Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Explainer

January 23, 2024

Affordability, Affordable Housing

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Homebuying Process

,

Housing Trends & Cycles

Central Bank Central Video Podcast: Miller Samuels’ Chief Sees Stubbornly High Mortgage Rates, Low Inventories

read more

October 3, 2023

Analysis & Research

,

Explainer

,

Manhattan

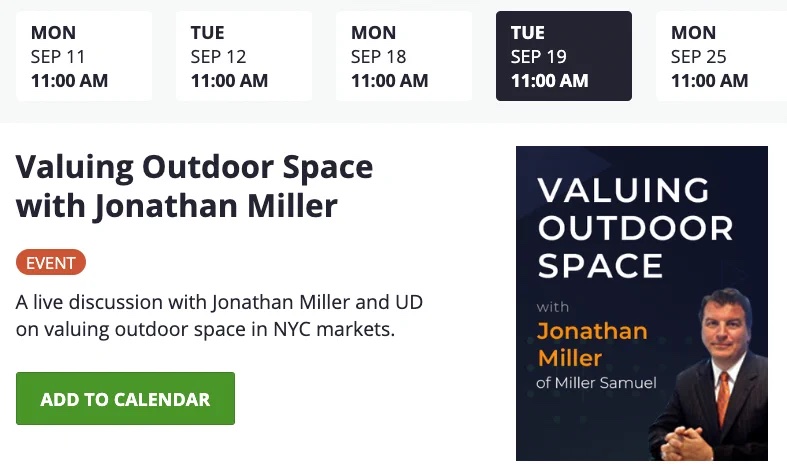

Urban Digs Webinar: Valuing Outdoor Space

read more

July 18, 2023

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Housing Trends & Cycles

,

Language, Jargon & Quotes

,

Social, Tech, Gadgets, Software

[Business of Home Podcast] A Real Estate Check-In With Jonathan Miller

read more

April 1, 2023

Luxury, Super, Ultra, Mega

,

New York City

,

Wall Street, Financial Services

Wall Street Bonuses Fall To Pre-Pandemic Levels

read more

November 13, 2022

Affordability, Affordable Housing

,

New York City

,

New York City Suburbs

,

NY1

My Interview on Crosstown with Pat Kiernan – What can we do about NYC’s housing crisis?

read more

November 7, 2021

Appraising

,

Boom Bubble Bust

,

Explainer

,

Homebuying Process

This Just In: The ‘A’ in ‘Zillow’ Stands for ‘Accuracy’

