Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Zillow

July 9, 2012

Distressed Housing

,

Elliman Reports

,

Wall Street Journal

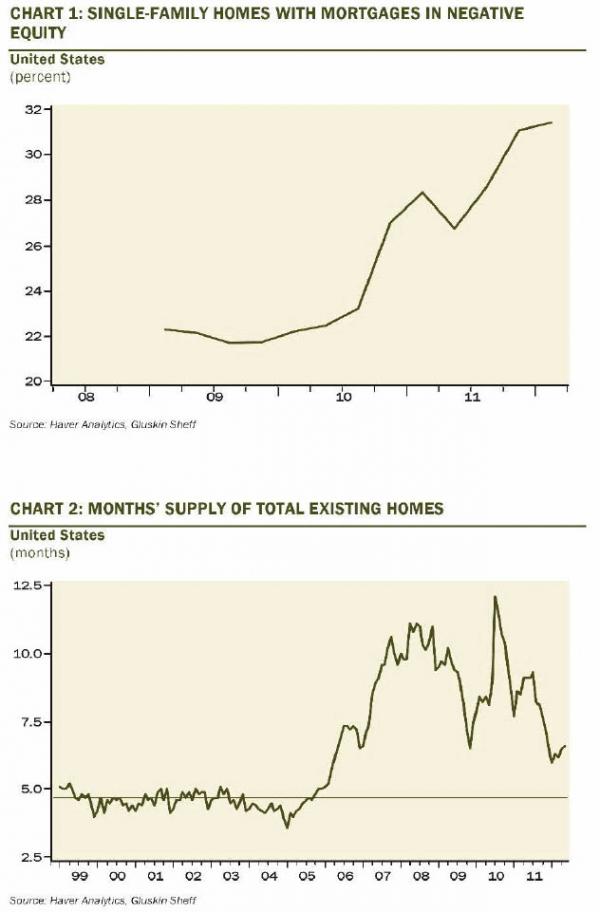

Low Housing Inventory Is NOT A Sign of Housing Recovery

read more

December 15, 2010

Economy

,

Inman News

,

Interviews

,

The Housing Helix

[Interview] Stan Humphries, Chief Economist, Zillow.com

read more

June 9, 2010

Amenities, Adjustments & Value Logic

,

Appraising

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

The Real Deal

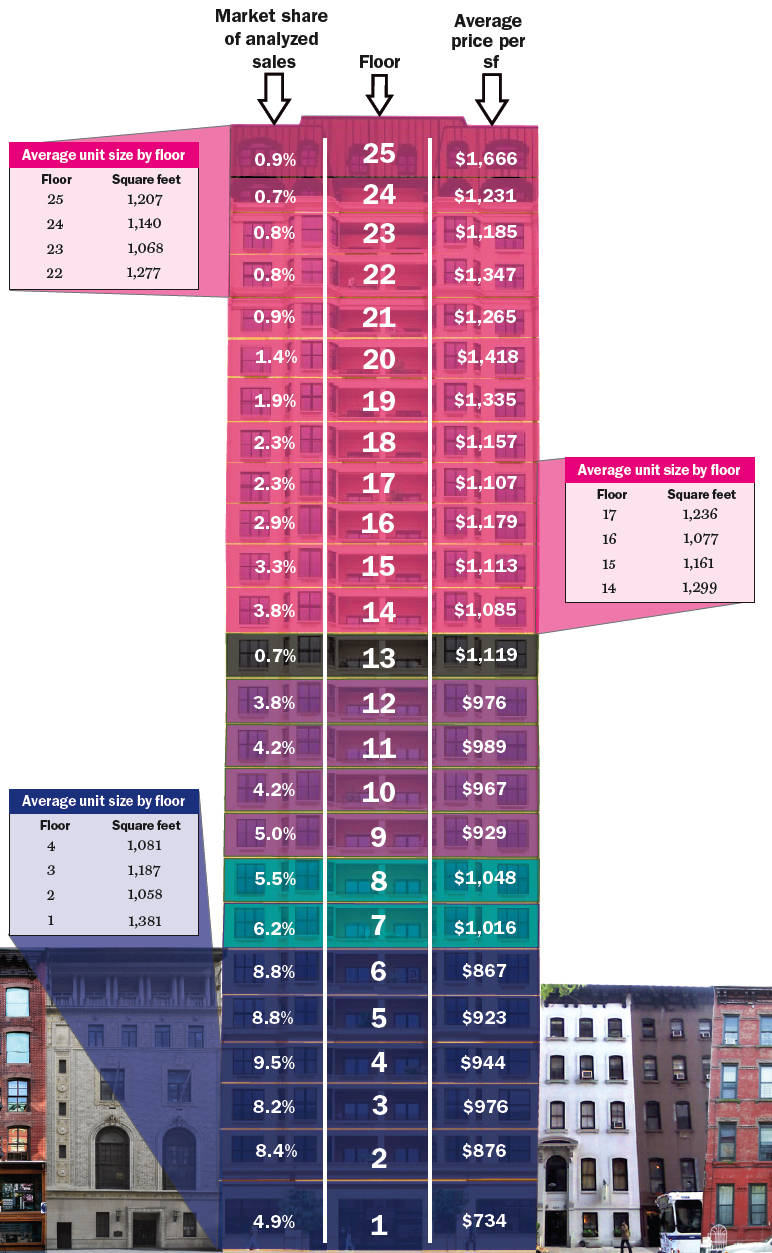

[ChartFloor] Manhattan Price Per Floor Breakdown

read more

March 3, 2010

Appraising

,

Brokers, Agents, MLS, NAR

Appraisal Journal Study Cites Flaws In Zillow AVM

read more

June 6, 2008

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

[The Homeownership Preservation and Protection Act] Dodd Bill Places A “Hit” On Good Appraisers, With Bondage

read more

June 6, 2008

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

,

Migration, Psychology, Demographics

[The Homeownership Preservation and Protection Act] Dodd Bill Places A “Hit” On Good Appraisers, With Bondage

read more

May 14, 2008

Affordability, Affordable Housing

,

Baltimore

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Humor or Whimsy

,

South Florida

,

Wall Street Journal

[Kayak Liquidity] Mortgages Underwater, Or At Least Those With A Pool

read more

March 14, 2008

Blogosphere

[Matrix ’82] Calling All Green, Irish (and non-Irish): Enter Your Carnival of Real Estate Submissions

read more

February 11, 2008

Blogosphere

,

Brooklyn

Carnival Of Real Estate [Week of February 11, 2008]

read more

February 12, 2007

Brokers, Agents, MLS, NAR

,

Government, Politics, Regulations & Policy

,

Migration, Psychology, Demographics

Zillow Gets Zerious About Public Records

read more

February 6, 2007

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Migration, Psychology, Demographics

Values: Being Precise About Precision Expectations (aka Good Enough)

read more

December 7, 2006

Media

Zillow Make(s) Me Move For Free

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top