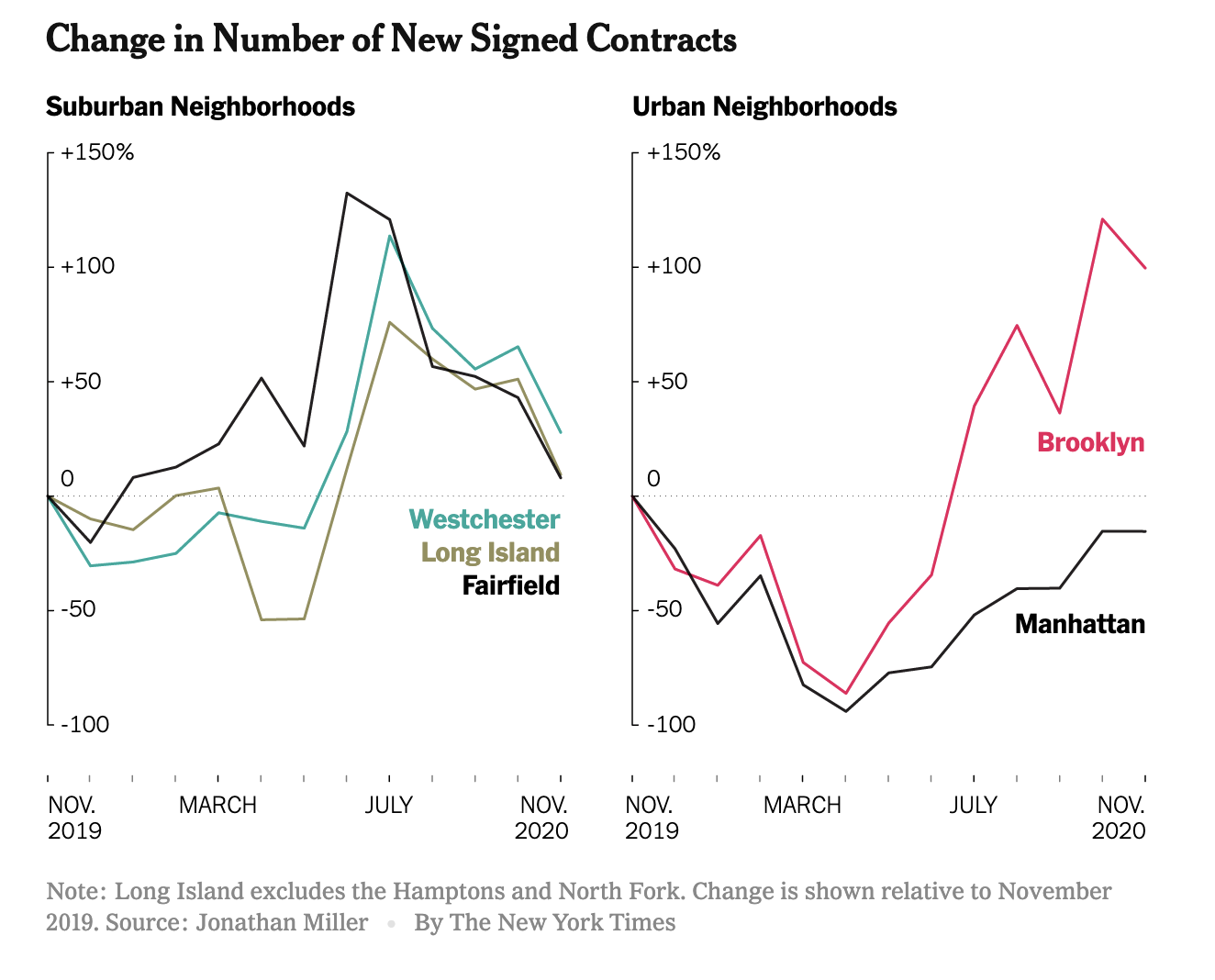

Peak Suburb Has Passed

read more

November 21, 2020

Brooklyn

,

Elliman Reports

,

Housing Trends & Cycles

,

Manhattan

,

New York Times

,

Queens

,

Rentals, Investing

