No, I am not referring to the names in the Mitchell Report.

One of the advantages of the falling dollar has been the benefit to a handful housing markets, by attracting foreign buyers, enticed by the imbalance of currency. The British Pound is current about 2:1 and Euro is about 1.5:1 making for a significant discount to foreign buyers of US assets.

British buyers see US residential real estate at half price.

Specific to housing, real estate markets like Seattle, New York and Miami benefited from the increased demand, but housing markets in midwestern cities were likely benefited to a lesser degree, probably correlated to tourism trends. The weak dollar been one of the leading reasons that a market like New York City maintained relatively robust real estate market in contrast to many other markets. However, it is not enough of an economic force that it assures such a housing market from a downturn.

I wondered whether the weak dollar was really a good thing?

>A currency depreciation as big as the one the dollar has already experienced–to say nothing of the prospect of a further drop–would be a big inflationary problem for a small, open economy like Britain (which still has a currency of its own). The effect is muted for the US, because its economy is bigger, less open (not because of import restrictions, but by virtue of its size), and because exporters selling to America are more inclined to price to market.

The sharp increase in exports has helped temper some of the economic damage from housing.

>Every time the dollar weakens, US exporters and US import-competing industries are gaining competitive advantage and/or increasing their profitability. The explosive growth of US export volumes (reaching 10 percent per year) is part of the reason that, despite the collapse of US housing construction, the US economy is still expanding at a reasonable albeit declining rate.

The bottom line is that a weak dollar places the economy at greater risk for inflation, which has become a renewed concern over the past week as the FOMC opted for another 25 basis point cut in the federal funds rate.

Inflationary pressures bring on higher mortgage rates. And unlike Major League Baseball players, its not something to stick into the housing market.

4 Comments

Comments are closed.

Isn’t inflation the ultimate aphrodisiac for real estate? What ever happened to the notion that real estate is a good investment because it (at a minimum) keeps up with inflation? Especially for those with fixed rate mortgages, inflation is a great thing. Adjustable rate loans create a cash mismatch — higher carrying costs but also higher asset values, but unless loan values are far above asset values, they make out well too.

Vacation destinations that appeal to Asian buyers such as Hawaii other markets in Florida that appeal to Canadian buyers, flush with their own strong currency, will most likely also be supported by the weakening dollar.

Jon – Generally inflation is good for hard asset prices like real estate. But this environment has nothing general about it.

Inflation, generally is coupled with strong economic growth. Rates rise to combat inflation, and cool economic growth. In these times, jobs are solid, wages are strong, and affordability is not a major issue.

However, in stagflation times, where inflation is a problem and economic growth is anemic, thath is NOT good for hard asset prices. Rates will rise to combat the worse of 2 evils, inflation, at a time when economic growth is NOT robust, jobs are at risk, wages are not rising, and affordability IS a problem!

This scenario seems more likely right now. Even as inflation is a growing concern, affordability remains the top reason against real estate; not to mention rising inventories and declining confidence.

History repeats itself.

OK, foreign buyers are being enticed into a few select U.S. markets by the weakening dollar. They still need to feel optimistic about their investment and that requires a continuing stream of ready, willing and able buyers.

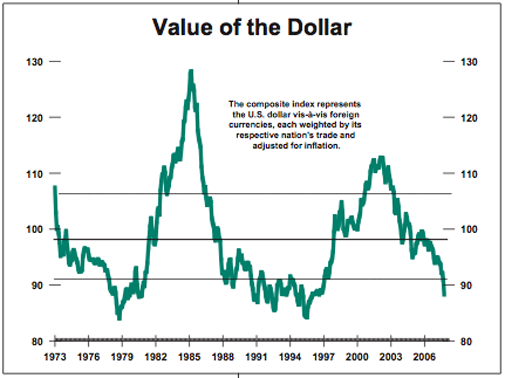

Look at the posted “Value of the Dollar” chart. As the dollar sank in the late 1980’s a major influx of foreign (mostly asian) buyers were scooping up American landmark properties. A slight case of xenophobia set in as we watched, stunned at the prices being paid for trophy buildings, bridges, golf courses, etc.

Just to cite one local example, a major Japanese conglomerate bought Rockefeller Center. Just like the current era, which is already over, the rules changed and sale prices were justified by unwarranted anticipation of never ending growth in equity and future income.

We all know what happened to that deal. Something similar could easily happen again. Stagflation would make it much worse.