Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Reports

January 25, 2013

Douglas Elliman

,

Elliman Reports

,

Hamptons/North Fork

[Tax Planning on Steroids] 4Q 2012 + 2003-2012 Hamptons/North Fork Decade Reports

read more

January 25, 2013

Douglas Elliman

,

Elliman Reports

,

IRS

,

Long Island

[Turning Corner?] 4Q 2012 + 2003-2012 Long Island Decade Reports

read more

January 21, 2013

Douglas Elliman

,

Elliman Reports

,

Palm Beach

,

South Florida

[Tightening] 4Q 2012 Palm Beach Report

read more

January 21, 2013

Douglas Elliman

,

Elliman Reports

,

Fort Lauderdale

,

South Florida

[Looking Up] 4Q 2012 Fort Lauderdale Report

read more

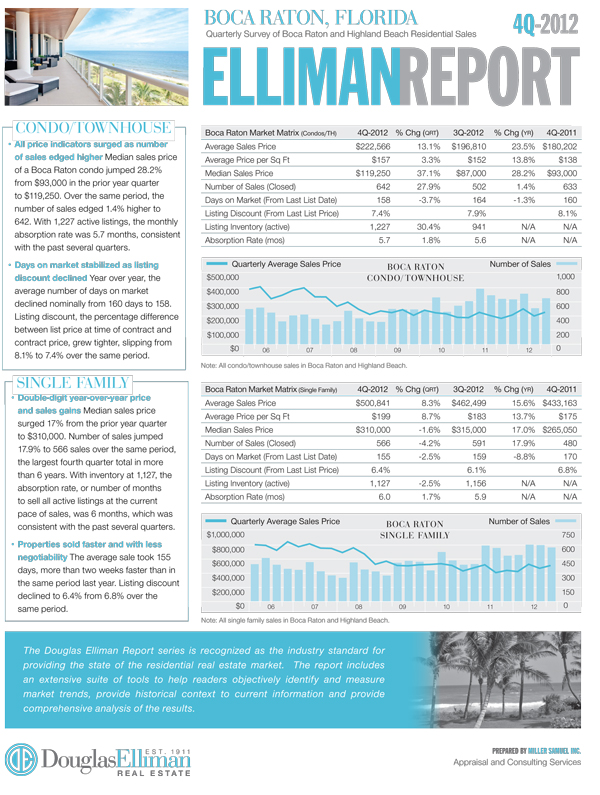

January 21, 2013

Boca Raton

,

Douglas Elliman

,

Elliman Reports

,

South Florida

[Rising, Faster] 4Q 2012 Boca Raton Report

read more

January 21, 2013

Douglas Elliman

,

Elliman Reports

,

New York Times

,

Queens

[7-Year List Low] 4Q 2012 Queens Report

read more

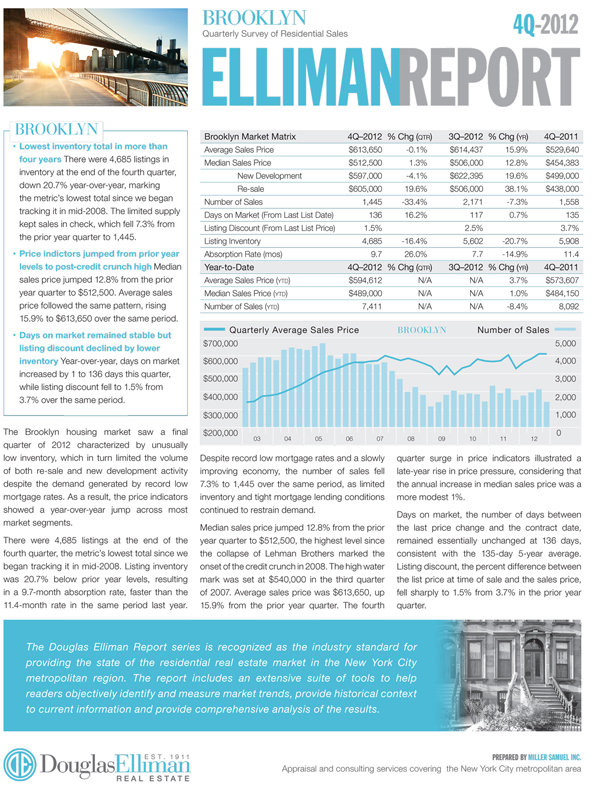

January 21, 2013

Brooklyn

,

Credit, Finance, Mortgage, Rates

