Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› NAR

January 27, 2013

Adventures in Media & Marketing

,

Appraising

,

Brokers, Agents, MLS, NAR

,

New York Times

Broken Appraisal: Lack of Market Knowledge Overpowers Lack of Data

read more

December 13, 2012

Analysis & Research

,

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

,

Housing Trends & Cycles

[Housing Recovery Update] Proclamations Over Reasons, Statistics Over Logic

read more

December 6, 2012

Brokers, Agents, MLS, NAR

,

Elliman Reports

,

Housing Indices & Portals

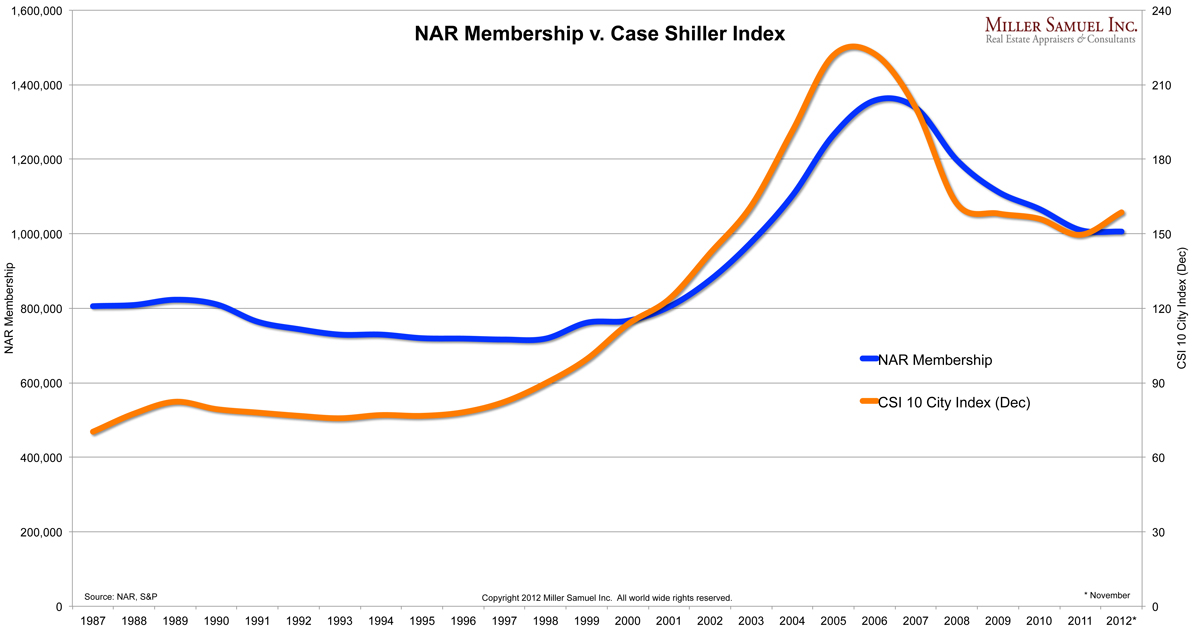

NAR Membership Flows With Housing Market

read more

November 27, 2012

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

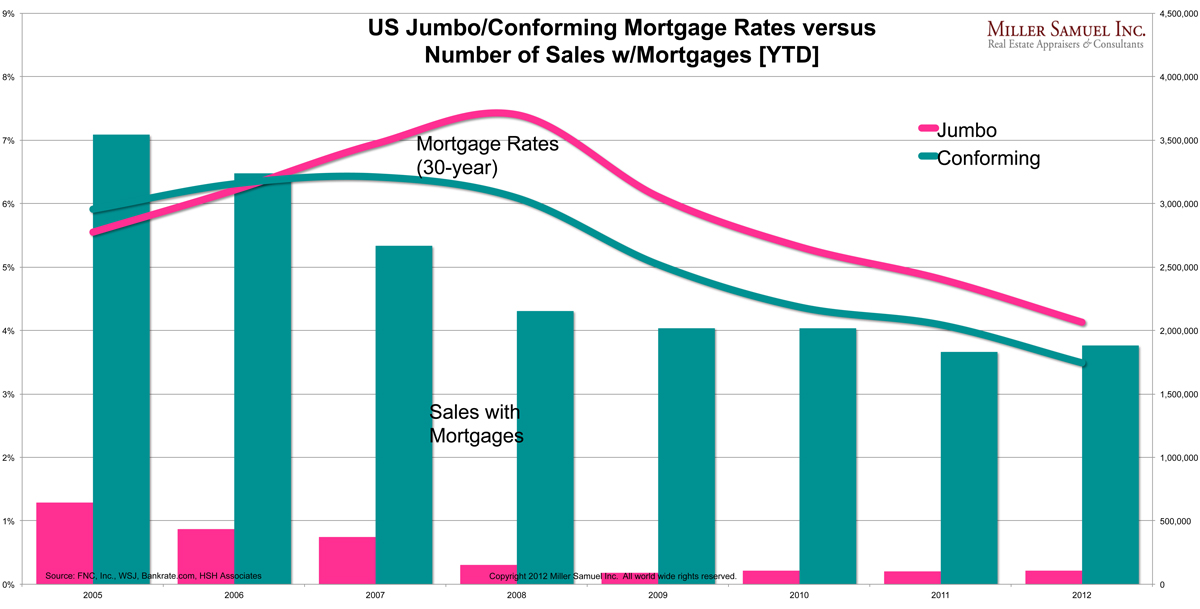

Get Down With It: Falling Mortgage Rates Are Not Creating Housing Sales

read more

November 4, 2012

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

,

Humor or Whimsy

,

New York Times

Why Doesn’t NAR Lobby Against Standard Time?

read more

September 19, 2012

Brokers, Agents, MLS, NAR

,

Curbed

,

Time Out

