Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Absorption

October 2, 2012

Douglas Elliman

,

Elliman Reports

,

Federal Reserve, New York

,

International

,

Manhattan

[Devoid of Sellers] 3Q 2012 Manhattan Sales Report

read more

September 24, 2012

Analysis & Research

,

Manhattan

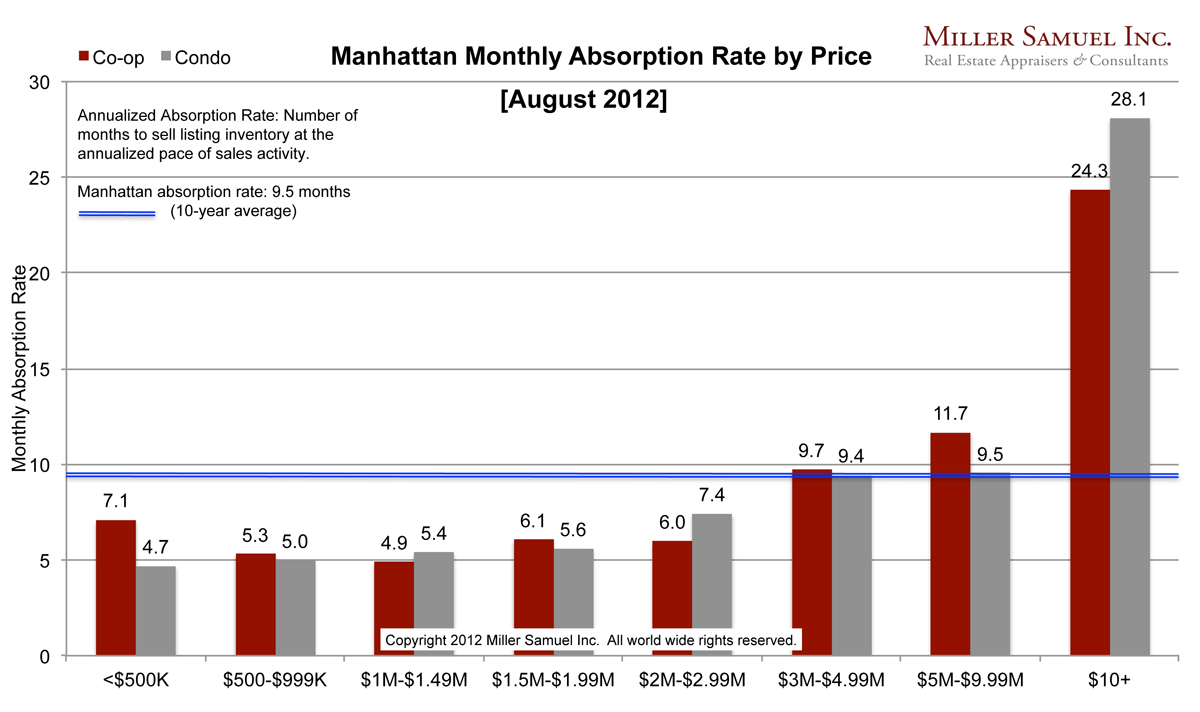

[Manhattan Absorption] August 2012 – It’s A Lot Faster On The Down Low

read more

September 19, 2012

Blogging Off The Matrix

,

Curbed

,

Douglas Elliman

,

Manhattan

[Three Cents Worth NY #210] Manhattan Housing Talks Like a Pirate

read more

September 6, 2012

Analysis & Research

,

Manhattan

[Rotate!] Manhattan Housing Market Absorption by Price (3/09 to 8/12)