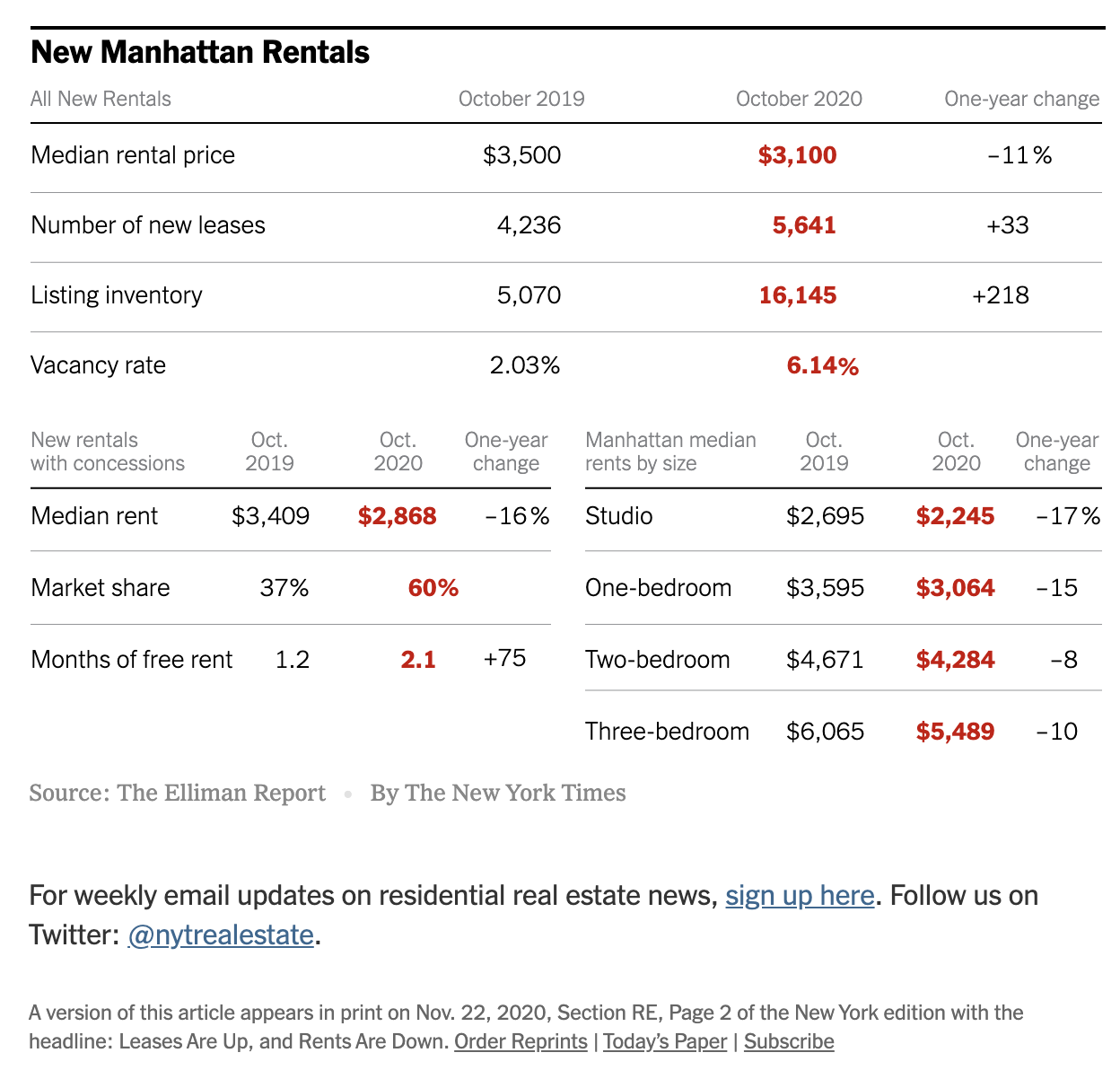

NYT Real Estate: Signs of a Manhattan Rental Market Recovery

read more

August 19, 2020

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Elliman Reports

,

