Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› FNC

November 27, 2012

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

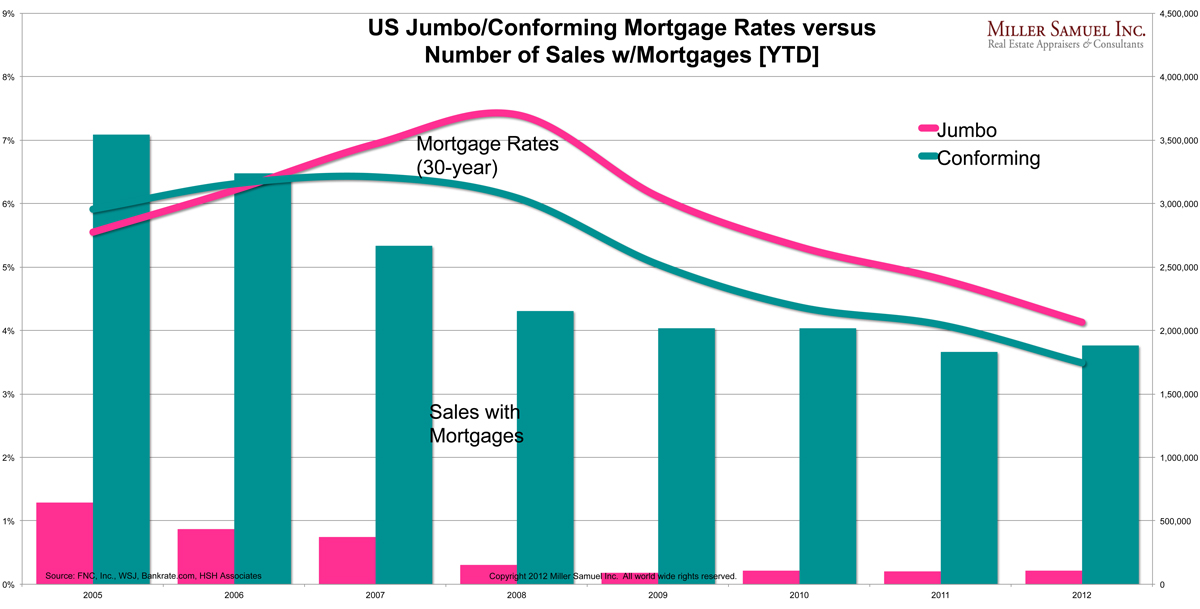

Get Down With It: Falling Mortgage Rates Are Not Creating Housing Sales

read more

November 26, 2012

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

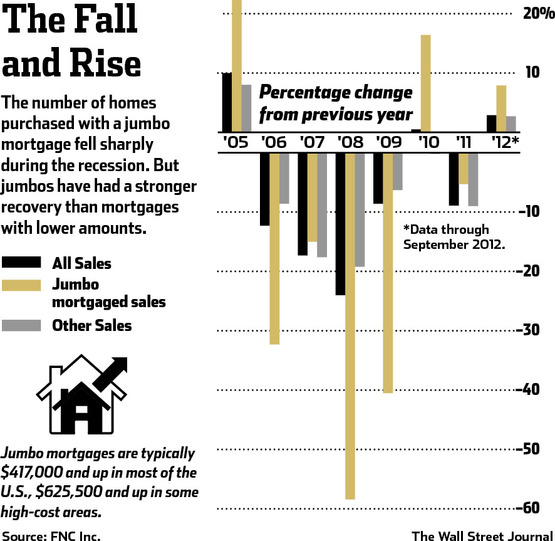

Jumbos Fell Harder, Now Rising Faster, But Off Low Base

read more

June 9, 2012

Elliman Reports

,

Housing Indices & Portals

,

Trulia

,

Wall Street Journal

,

Weather & Natural Disasters

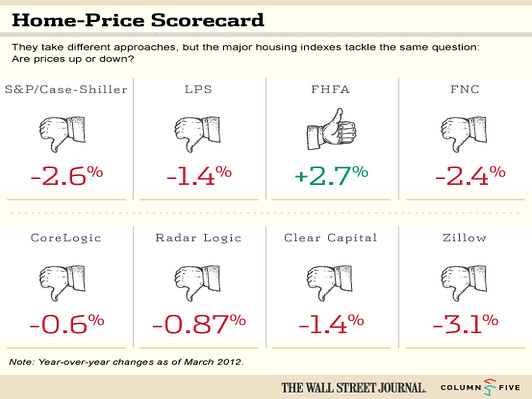

[WSJ] The Crazy 8: Comparing Results of National Home Price Indices

read more

November 9, 2009

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

The Housing Helix

[The Housing Helix Podcast] Bill Rayburn PHD, Co-founder, Chairman & CEO, FNC

read more

November 9, 2009

Analysis & Research

,

Appraising

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Interviews

,

The Housing Helix

[Interview] Bill Rayburn PHD, Co-founder, Chairman & CEO, FNC

read more

December 5, 2008

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

International

,

IRS

,

New York Times

,

Wall Street Journal

[Below 1%] Turning Japanese, I Really Think So

read more

Page load link

Go to Top