read more

July 19, 2021

Appraising

,

Law, Ethics & Fraud

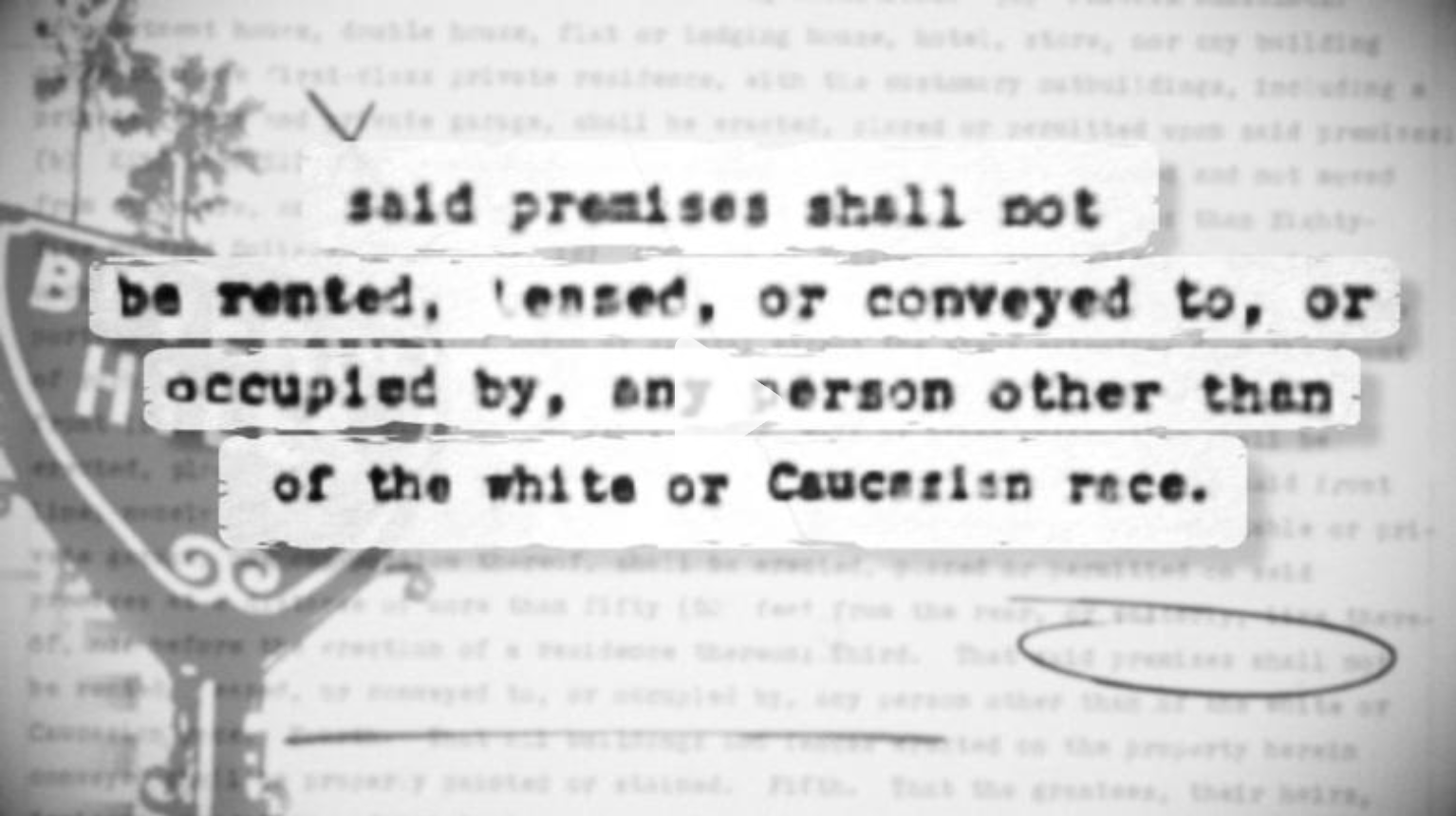

MORE AMORIN INFLUENCE (MAI): The AI National Nominating Committee Design Is Being Attacked By FOJs

read more

May 18, 2021

Appraising

,

Continuing Education & Licensing

No Diversity: 96.5% Of U.S. Appraisers Are White

read more

February 24, 2021

Appraising

,

Explainer

,

Law, Ethics & Fraud

Epic Fail: The Appraisal Institute IRS 990s Show They Need To Do A 180

read more

December 28, 2020

Bloomberg News

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Greenwich

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

New York Times

,

Rentals, Investing

,

Sales

,

Westchester County, NY

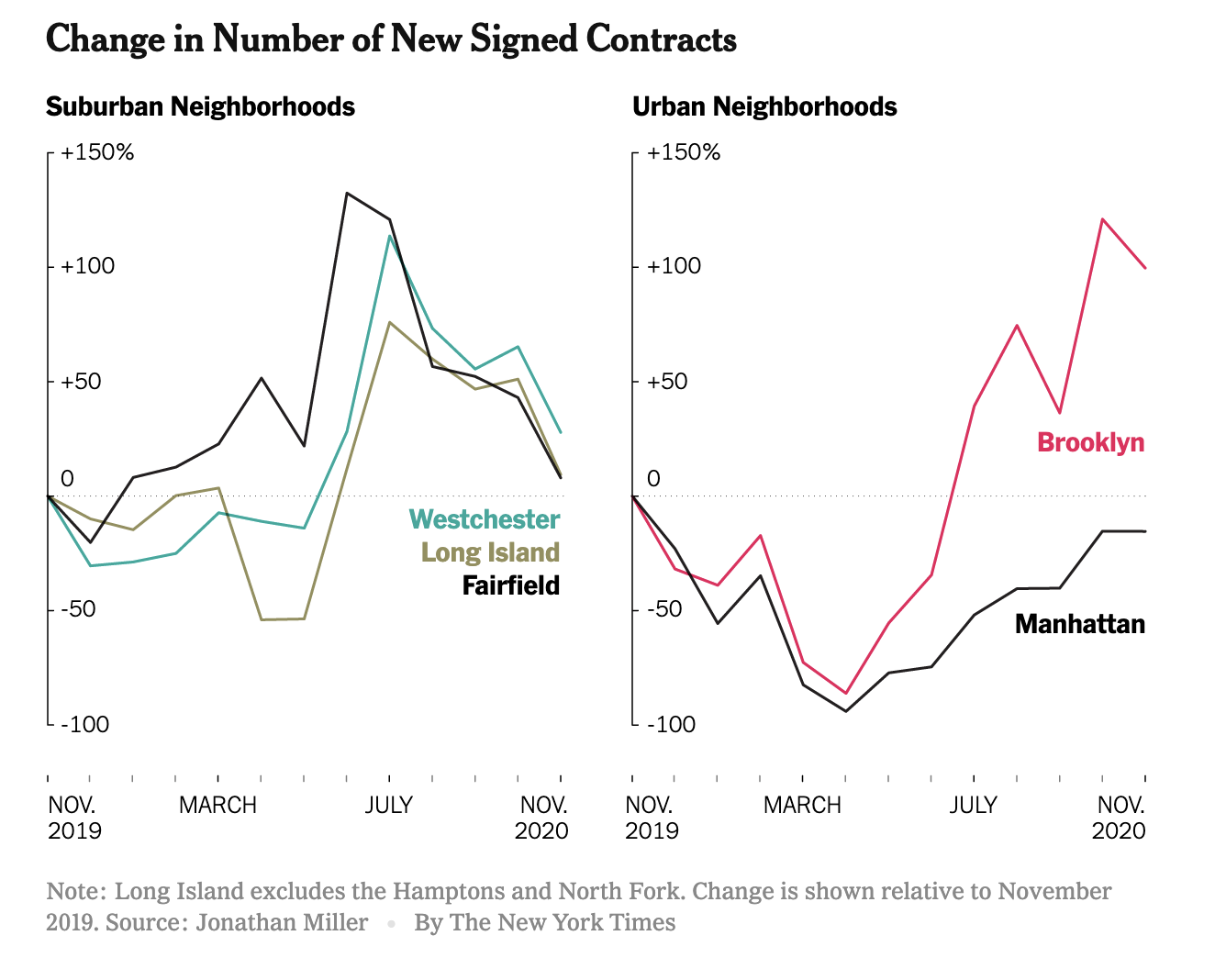

Peak Suburb Has Passed

read more

December 28, 2020

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

The Real Deal

,

Westchester County, NY

TRD Quick Question: Jonathan Miller “What’s Happening in the NYC Real Estate Market?”

read more

July 25, 2020

Appraising

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

The Previous Victim Of The Appraisal Institute Sham Election Maneuver Shares What Happened

read more

1

2

Next

Load More Posts

Page load link

Go to Top