Housing Note

,

Housing Trends & Cycles

,

Manhattan

,

New York Times

,

Westchester County, NY

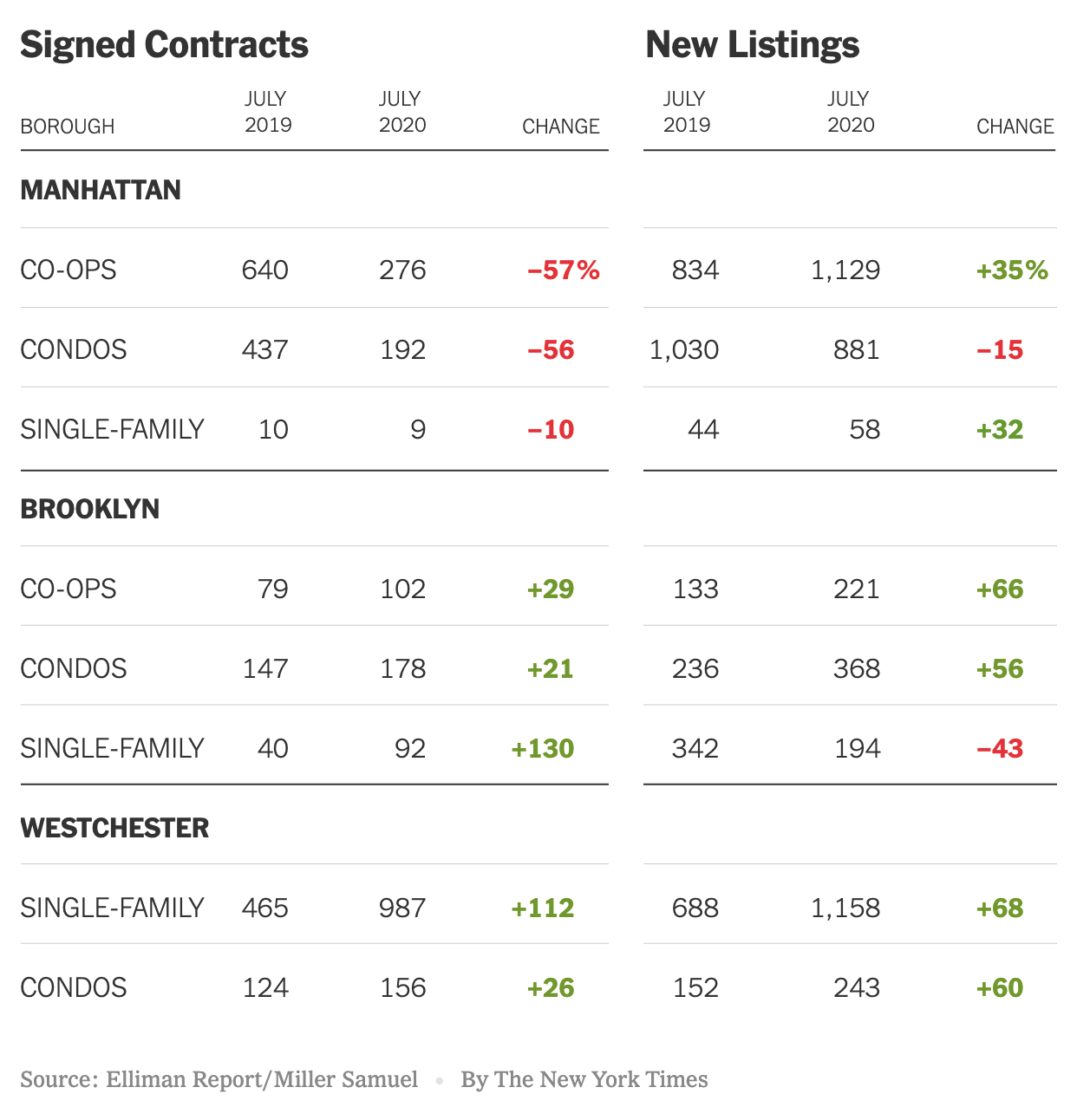

The ‘Urban To Suburban’ Narrative Is Really ‘Manhattan To Suburban’

