Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Investigative

January 6, 2021

Appraising

,

Law, Ethics & Fraud

Appraisal Institute Board of Directors Tried To Sneak Sham Bylaw Changes Past Membership

read more

August 19, 2020

Appraising

,

Government, Politics, Regulations & Policy

,

Housing Note

,

Law, Ethics & Fraud

With All That PPP And Without All That Travel, The Appraisal Foundation Doesn’t Need A Grant From ASC This Year

read more

August 8, 2020

Appraising

,

Law, Ethics & Fraud

Quid Pro Quo: The Right Candidate Got Elected And Corrupt Leadership Got To Keep Their Sham Election Maneuver

read more

July 25, 2020

Appraising

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

The Previous Victim Of The Appraisal Institute Sham Election Maneuver Shares What Happened

read more

July 13, 2020

Appraising

,

Boards & Associations

,

Law, Ethics & Fraud

The Appraisal Institute Has Missed The Opportunity To Come Clean With Its Members

read more

March 18, 2020

Appraising

,

Explainer

,

Government, Politics, Regulations & Policy

Some Financial Institutions Care About The Safety Of Appraisers, While Most Do Not

read more

February 5, 2020

Charts, Maps, Images, Infographics, Video

,

Government, Politics, Regulations & Policy

,

Manhattan

,

The Real Deal

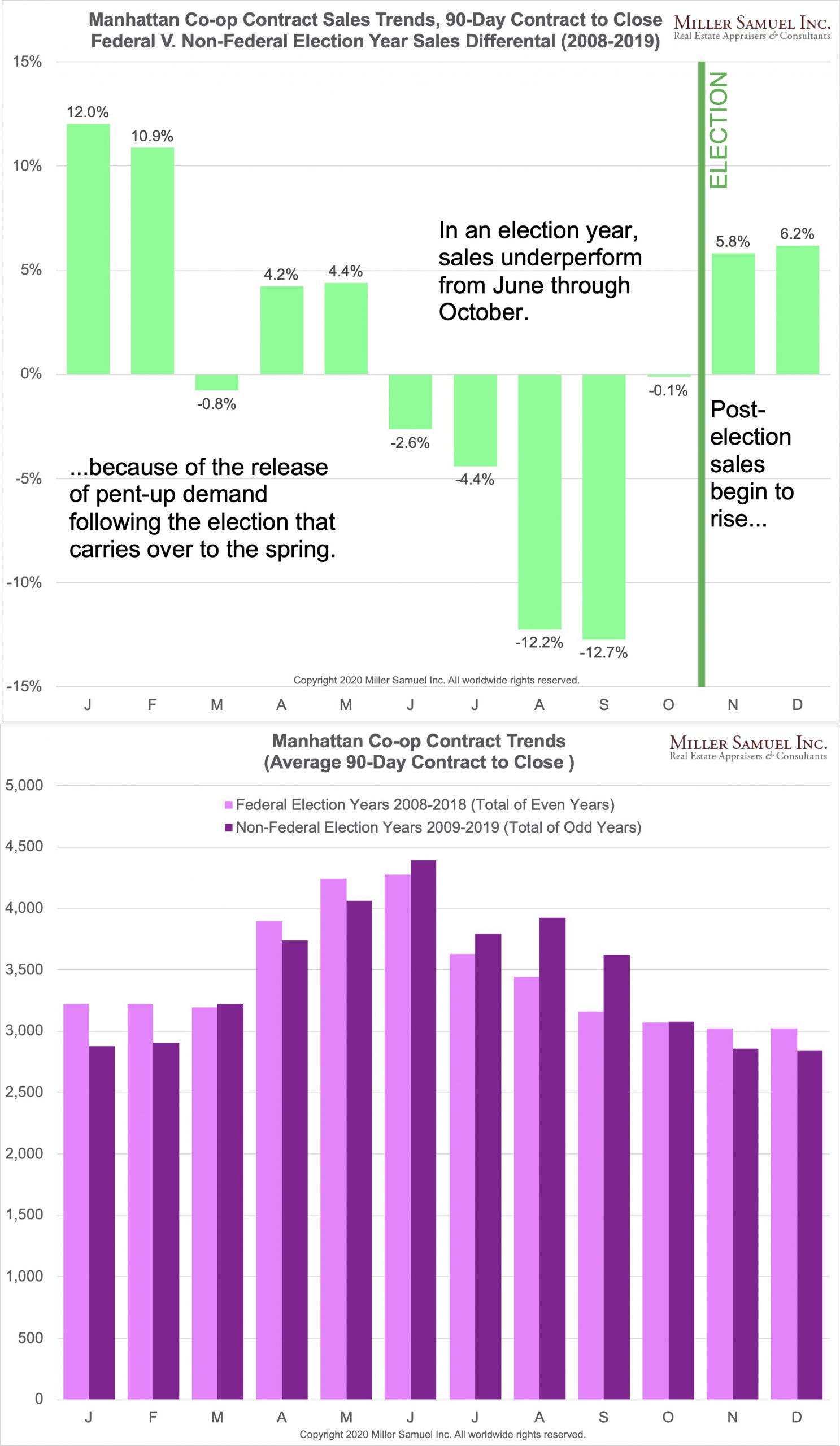

Manhattan Co-op Sales Fall During Federal Election Year

read more

March 19, 2019

Affordability, Affordable Housing

,

Brooklyn

,

Government, Politics, Regulations & Policy

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York City

,

Queens

,

Taxes, Insurance, Fees

The Proposed NYC “Pied-A-Terre Tax” Looks Catastrophic to NYC Real Estate

read more

November 30, 2018

Appraising

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

Remember liar loans of a decade ago? Those same people want to do away with appraisers.

read more

December 27, 2017

Bloomberg TV

,

Explainer

,

Media

,

Taxes, Insurance, Fees

Bloomberg TV – Housing Related Issues in Final Version of the Tax Cut and Jobs Act of 2017