Housing Trends & Talk Like A Pirate Day 2012 (10th Anniversary)

read more

September 4, 2012

Brokers, Agents, MLS, NAR

,

Housing Indices & Portals

,

Inman News

,

South Florida

NAR and Florida Realtors to Create Repeat Sales Index: Why?

read more

August 29, 2012

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Elliman Reports

,

Media

[In The Media] BeastTV –

The Number

with Dan Gross 8-29-12

read more

July 19, 2012

Media

[In The Media] Yahoo!’s ‘The Daily Ticker’ With Dan Gross 7-19-12

read more

June 21, 2012

Brokers, Agents, MLS, NAR

,

Humor or Whimsy

[Ellen Show Video] Super Awkward Realtor Branding

read more

May 22, 2012

Bloomberg News

,

Brokers, Agents, MLS, NAR

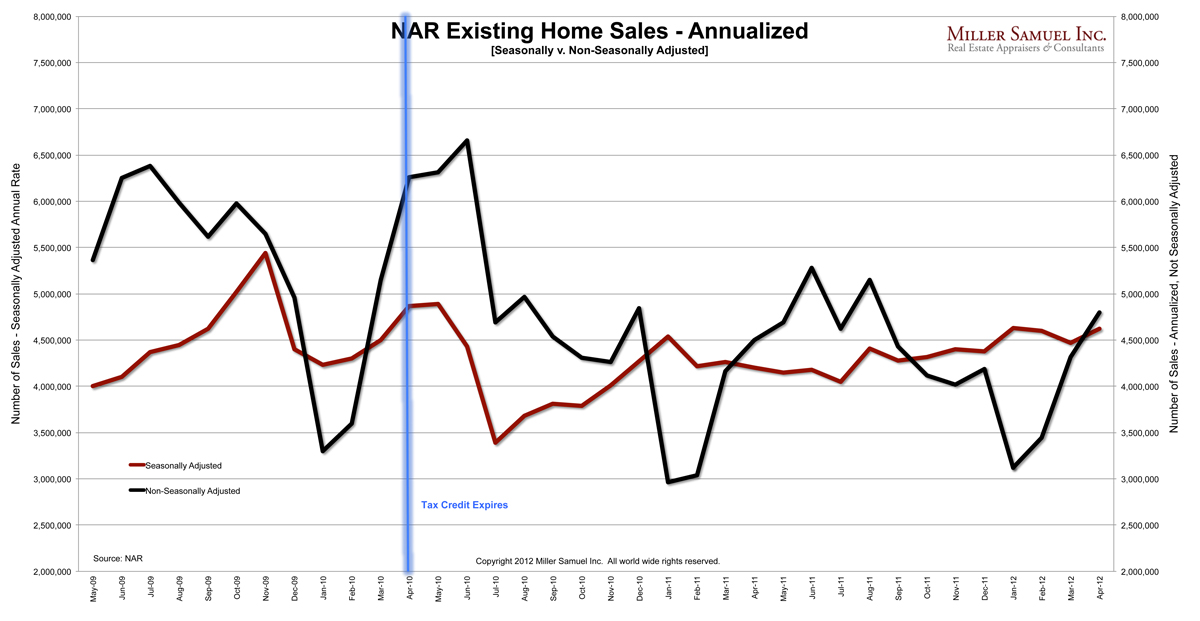

[NAR] Existing Home Sales Continue to Edge Higher +10% Y-O-Y

read more

December 1, 2010

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Interviews

,

The Housing Helix

[Press Call] Steve Berkowitz CEO, Sue Stewart SVP, Move, Inc. Realtor.com, Move.com, MortgageMatch.com

read more

Previous

2

3

4

Next

Load More Posts

Page load link

Go to Top