read more

February 5, 2020

Charts, Maps, Images, Infographics, Video

,

Government, Politics, Regulations & Policy

,

Manhattan

,

The Real Deal

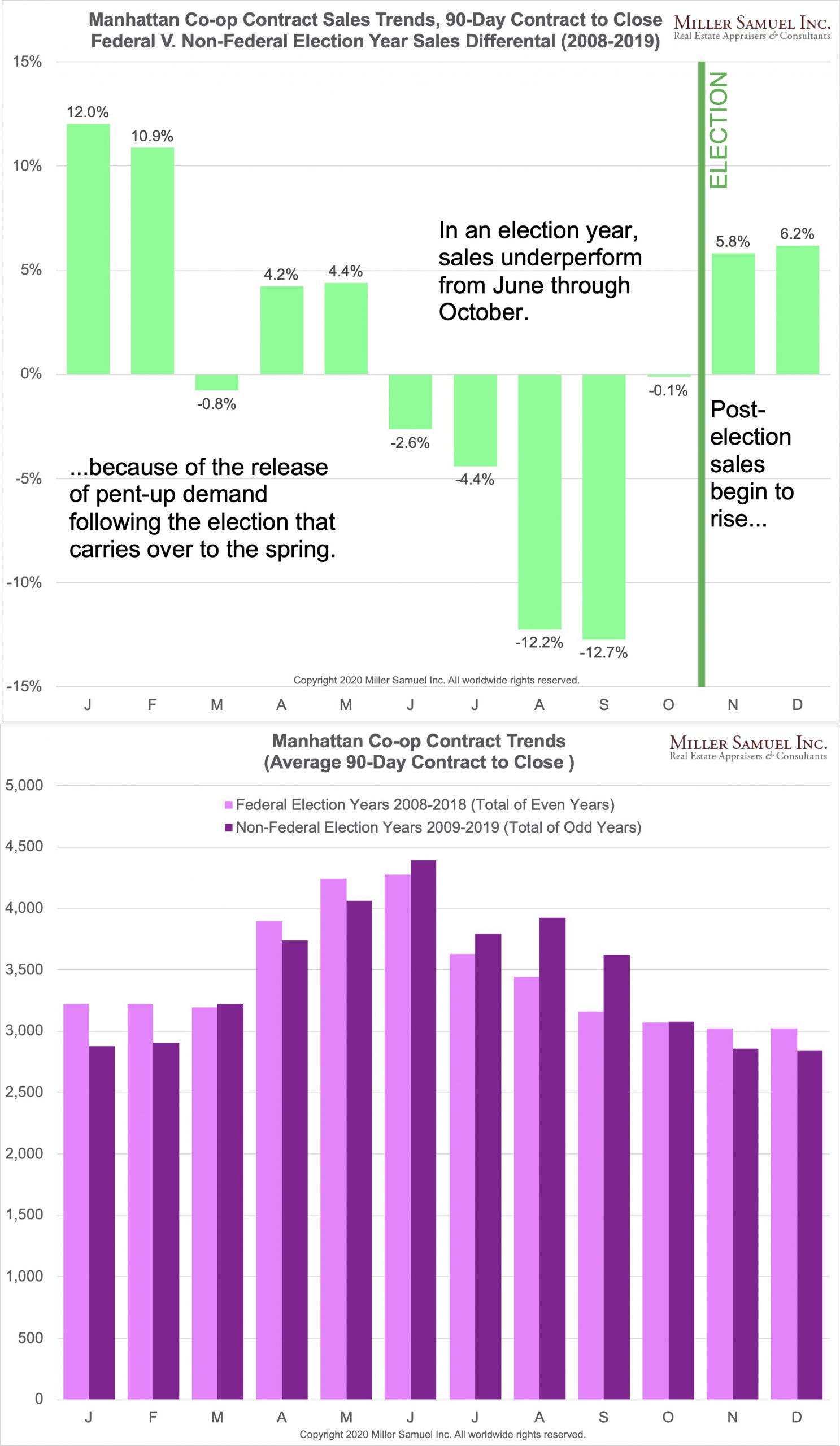

Manhattan Co-op Sales Fall During Federal Election Year

read more

February 7, 2019

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

January 2019 YOY% Change in Manhattan Co-op/Condo Listing Inventory

read more

December 14, 2018

Aspen

,

Boca Raton

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Greenwich

,

Manhattan

,

Statistics, Metrics & Data

Elliman Magazine Winter 2019 – Market Update