,

Douglas Elliman

,

Elliman Reports

[Tempering Sales] 4Q 2012 Brooklyn Report

read more

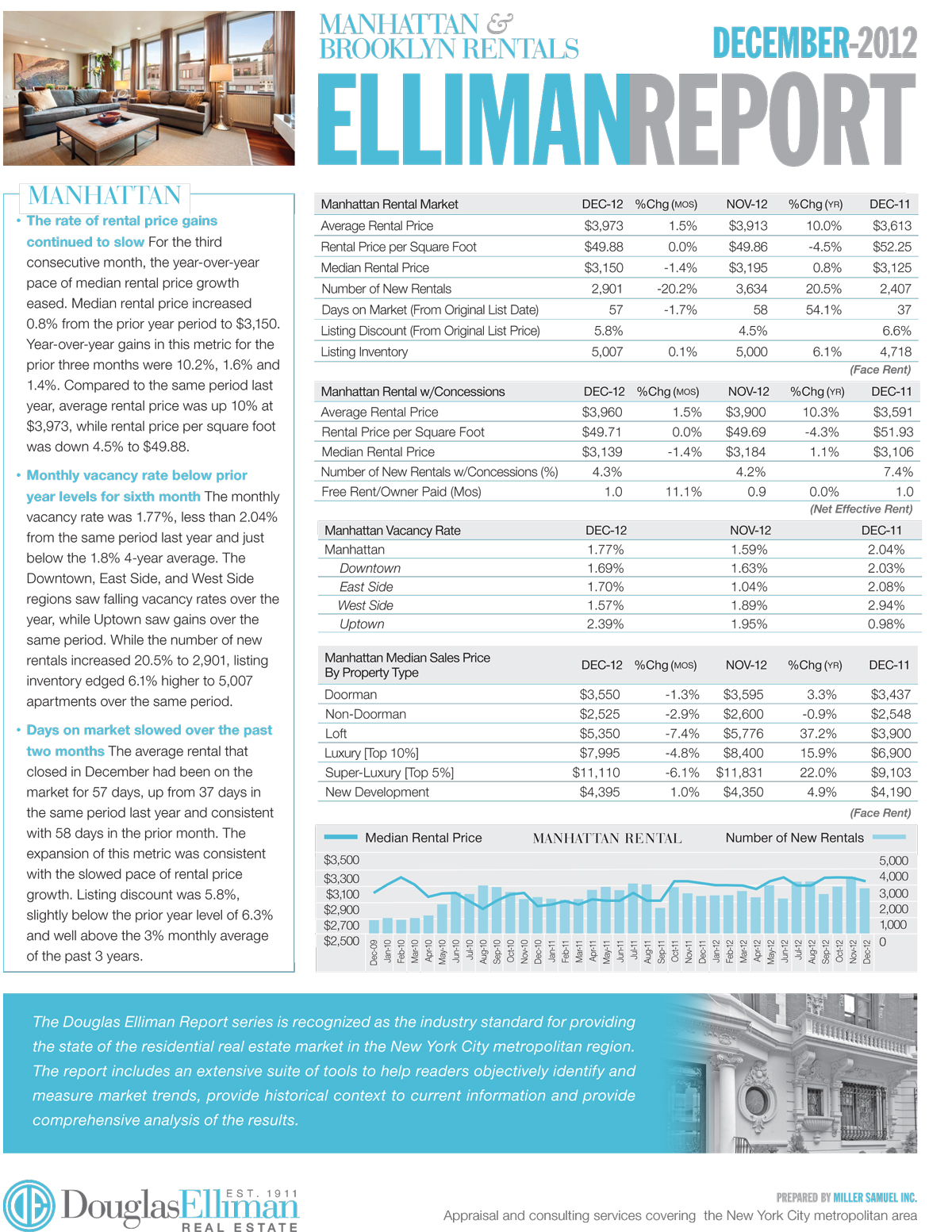

January 21, 2013

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Manhattan

,

Rentals, Investing

[Cool Your Jets] 12-2012 Manhattan/Brooklyn Rental Report

read more

January 12, 2013

Douglas Elliman

,

Elliman Reports

,

Putnam County

,

Westchester County, NY

[Stronger Finish] 4Q 2012 Westchester & Putnam Report

read more

January 12, 2013

Douglas Elliman

,

Elliman Reports

,

Miami (Beach + Mainland)

,

South Florida

[International Story] 4Q 2012 Miami Sales Report

read more

January 3, 2013

Douglas Elliman

,

Elliman Reports

,

Manhattan

[In Lieu of Paying More Taxes] 4Q 2012 Manhattan Sales Report

read more

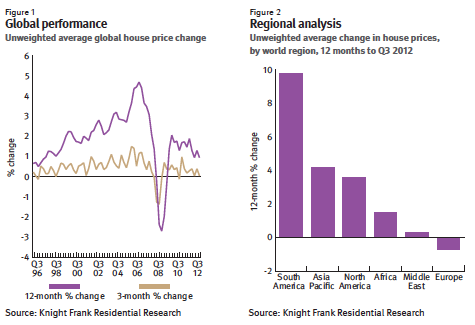

December 13, 2012

Housing Indices & Portals

,

International

,

Knight Frank

,

Market Reports

[Knight Frank] Global Reports That Look Forward and Backward : Europe As Denominator

read more

Previous

4

5

6

Next

Load More Posts

Page load link

Go to Top