read more

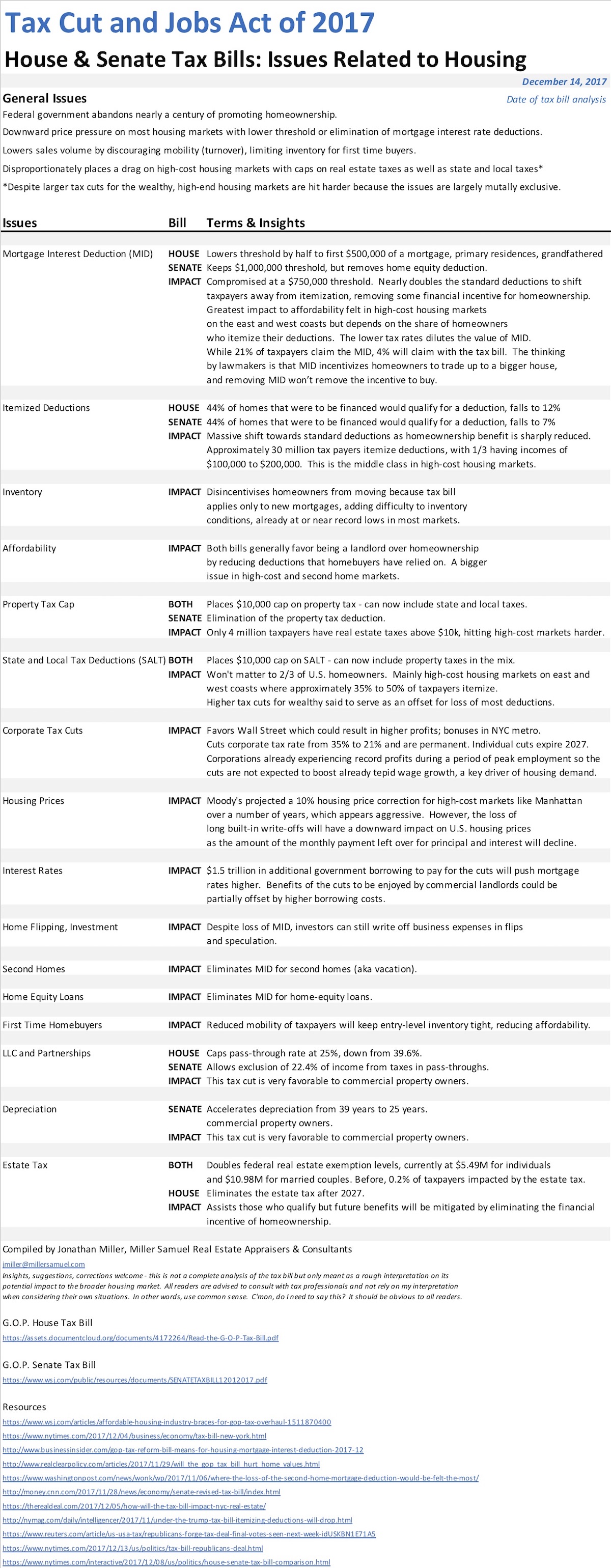

December 14, 2017

Explainer

How the GOP Tax Bill Might Impact U.S. Residential Real Estate

read more

August 24, 2017