read more

December 13, 2018

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

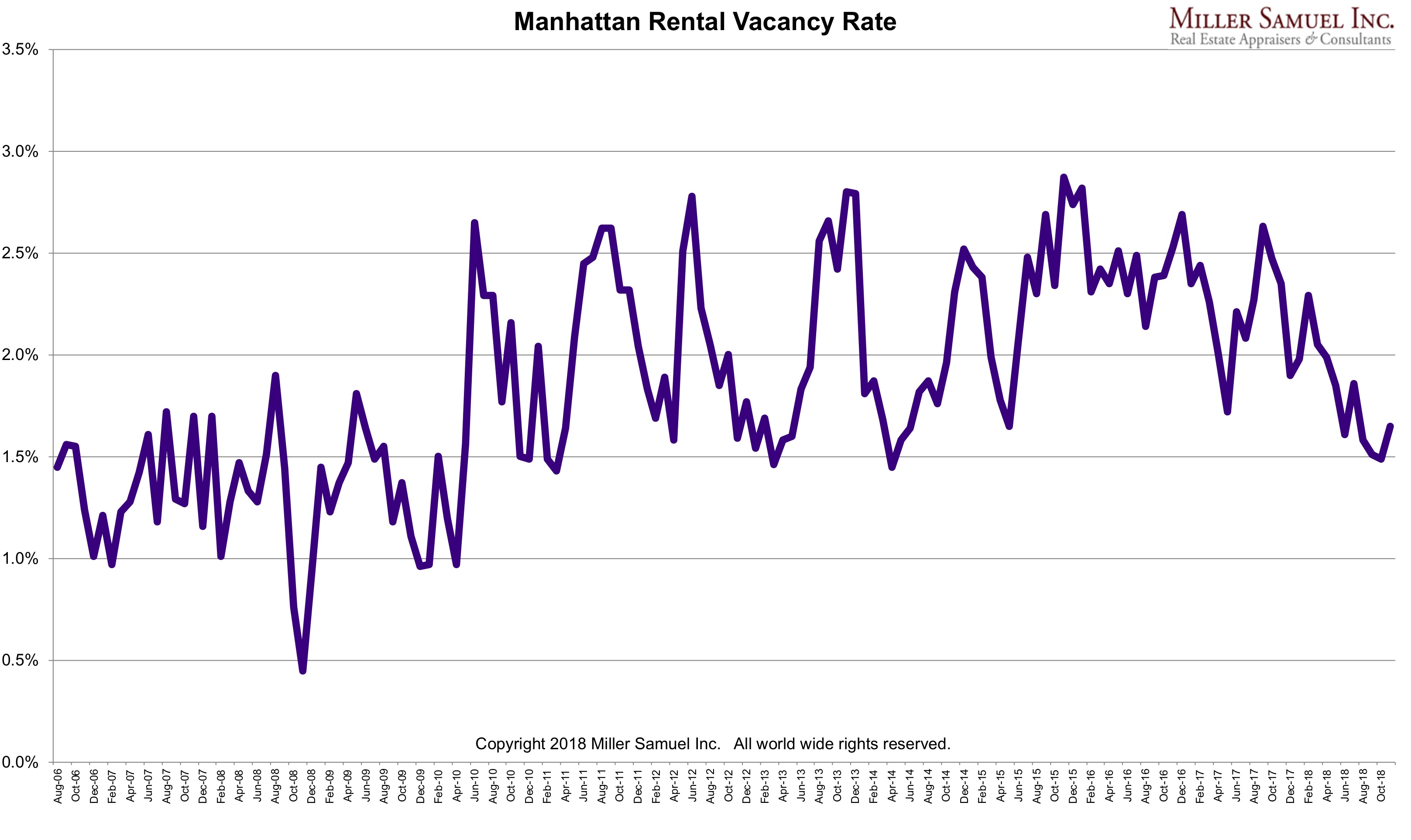

Manhattan Residential Vacancy Rate Isn’t Seasonal?

read more

January 3, 2018

Development, Construction, Architecture & Land

,

Manhattan

New Manhattan Condos Got Really Big Over The Past Three Years

read more

January 1, 2018

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

New York Times

2017: The Year The 2015 Manhattan Market Shift Became Conventional Wisdom

read more

1

2

Next

Load More Posts

Page load link

Go to Top