read more

July 31, 2012

Douglas Elliman

,

Elliman Reports

,

Fort Lauderdale

,

South Florida

[Full Frontal Waterfront] 2Q 2012 Fort Lauderdale Report

read more

July 27, 2012

Douglas Elliman

,

Elliman Reports

,

Hamptons/North Fork

[More Sales] 2Q 2012 Hamptons & North Fork Report

read more

July 19, 2012

Brooklyn

,

Credit, Finance, Mortgage, Rates

,

Douglas Elliman

,

Elliman Reports

[Stableborough] 2Q 2012 Brooklyn Report

read more

July 16, 2012

Analysis & Research

,

Manhattan

[Manhattan Absorption] June 2012, Moving Faster, Strength Expanding

read more

July 12, 2012

Douglas Elliman

,

Elliman Reports

,

Westchester County, NY

[Stable Burb] 2Q 2012 Westchester & Putnam Report

read more

June 18, 2012

Analysis & Research

,

Manhattan

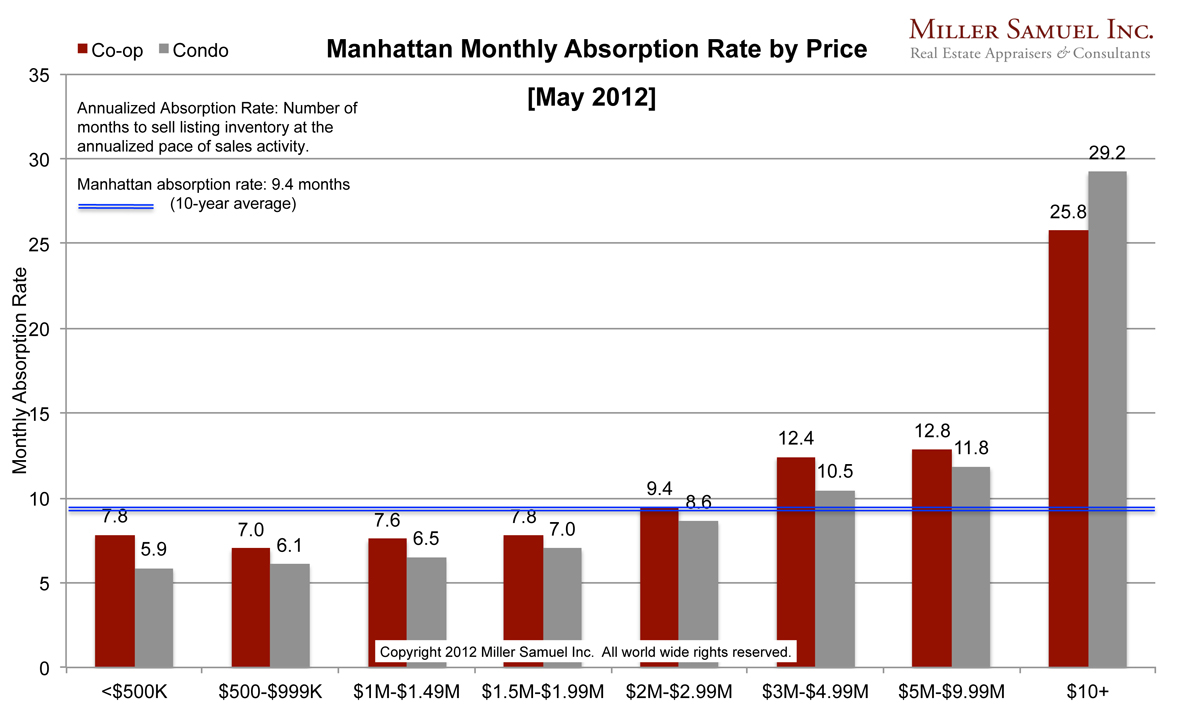

[Manhattan Absorption] May 2012, Faster Pace Than Last Year

read more

May 29, 2012

Blogging Off The Matrix

,

Curbed

,

Manhattan

[Three Cents Worth NY #191] Manhattan Rentals Are Quicker Picker Upper

read more

May 22, 2012

Bloomberg News

,

Brokers, Agents, MLS, NAR

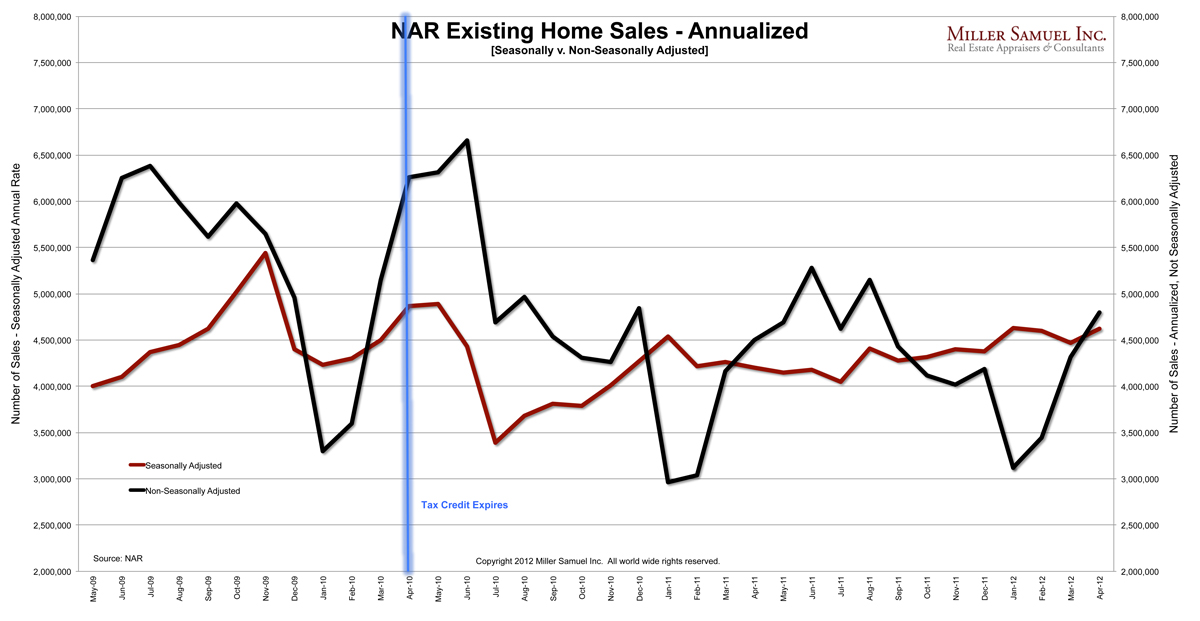

[NAR] Existing Home Sales Continue to Edge Higher +10% Y-O-Y

read more

Previous

3

4

5

Next

Load More Posts

Page load link

Go to Top