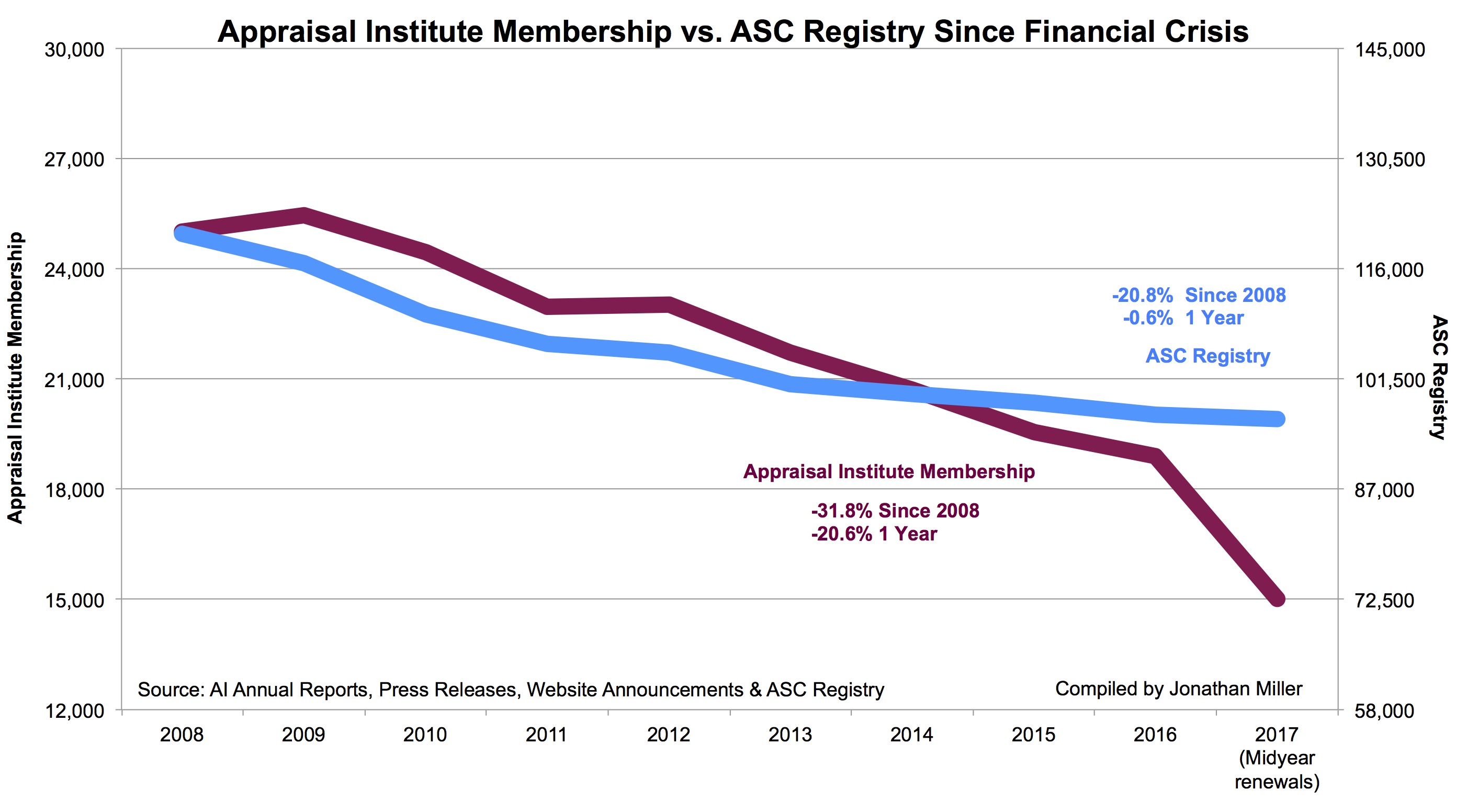

Appraising

Appraisal Institute Membership Falls Sharply As ASC Registry Levels Off

read more

1

2

Next

Load More Posts

Page load link

Go to Top