Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

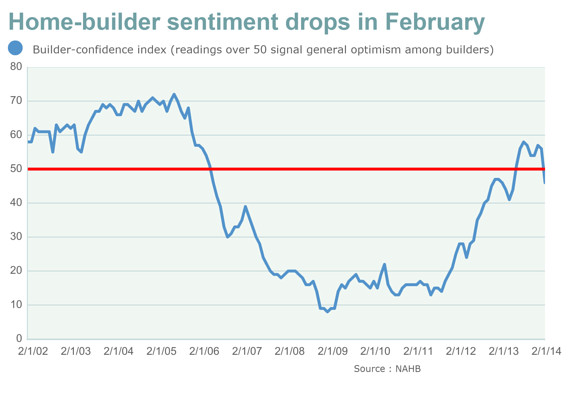

› NAHB

February 20, 2014

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

Housing Trends & Cycles

,

Media

,

Statistics, Metrics & Data

,

Weather & Natural Disasters

Housing Starts Drop: Whether the Weather or New Trend?

read more

December 13, 2012

Analysis & Research

,

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

,

Housing Trends & Cycles

[Housing Recovery Update] Proclamations Over Reasons, Statistics Over Logic

read more

November 4, 2012

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

,

Humor or Whimsy

,

New York Times

Why Doesn’t NAR Lobby Against Standard Time?

read more

July 14, 2009

Appraising

,

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

[NAHB] 26% Of Appraisals Faulty While AMC’s Talk Parrots

read more

June 24, 2009

Appraising

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

[NAHB] New Guidelines For Appraisers: Break Into Houses?

read more

June 24, 2009

Appraising

,

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

,

Market Reports

,

New York Times

[Snowball Pile] NAR Says Sales Higher, Blame Appraisers For Stalling Housing Recovery

read more

June 17, 2008

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Media

,

Statistics, Metrics & Data

[In The Media] Fox Business Interview for 6-17-08

read more

May 16, 2008

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

International

,

Media

,

New York Times

,

Statistics, Metrics & Data

,

Wall Street Journal

[In The Media] Fox Business C-Suite Interview for 5-16-08

read more

March 20, 2008

Adventures in Media & Marketing

,

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Statistics, Metrics & Data

Builder Confidence Not Building

read more

December 2, 2007

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

There Is No National Housing Market

read more

November 14, 2007

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Economy

,

IRS

,

New York Times

Housing Market Depreciates The Politics Of Future Expectations

read more

January 12, 2007

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Media

,

Migration, Psychology, Demographics

The National Numbers Don’t Feel Your Pain

read more

1

2

Next

Load More Posts

Page load link

Go to Top